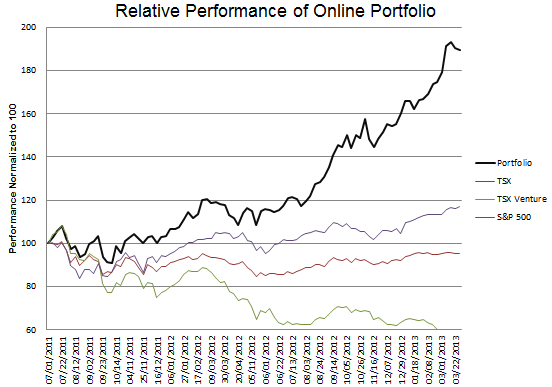

Week 91: Consolidating

Portfolio Performance

Consolidation

Patience is a difficult virtue. I’ve had 3 weeks of pretty so-so performance, some stocks going up and some stocks going down and overall not much of anything happening. With the market going up seemingly every day its hard to not let that play on your mind.

But you have to have a balance of patience and impatience to do well in stocks. You need to have a healthy level of impatience so that you don’t hold onto positions for too long, but tempered with an equal dose of patience because, as I read some time ago from a cagey market veteran, you will make 80% of your gains for a year in 2-3 weeks, and figuring out which weeks those are is nearly impossible.

In the last few weeks I think I demonstrated a little bit both; witness impatience in my selling of gold stocks and of my position in Tricon Capital and patience as I held on to falling positions in MBIA, Impac Mortgage and watched YRC Worldwide and Yellow Media correct substantially from their highs.

Reducing my position in gold stocks

I struggled over this decision last weekend. I understand that gold stocks are hated and oversold; indeed, this was my reason for adding trading positions in OceanaGold, Argonaut Gold, and Brigus Gold a few weeks ago. Had I held, I admittedly might still be able to pull off some short-term gains as the over-sold position is worked off.

And I remain sympathetic to gold over the long-run. As I’ve written extensively, I am wary of more credit dislocations and I expect the response to be further quantitative easing.

But I am also wary of current underlying conditions and what they portend to the short term price of gold. It appears to me that the credit system is reflating. The collateralization market is showing life. What clarified my opinion to sell was listening to the conference calls of a number of commercials REITs. As I will discuss below, there has been a marked improvement in the credit markets over the last 6 months .

Our economic growth is tied to the growth in credit. I’m a reader of the Richard Duncan (he has a new book I finished a month ago called the New Depression) and I agree with his argument that since the breakdown of Bretton Woods, the relationship between the money supply and growth has changed. Economic growth is now directly tied to our ability to expand credit.

While the conclusions that Duncan draws are dire (thus the title, The New Depression), and will likely be right in the long-run, applying it to the immediate condition leads to the conclusion that the reflation of the credit system should result in one more party before reality catches up.

In this environment, I’m not sure what happens to gold. On the one hand, the period between 2002 and 2007 could be used by analogy. The system saw credit expansion and the gold price rose significantly. Maybe that’s how it plays out.

But the difference this time is that gold is pricing in a certain level of easing already. How does gold react if the Federal Reserve begins to scale back its quantitative easing? It may not be favorable.

Now all this discussion presupposes that credit market growth does lead to economic growth; basically that the Fed’s programs will and are working. There are many who would argue that this is not the case. I am not suggesting that I know one way or the other. I am only suggesting that I am uncertain about which way this goes and which way that causes gold to go, and therefore I cannot get comfortable with the risk/reward for gold stocks. So I reduced my positions significantly.

New Positions in ABR and RAS

I’m late on this idea but hopefully not too late. I was introduced to Commercial REITs as an investment thesis by @Tito_z40 back in December. He told me to look at RAIT Financial (RAS), which was trading at about $6 at the time. I did so but (unfortunately) I didn’t really get the premise. I saw a lack of a discount to book (it was around $6.50 versus the a price $6.00 back then), and a dividend that was reasonable but not exceptional (it was about 6%). So I passed.

What I didn’t understand was how much RAIT was going to benefit as the securitization and funding markets came back, and that their ability to generate income by increasing originations and expand their balance sheet was just beginning to take off. RAIT said on their fourth quarter conference call that they expect to do $150 million of CMBS securitizations in Q1, versus $98 million in Q4. They also received a new $150 million warehouse line in the fourth quarter from Credit Suisse, which has allowed them to increase their bridge and mezzanine lending in Q1. Arbor Realty (ABR) has done even more. Arbor has structured two non-recourse CLO’s since the third quarter. These are the first two non-recourse CLO’s for anyone in the industry since before the crisis.

The thawing of credit has three virtuous effects on these REITs

- lower funding costs, both in the form of short term funding such as warehouse lines and longer term funding through securitization. Arbor pointed out on the fourth quarter conference call that the funding cost of the second CLO was 130 basis points lower than the first.

- increase leverage on their balance sheet. I compared Arbor Realty in 2007 to today and found that the assets on the balance sheet were $2 billion then versus $1.5 billion today with a similar level of equity.

- increased fees from originations of loans as demand for loans to feed the securitization channel increases

Of the two companies, I am less enthused with RAIT Financial than I am with Arbor Realty. Honestly, I didn’t have an intention to add a position in RAIT before they announced the secondary offering on Thursday. What really interests me is the idea that the securitized loan market is making a return. Arbor is proving itself to be a trailblazer in this area, having closed 2 CLO’s in the past 9 months, while RAIT management has said that the company is sticking to their bread and butter of originating loans for sale.

Still, with the dip in the share price of RAIT that coincided with the secondary, I opportunistically picked up some shares for a trade.

Both of these stocks have had significant runs over the past few months, and I am hoping that what we are seeing in the commercial space is akin to what we saw in the residential space last year; that the run thus far is only the first leg. In the case of Arbor, which is still trading at a 25% discount to the net asset value (which the company disclosed on their 3rd quarter conference call) and at a similar discount to adjusted book value (which was $10.40 at year end), I am fairly confident this is the case. In addition, Arbor has been repurchasing debt from its own CDOs at a discount, to the point where the CDO bonds owned by the company have an implied discount of $3 per share. This discount is not reflected on the balance sheet, where the asset and liability cancel out one another, but when the CDOs are unwound the company will receive the $3 per share in cash flow from the discounted bonds.

Adding back MGIC

I reduced my position in MGIC (MTG) after the stock ran up over 100% in little more than a week. It was fairly clear that some consolidation was needed before it moved higher. This last week, with the stock having fallen about 20% from where I sold down my position and 30% from its highs, I decided to add the position back in the $4.30’s.

When I look at each of the positions in my portfolio, I am hard pressed to find one that I think will perform better than MGIC. The company operates in an industry with high barriers to entry (mortgage insurance requires significant up-front capital and approvals from the GSE’s as well as state regulators), has seen many of its competitors fall into bankruptcy or run-off, is insuring houses that have been underwritten with extremely tight standards, is underwriting the vast majority of its insurance based on a monthly premium model that will continue to pay fees as long as the mortgage is outstanding, and this in an environment where its hard to imagine rates not going up and where home prices are increasing, and has stated that the new business that is being written is expected to return at least 20%. It’s a tough story to beat.

There was also an interesting press release put out by the FHFA on Thursday. The FHFA announced a program that will allow homeowners who are both delinquent on their mortgage payments and underwater on their house to refinance at lower rates and extend the terms of their mortgage out 40 years. The program appears to be extremely flexible and does not require any documentation or income or assets. While one might object to the construction of such a program, there can be no doubt of its positive impact on the MI business.

Another Chapter for Equal Energy

I’ve been in and out of Equal Energy (EQU) for a little over a year now with very little success (so take these comments with that grain of salt!) However I had a bit of luck this time around, getting back into Equal the day before the announcement of a takeover bid from Montclair Energy. Sometimes it can seem like fate is against you, while other times its at your beckon call. Overall it probably averages out I guess.

I got back into Equal because both natural gas and propane storage levels have been falling precipitously with the cold weather (see the figure below), because some much needed terminal capacity to export propane will be coming on-line in the next 6-12 months, and some much needed pipeline capacity has been added and should alleviate the the NGL bottleneck that has been plaguing prices at the Conway hub, where Equal delivers their Hunton production.

While I was happy to see the takeover offer, I think that given the improving environment we should expect a better offer. What was a small position in the company before the takeover I have made a large position since. The risk is that if the bid doesn’t go through the stock could tumble back. But I am of the mind that the better possibility is that a higher bid emerges, my guess would be in the $5 area, or that Montclair raises their own bid somewhat to win over management. Given the improving economy, the improving transportation dynamics around NGLs and the improved natural gas outlook, I don’t think the risk is very high that the $4 bid is pulled. So it seems to me like a good risk/reward, particularly in a market where I’m having more difficulty finding opportunities.

Exiting Tricon… for now

I need to do more work on Tricon (TCN.to). I have tied myself up analyzing the REITs, which is a new business for me to understand and therefore slow going, until I get some time to really analyze the home buying business and make sure that its going to work, I decided to let go of my position in Tricon.

The other thing that continues to nag me about Tricon is the asset management business, and the long lag before the company begins collecting its incentive fees on its funds. Part of my concern has to do with the Canadian housing market, where I continue to hear stories about the number of unoccupied condominiums in Vancouver and, to a lessor extent, Toronto, and the other part has to do with the susceptibility to sentiment – that when you have earnings so far out in the future its very easy to imagine scenarios both bad and good that cause very different interpretations of net present value.

Finally, taking positions in Arbor Realty and RAIT Financial used up a lot of cash, and so the other consideration in my sale of Tricon was simply the desire to not become over levered.

I plan to come back to Tricon in the next few months and re-evaluate my decision.

What I’m looking at now

I’m having trouble finding opportunities. I look 5-10 new stocks a week with some detail, and while in December doing so was uncovering so many opportunities that I didn’t know what to do with them all, the work I have done lately has come up with very little. In the next week or two I expect to continue my search for undervalued natural gas companies, in particular light natural gas liquid producers that, and to come back to the auto parts makers, both re-evaluating American Axle Manufacturing (AXL) and taking a look at Martinrea (MRE.to) and Supreme Industries (STS).

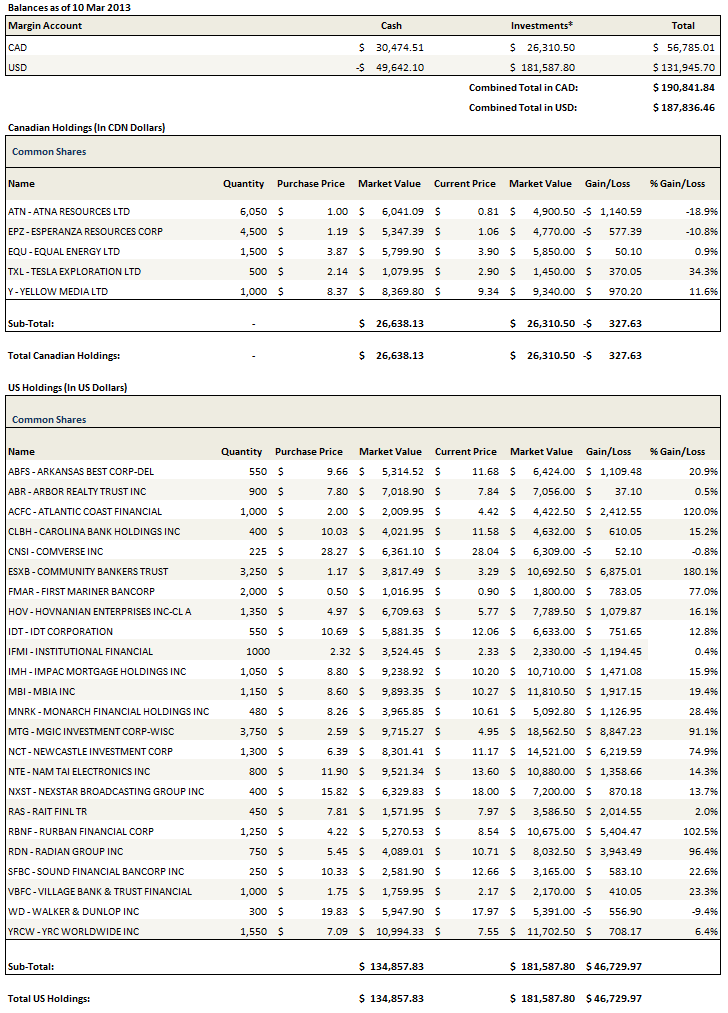

Portfolio Composition

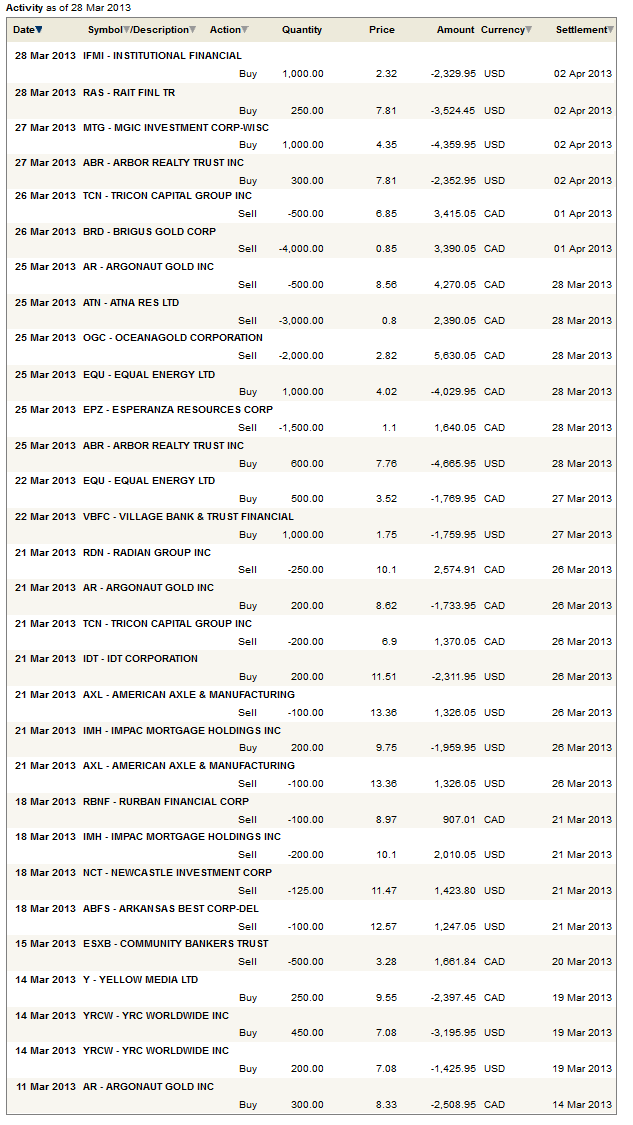

To see the last three weeks of trades, click here.

{kind=link}

The following comment is from Andrew Shapiro from Lawndale. More pressure on the BofD to realize value at Equal:

You are referring to New Source Energy LP (NSLP) http://bit.ly/16mqcaf It is trading for a valuation multiples far higher than Equal. This despite Equal’s larger production and reserves, which arguably create greater efficiencies and margins on the necessarily costly Electric and water infrastructure needed in De-watering play of the Hunton.

It is a natural for NSLP to be making a bid for Equal. NSLP is loaded with newly raised (from the IPO) cash and currency from a continuing higher multiple. NSLP will have this one opportunity to seize upon such a synergistic play in its backyard. Should a larger player acquire EQU, then the relative valuation multiples between the two companies the next time may not be as favorable to NSLP. If I were a board member of NSLP I would be pounding the table to consider what accretive price (to NSLP) makes sense and enter the fray.

We are preparing a letter for EQU’s board that expresses our expectations and concerns over recent events and the upcoming process.

http://seekingalpha.com/currents/post/907241