Getting Comfortable with Walker and Dunlop

I was originally put on to the idea of Walker & Dunlop (WD) by a reader of the blog back in September (while I will leave the name of that tipster anonymous, many thanks for the idea). The call was prescient and I can only wish I had made my purchases sooner.

As it was, I initiated a position in Walker & Dunlop about 4 weeks ago, doing so after the stock had fallen 10% from its 52 week high of $21.76. Unfortunately that turned out to be at least $2 too soon.

The stock has subsequently fallen further. As usual being wrong has compelled me to re-evaluate my thesis, which I did this week. After some waffling I have decided not only to hold on to the position but add to it, which I did on Thursday and again on Friday.

What they do

Walker & Dunlop is the commercial lending equivalent of Nationstar Mortgage. Their business is the origination and servicing of commercial mortgage loans. The vast majority of those loans are multi-family and are passed along to Fannie Mae, Freddie Mac or into HUD insured Ginnie Mae securities. The company generates revenue from origination fees and on the servicing of its loans. They are the eighth largest originator of commercial mortgage loans in the United States, and the second largest originator of multi-family loans.

Extending the analogy to Nationstar, Walker & Dunlop recently acquired its fellow commercial originator CWCapital from Fortress Investment Group, who became a large shareholder after acquiring 11.6 million shares as part of the sale.

Why the stock is being pressured

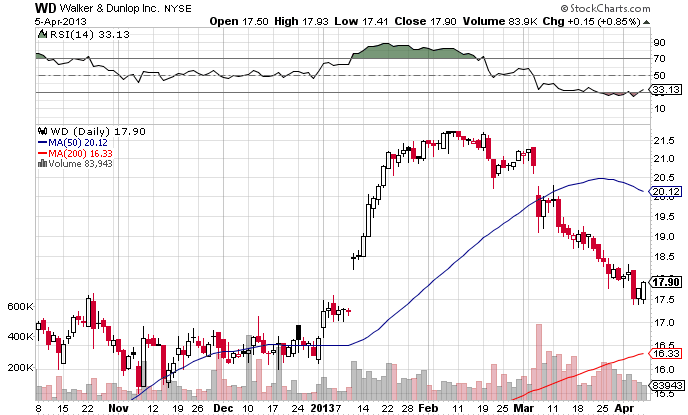

The weakness in the stock has coincided with the end of the lock-up period on the Fortress shares, which ended at the beginning of March. A look at the chart shows how closely the decline has coincided with it.

On the conference call discussing the acquisition management hinted that at least some of the Fortress shares would be sold once the lockup period ended. The shares held by Fortress are equally divided between Credit and Private Equity funds (see disclosure here). As the comments from the CWCapital acquisition conference call indicate, the position of credit funds are at risk of liquidation.

Fortress has two sides to it, a private equity side and a credit side. And our stock is held between those two sides of the house, if you will. And so, if – I know that the private equity side looks at this as a longer term investment, if you will. And I would think that the credit side looks at it as a shorter term investment. And therefore, it would not surprise me if the credit side looks to do something during 2013 with some of their shareholdings, I have absolutely no idea when, how much, what have you.

In retrospect I should have investigated this from the get-go. Buying in the second week of March was, to put it bluntly, stupid. Even now I might be too early. Since the beginning of March about 4.5 million shares have traded hands. The position of the credit fund appears to have been in the neighborhood of 5.75 million prior to the end of the lockup period. So depending on the extent that they want their position to be reduced, we could have some ways to go.

The Good Thing about having Fortress on your side

Being affiliated with Fortress is not all bad however. Fortress has two directors on the Walker & Dunlop board and I expect that those directors will be able to create value much in the same way that Fortress has done with Nationstar. Consider this excerpt from the CWCapital acquisition conference call:

Fortress, you know this very well, Brandon, I mean with Nationstar and with a number of other investments that they have, they not only know how to raise capital very effectively, but they also have been very capable at figuring out where there are opportunities and how to go about, if you will, navigating these waters. And so I think that having two seats on our board that will be representatives of Fortress and having them be such a big shareholder is very advantageous to us.

In particular, having Fortress in their corner during a wind-down of the commercial business of Fannie Mae and Freddie Mac would be particularly helpful, as they could become both a source of funding and of end customers. While the re-election of the Obama administration makes it less likely that anything dramatic will happen to the GSE’s in the near term, eventually they are going to be dealt with, and Walker & Dunlop stands in a better position aligned with Fortress.

Also, as part of their next stage of growth Walker & Dunlop has expressed the desire to expand into other types of commercial lending and to develop non-GSE conduits to deliver their loans such as a REIT or into private label CMBS. They admit that these moves will put them in more direct competition with lenders that have a lower cost of capital. Fortress is going to help Walker & Dunlop even that footing.

Post-acquisition Walker & Dunlop

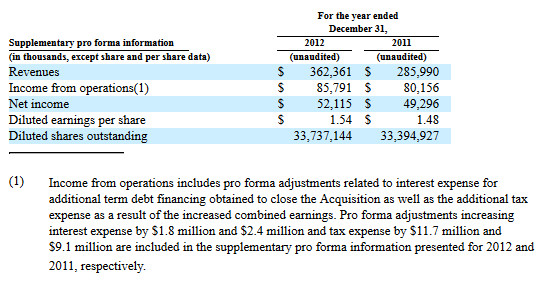

In their 10-K, the company provided a pro-forma estimate of what the combined Walker & Dunlop / CWCapital entity income statement would have looked like had the two companies been together during 2011 and 2012.

While not included in the above estimate, Walker & Dunlop has also pointed to a number of cost savings that they could achieve once CWCapital was integrated into their business model. First, they expected that they could reduce the cost of servicing on the loans acquired from CWCapital by 40-50%. Second, they decreased the cost of warehouse financing by 18-20 basis point and further reduced CWCapital’s costs by another 20 basis points after shifting their closings over to the Walker & Dunlop facilities. Third the consolidation of staff and employees eliminates 25 positions and will save $5 million to $7 million per year in G&A.

What I Hemmed and Hawed about

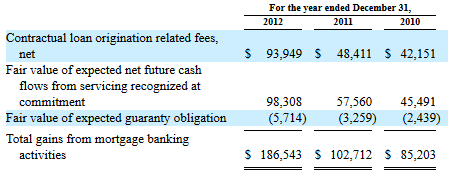

A large portion of Walker & Dunlop’s gain on sale comes from capitalizing mortgages servicing rights that are held onto after the loan is originated and sold. The following figure is from the 10-K. It illustrates that more than 50% of gain on sale comes from capitalized MSR. While there is nothing that suggests that their capitalization metrics are out of line, it is a non-cash item, so earnings and cash generation for the company are not necessarily the same thing.

There are some that have been questioning this method of accounting. Doug Kass has declared a pair trade that shorts Nationstar while going long Ocwen. My understanding is that the trade is at least in part predicated on the accounting methods of Nationstar, which follow the same MSR capitalization model as Walker & Dunlop.

After giving it some thought though, I don’t think that the same concerns that apply to Nationstar apply to Walker & Dunlop. The concern is that the capitalization of the MSR causes earnings to depend on continual generation of new originations. If originations volumes fall, earnings at Nationstar will too. With the Ocwen model the MSR is not capitalized and so the revenue generated by the MSR is not offset by the amortization of that capitalized value. Thus earnings will not suffer nearly as much.

While the same logic applies to Walker & Dunlop, the difference I think is that there is very little concern that commercial originations will suffer from rising rates in the same way that residential originations are expected to. Commercial loans are typically far less rate dependent then residential loans. In fact part of my investment thesis is based on the expectation that a large volume of commercial loans will require refinancing over the next few years.

Solid Guidance for 2013

What got me interested in Walker & Dunlop in the first place was reading through the fourth quarter press release, where they announced guidance for the industry and for themselves.

“As the economy recovers and the financing markets heat up, there is a fantastic opportunity for us to continue growing in a fast, yet measured and risk-appropriate manner. The Mortgage Bankers Association estimates 14% annual growth in commercial / multifamily loan originations until 2015, and with almost $2 trillion of commercial real estate loans maturing over the next 5 years, our market opportunity has never been greater. As we have said before, we expect to originate between $10 and $12 billion in commercial real estate loans during 2013, with $1.9 to $2.4 billion originated during the first quarter, compared to $674 million of originations in the first quarter 2012.

In comparison, in 2012 Walker & Dunlop originated $7.1 billion in loans. Including originations from CWCapital, $9.5 billion loans were originated. So they are expecting reasonable growth this year.

What 2013 might look like

Both fee and capitalized servicing margins have been pretty consistent over the last couple of years (fee margins were 132 and 120 basis points in 2012 and 2011 respectively, while capitalized serving was 143 and 138 basis points). Thus, in order to ballpark 2013 earnings it seems reasonable to take the average of the two years and run those margins at the mid-point of the 2013 origination estimate of $11 billion. Doing so calculates total gains from mortgage banking activities of $292 million. On the fourth quarter conference call the company said that they expect to generate $90 million from servicing fees. On top of that I will make a conservative assumption that they generate an additional $18 million from warehouse interest, escrow earnings and other sources. Together it adds up to total revenue of $400 million. Assuming an operating margin of 31% gives about $100 million of operating earnings and $76 million of after tax earnings. That is $2.26 per share.

The company could exceed these estimates if costs come in lower or revenues higher. The 31% operating assumption is consistent with what was achieved in 2012, but far below the 37% margin they had in 2011. I have already mentioned a number of synergies the company has identified with CWCapital. It is also possible that the company is guiding revenue conservatively. Fourth quarter origination volumes of the combined Walker & Dunlop / CWCapital entity were $2.9 billion.

While estimates based off of management guidance are always something to be wary of, keep in mind that this is a company that set out 5 years ago with the lofty goal of growing revenue, income from operations and net income by five times in the next five years, and proceeded to do just that. Ignoring the acquisition of CWCapital, the company organically grew originations by 20% in 2012. Thus I have some comfort that management estimates can be met or even exceeded.

My Plan

I made a mistake by buying the stock too early but I don’t think I made a mistake by averaging down this week. As I’ve explained in the past I only add to losing positions after careful consideration. It is a rule I don’t break lightly. In this case I did, and I plan to do it again if it falls into the $16 range. I would consider my current position two-thirds full, even though it is admittedly quite large (about 7%). My enthusiasm in the face of dissonance is due to a belief that the selling is the consequence of a large shareholder exiting their position for reasons unrelated to the business. Thus, I will take advantage of it while it lasts.

I don’t see Walker & Dunlop as a particularly risky stock at least in comparison to many of my other positions. They are a leading multi-family commercial lender, have steady margins and are run by a management team who has proven themselves to be capable of navigating a growing business. The main risk I see is that they are levered to the US economy; if the United States falls back into recession, the stock will suffer as the demand for loans dries up. I have already described my thoughts on this on numerous occasions; while the long term outlook for the US economy is murky at best, the short term should be buoyed by an improving residential housing market, the return of private credit and the continued easing of the Federal Reserve. So that is a risk I am willing to take.

Interesting analysis – thanks.

What kind of multiple do you think this stock should be on?

You have a great blog… very good write up on this name. I have owned WD for the past year and will just add my 2cents. WD’s servicing portfolio alone is $35B as you allude to… the nature of CMSR’s are mostly prepay protected. From pg 5 of the 3/6 slide deck… servicing is expected to generate $680M over the life of the portfolio. That’s greater than their current makt cap. And it may be realized over what, 8 years? And this servicing fee component of WD is only 25% of their total revenue. They acquired a lot of capacity in 2012 and now they must fill it or else 2013/14 are going to be lumpy years.

Here’s my wild speculation: Fortress owns 73% of NSM, and NSM is the feeder of servicing rights to NCT (also owned by FIG) to spin off the dividends. Walker Dunlop is now 47% owned by Fortress w/ 2 seats on WD’s 11 person board. Would it be beyond the realm of possibility that NCT ends up becoming the dividend paying bucket for WD’s CMBS too? Just a thought.

Nice timing on Q1 announcement : http://finance.yahoo.com/news/walker-dunlop-announces-1q13-loan-120000970.html

No change to my idea but maybe $16 will happen

What is your take on valuation? The stock looks to have traded for 8-10x EPS in 2011 and 2012. Assuming the multiple doesn’t change and your 2013 estimate is on target, we’re looking at an $18-22 stock for 2013. That doesn’t seem like a lot of upside. What is the case for big upside? Multiple expansion? Continued growth? Both? I think it is worth noting that while revenue has grown rapidly, margin compression and more importantly sharecount increases have resulted in flat EPS over the past three years. What are your thoughts on this?

Thank you for all the great work.

I don’t think there is anything wrong with your analysis, except that I am expecting more love for the sector as the CRE market improves. I’m also expecting some surprises from the Fortress relationship that help them exceed those estimates.

Great analysis!

I came up with similar conclusions on WD, except I am leaving out MSR capitalisation and only taking into account servicing fees (0.24% of servicing portfolio, or the 90m you mention) when calculating cash revenues. I believe this gives a slightly better perspective on company’s cash generation capabilities and avoids double counting of servicing fees.

Another point on price pressure, For me it seems this was more caused by Credit Suisse rather than Fortress selling off (at least I get this info from insidertrading.org). CS reduced it’s stake by 30% over last year and still has plenty of stock to go (any thoughts on this?) So if Fortress starts selling as well, further price drops can be expected.

Anyways, thanks for a really nice write-up