Some Conclusions on the Natural Gas Market

I have spent much of my weekend researching the state of the Natural Gas market. In this post I am going to outline what I’ve learned and draw some tentative conclusions.

My interest in natural gas was piqued after the abnormally cold March that we’ve had and the coinciding decline in natural gas storage to below the 5 year average.

Subsequently, after reading an article posted by @Dedwardssays on his blog and a couple of articles on Seeking Alpha, I took a position in Gastar Exploration (GST). At the same time I added a call position in Exco Resources (XCO). Since then I have added a small position in WPX Energy (WPX), which appears to have had a large Niobrara discovery in the Piceance Basin. I also, of course, have held a position in Equal Energy (EQU) for the last number of weeks. I am actively looking for undervalued natural gas biased companies producing the in the lower 48.

Much of my research has focused on the following question: is the current price trend sustainable? I’ve found quite a bit of information on the excellent Berry Petroleum message board on InvestorVillage, including charts of rig counts, anecdotal evidence of Marcellus behind pipe capacity, and the excellent detailed projections from Robry.

I’ve mentioned Robry before. Robry has been posting daily gas flow updates for as long as I have followed the site. His weekly storage projections are comparable to (if not better than) the analysts. He knows the natural gas market as well as anyone. So when he made the following comments on Friday, I took notice:

Natgas remains terribly bullish, and for those here on the buy-side this is going to be a wicked, take-no-prisoners type of bull market once we get beyond bottom-hole testing next week (when all storage fields are open for injections). Those 794 BCF (EIA) and 873 BCF (Cap/gf) year-over-year deficits have to be dealt with, and quashing generation fuel-switching is only (says the Longer-Term model) going to get us half-way there.

While I do not have the knowledge of a Robry, I do work in the natural gas industry, and am well aware of the dynamics that exist that can lead to large swings in price. In particular, those elements are:

- Multi-frac horizontal wells that decline precipitously in the first year

- Companies switching their drilling programs between gas and oil and those budgets are generally re-evaluated only on a yearly basis

- Adding natural gas infrastructure (compression, pipelines) is not trivial and the uplift of such programs is often over-estimated (one wells uplift is another wells backout)

- Demand shifts caused by coal-gas switching for power generation

- The lag between when a decision is made (to drill a well or not to drill a well) and production is impacted is anywhere between 3 months and a year and so cause and effect is not always clear (human beings are terrible at discerning temporal delays between cause and effect. The excellent book Logic of Failure describes this in detail)

I am also wary of rosy projections about the abundance of natural gas. Having worked for a company who comes up with the PDP and PUD estimates that we all rely on, I can tell you that there is a great deal of uncertainty as to how accurate our methods are for predicting the performance of complicated horizontal wells with dozens of fractures. It was hard enough to anticipate well performance when the unknowns were the geology, now that the near wellbore geology is being blown to all hell before the well is produced, there is even less uncertainty as to how that well might perform 5 years out.

But I digress. That is a long term question and I am looking for short term answers. And my short answer, having processed all of the articles and digested all of the numbers, is that the picture appears to me to be constructive.

The natural gas market is complicated and trying to come up with a definitive conclusion on its direction would be a foolish thing for me to do. Luckily I write a blog and not an investment advisory or another such publication that requires certainty. Thus I can be quite honest and say that I am left with only tentative conclusions. This does not look like a no-brainer to me, but there is evidence that suggests we have turned the corner and that higher prices lie ahead.

The most compelling argument in favor lies with the rig count. Natural gas drilling has fallen off of the cliff. Below is the natural gas rig count since 2005 is shown in red.

What has consternated those who have been long natural gas over the last twelve months is that even as that rig count has dropped off, production has remained stubborn. I think there are a number of reasons for this:

- Pad drilling allows for a single rig to be more efficient

- Associated gas from gas-condensate and volatile oil fields (such as the Eagleford) is continuing to be drilled for

- The tie-in of the backlog is being worked through

- The Marcellus production has risen faster than anticipated

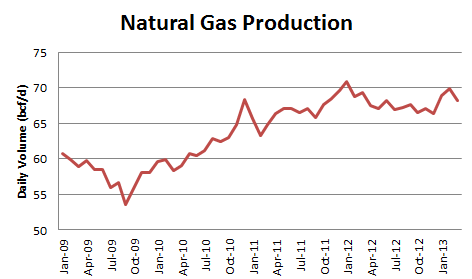

But given how far the rig count has fallen, I can’t help but think that an inflection point is soon to be upon us, if we have not already crossed it. Robry’s dry gas production figures, which I have graphed below, look toppy.

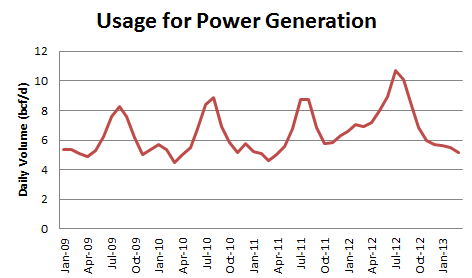

The two arguments used most often to support a bearish thesis are that coal to gas switching will reduce natural gas demand significantly through the summer months, and that a large backlog of drilled and completed exists in the Marcellus and that those wells will soon come on-stream.

Thomson Reuters estimated last week that coal-gas switching was down to 2.3 bcf/d, which would be the lowest level since June 2011. When I compare the current seasonal level of generation demand against prior years, even after accounting for changes in the weather (again taken from Robry’s data), it doesn’t look to me like there is significant demand over and above what has been used in 2010-2011, when coal-gas switching was at normal levels.

It is worth noting that what’s left of coal-gas switching is going to come from Central Appalachian coal, which becomes competitive at $4.25/mcf gas.

I have read in some places that there is as much as 4-6 bcf/d of capacity that is behind pipe but not on-stream in the Marcellus. I’m just not sure I believe it. According to Range Resources, current production in the Marcellus is around 9 bcf/d. That there is more than 50% of that total just waiting for completion and/or midstream operations seems unusually large to me. This article, from SeekingAlpha, suggested more reasonably that production in the Marcellus may increase 2 bcf/d by the end 2013, which is not an insubstantial amount in its own right, but nowhere near the bearish estimates.

While the Marcellus may have a large backlog of drilled, completed, ready to go and shortly to be on-stream wells, it is certainly not being discussed by the companies with large drilling programs in the Marcellus. I read through the transcripts of most of the large Marcellus producers (Cabot, EQT, REXX, Anadarko, Range Resources, Gastar) and saw very little about drilled and completed production waiting for pipeline capacity. There does appear to be infrastructure constraints, but these are preventing wells from being drilled, and some companies, including Gastar and Cabot, seem cautious about expansion this year because of the lack of infrastructure.

What’s more, the other consistent theme from the conference calls was that drilling will be focused on the “super-rich” region where condensate yields are higher. With condensate making up over 50% of the production for these wells, natural gas production will be significantly lower than it would have been had the dry gas areas been the focus.

What goes for the Marcellus can be said for United States natural gas production as a whole. Why would producers switch from oil to gas when the price differential so heavily favors oil? The crux of the bullish argument is that the rig count is too low and that the rigs drilling for oil with associated gas and gas-condensates are not going to produce enough gas to cover the deficit created by the dearth in dry gas production.

I am sympathetic to this argument. I think that what we’ve seen over the last 12 months is the natural lag, and that we are probably nearing the end of that lag. But I admit I only draw this conclusion tentatively and therefore will only look to slowly increase my positions in natural gas names as evidence mounts that I am right. Unlike many of my investor friends I require only a moderate level of conviction to move ahead with an investment thesis. I am happy to have a thesis that makes sense to go along with a significant reward if proven right, and to ride that until the evidence becomes clear one way or the other. I have found this behavior to be a profitable strategy, because so often by the time the evidence is clear the move is mostly over. Thus, that is what I plan to do hear, adding to positions over the spring and summer as long as production does not increase substantially or there is not a drop-off in demand. The upside of being right, if prices really can explode as Robry is suggesting they might, warrants the speculation.

thanks for posting this view and info. how does storage factor into your view?

LPR is interesting. At $1, it probably has about $3-$5 of assets. It’s a Canadian spinoff from Forest Oil. Mgmt appears to be waiting for Sept, when the 2 year tax anniversary arrives and it can sell itself to highest bidder (it’s got too much high-cost debt at this point to invest in more production). At $1, if you can wait six months, I see a good return.