A look at the Gastar’s Hunton Play

I took a position in Gastar (GST) as part of a basket of stocks I bought to play the natural gas price recovery (which I wrote about here).

Soon after I added the company released news of a transaction with Chesapeake to acquire a significant amount of acreage in Western Oklahoma. At the same time they unveiled that their secretive mid-continent play was the Hunton in Oklahoma (not an unfamiliar name to us Equal Energy bagholders), and that the acreage being acquired from Chesapeake would expand their position in the Hunton significantly. As it was, I bought more.

This weekend I listened to the Gastar presentation at the IPAA Oil And Gas Investment Symposium and I was happy to hear how well their second Hunton well is performing.

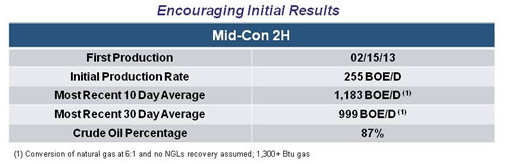

For comparison on April 4th, when Gastar announced the Hunton transaction with Chesapeake, they provided the following table showing the production of the Mid-Con 2H well:

April 4th Midcon-2H Update

On April 16th, at the IPAA, Gastar provided an update. Curiously, this updated slide is available with the presentation, but is not included in the slide deck downloadable on their website.

April 16th Midcon-2H Update

This is turning out to be an outstanding well. It has been on production for over two months and produced at nearly 1,200 boe/d for the last 10 days. What’s more production is continuing to increase.

The increasing production is a curious aspect of the well, but one which I not able to draw any firm conclusions on. At first I thought that the increasing production was due to dewatering. Equal Energy has been drilling Hunton wells to the east of Gastar, in Logan and Lincoln county, and the type curve on those wells shows an unorthodox increase in production over the first few months. This is caused by oil trapped in smaller pores being released into the originally water saturated fracture matrix. In a situation somewhat analogous to a CBM well but without the adsorption, the reservoir needs to deplete the water in order to release the oil, with the result being initially high water production, followed by increasing hydrocarbon production.

However this does not appear to be the dynamic occurring in the area being explored by Gastar. I have yet to hear a mention of a “dewatering phase” by Gastar, they do not talk of a production plateau, and the type curve the company provided as part of their IPAA presentation looked very much like the typical decline curve we are all used to.

The alternative is that the well is still cleaning up, but this seems to me to be going on too long for that. So it remains a mystery to me what is different and I welcome any comments as to the dynamic that is at play.

One other possibility is that this just isn’t the same Hunton. Gastar has explained that they are chasing a lower layer of the Hunton, above which lies a gassier zone. Perhaps this is the explanation; that there is a second, more conventional Hunton zone that lies under the first. If that is the case, it begs the question of whether this lower zone lies under Equal’s land as well (hmmmm).

In order to illustrate the geographical proximity of the Gastar and Equal drilling, below I have taken a slide from Equal’s most recent investors presentation and highlighted the area (in red) where Gastar drilled the Mid-Con 2H (they have also drilled and put on production another less prolific well, and have two others that have not had results released yet).

Though questions remain, it cannot be denied that Gastar has potentially found something quite good here. The company has around 88,000 acres in what they call the “Tier 1” Hunton. Regardless of the reason that the production profile is different, this remains a significant well for a company this size. In the fourth quarter Gastar produced a little over 7,000 boe/d. The wells that Gastar is drilling in the Hunton are part of a 50/50 JV, so the April production net to Gastar from the 2H is around 550 boe/d.

As I have delved into Gastar over the last few weeks I have been impressed by the quality of their acreage even as I am made wary by their current cash flow multiple (about 8x enterprise value) and by their capital expenditures (which exceeded cash flow by nearly 5 times in 2012). As I written about in the past, the E&P junior landscape is littered with companies that have spent beyond their means until they could spend no more.

To avoid that fate Gastar needs to keep showing success. The Marcellus land has done just that. I have seen estimates that their Western “super-rich” block of land in the Marcellus would be worth the current enterprise value alone based on current sales metric. If that is indeed the case, the Hunton provides significant upside to the stock. If the third and fourth Hunton wells turn out to be anywhere near as successful as the second, I would expect the share price to run much higher.

7/22/2013

Gastar looking to expand in Oklahoma:::

Gastar Exploration Ltd are rumoured to be in negotiations to aquire london listed smallcap Nostra Terra Oil & Gas,it is thought that the company are keen to expand their interests in Oklahoma and Texas,where Nostra have minority stakes.

A spokesman at Gastar neither confirmed or denied the rumour but did reveal that the company are actively trying to build their asset bases in the quoted states this year.Gastar have recently disclosed an agreement to sell “undeveloped” leases in Oklahoma to an undisclosed third party for about $62.0 million in cash and will use the funds to further increase stakes in “developed” leases in the state.

Thanks for the comment – i didn’t even know of Nostra Terra but I’ve started to take a look at the name

Hey Lsigurd great blog dude,i am a long term holder of GST and also heard rumours lately from some pals in canada that we are about to get more leases around the hunton.The company nostra terra are right in where we want to be and an easy buyout option for us,they also got some assets in texas and colarado we could develop on low capex.

Brad