Taking Advantage of the REIT Sell-off

For some time now I have wanted to take advantage of companies that will benefit from improving credit conditions. Yet since the beginning of the year the steep run-up in these stocks has led me to limit my purchases to a small position in Arbor Realty (ABR) and a short lived position in RAIT Financial (RAS).

Thus I am pleased that we are finally seeing a significant correction in these names. The correction is being brought about by the rise in interest rates, a pullback in the credit markets (here and here), my interpretation of which is that it has been driven by a temporary oversupply and of course fears of the Fed, and investors inability to distinguish between more unconventional REIT structures that are not sensitive to increases in interest rates and simple agency and non-agency mortgage REITs that are. The companies that I am interested in are mostly agnostic to interest rate increases and in some cases will actually benefit from a rise in rates, but that hasn’t stopped them from selling off.

In the last three weeks I have taken advantage of the sell-off by buying shares in the following names:

- New Residential (NRZ)

- PennyMac Mortgage (PMT)

- Northstar Realty (NRF)

New Residential

The first company on the list is not a new one. I have owned Newcastle Investments, from which New Residential was spun-of in the middle of May, for about a year and a half now. New Residential got hit very hard by the REIT sell-off, falling from a high of above $7 to just a few cents over $6. Unfortunately this was a situation where $6.75 looked good to me, $6.50 looked better and $6.25 even better, so I was buying all the way down and, rather than catching the bottom, I caught a falling knife, and ended up with an average a cost of around $6.55.

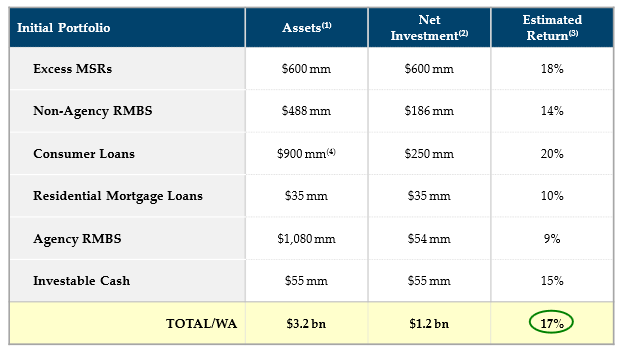

There is a pretty good summary of New Residential’s assets in this article. Below I have snipped a slide from the company that summarizes their assets and net investments in each area.

About half of the net investments are mortgage servicing rights (MSRs). It’s hard to believe I’ve been talking about MSR’s for almost a year and a half now and still feel there is opportunity, but I do. As I’ve said multiple times, the MSR’s being written today are some of the highest quality servicing rights ever. The loans are being originated at an interest rate trough where the risk of refinancing is low, with extremely strict underwriting criteria so the risk of default is low, and at a time when house prices have passed their trough and are beginning the up-swing. I think we are all going to be surprised by just how long these loans (and necessarily their corresponding MSRs) stay on the books.

The rest of the assets are comprised of commercial loans and non-agency RMBS, which are going to be more sensitive to improvements in the economy (which will improve the condition of the underlying collateral which has been bought at a discount to par) than the rise in interest rates. While the company does have a relatively large balance sheet position in agency CMBS, it makes up only a small amount of the company’s equity because of the leverage involved.

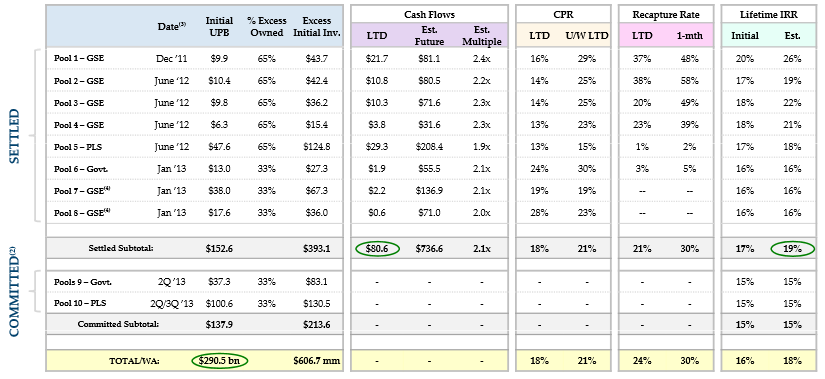

Since mortgage servicing assets make up such a big portion of the company’s investments and since they are the primary reason I have taken such a large position in New Residential, I want to talk a bit more about the company’s mortgage servicing portfolio. The 7th slide of the company’s May Presentation provides details.

The key metrics to focus on are the CPR, which is the prepayment rate and the recapture rate. Between the two of these you can get a sense of how long mortgage servicing assets are staying on the books and how good the company (through their servicing partner Nationstar) is at recapturing those loans when they are prepaid.

What I think is particularly noteworthy about the table is the recapture rate. I remember reading Nationstar’s prospectus last year (Nationstar is, of course, the partner of New Residential and manages the actual servicing of the mortgages involved), that their projection was for a 35% recapture rate, and that they suggested that if everything went right they may be able to push that level up to 50%. Its impressive that they have met and, in the case of the second pool, exceeded that rate.

Unlike other mortgage assets, the value of mortgage servicing rights increases as interest rates rise because the probability that the loan refinances diminishes. The longer that the mortgage servicing right stays on the books, the longer that New Residential will collect the fee income. Given that we’ve had years and years of lower interest rates, I think there is a reasonable chance that there is an upside surprise to just how long existing mortgage servicing rights generate fees. Even though the mortgage servicing right asset has received much more attention over the last year than when I first began investing in them, I think that investors are still underestimating their longevity.

With New Residential trading down 15% from its peak, and at a level that offers about a 10% dividend, I believe the sell-off offered an excellent opportunity to add to my position in the stock. So I did. Its now the largest position in my portfolio.

PennyMac Mortgage

I owe this idea to Bigenergybull, an investorsvillage poster who I was told will soon be changing his name to BigREITbull, which doesn’t have quite the same ring to it.

PennyMac Mortgage (PMT) operates three different businesses: they buy distressed real estate loans and MBS, they originate correspondent loans, and they hold on to the mortgage servicing rights that they receive from the loans that they originate.

Two of these businesses (mortgage servicing rights and the distressed real estate) will benefit from an improving economy, while mortgage servicing rights will also benefit directly from rising rates. And while one might think that the correspondent business would be hurt by lower volumes, a more nuanced view of the business suggests that the impact might be mitigated: lower volumes and margins on small banks and brokers will force them to sell more of their mortgage servicing rights in order to cover the cash flow requirements of the origination business. While the total number of loans being originated will decline, the share of loans through the correspondent segment should increase. I also looks at PennyMac’s correspondent business as more of a platform to accumulate assets than a stand-alone profit center. In addition to the mortgage servicing rights that the company takes in through the business, they have been expanding their lending to jumbo loans, which I expect they will begin to securitize privately (keeping an equity stake) once the market allows.

The mortgage servicing portfolio at PennyMac is only about 10% of assets. Its not nearly the size of the New Residential operation, and future growth will depend on loans originated from the correspondent business. Admittedly the company capitalizes their servicing rights rather aggressively at 100 basis points, while most competitors I’ve seen are closer to the 75 basis point range. So they are booking a good chunk of the potential upside I see in servicing up front.

The larger opportunity at PennyMac comes from the distressed loan business. Distressed loans and real estate owned (REO owned by PennyMac refers to distressed loans that have worked their way through to foreclosure) make up over 50% of assets at the company.

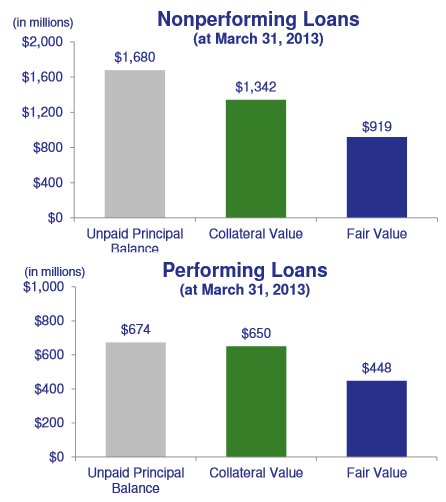

The distressed assets have some hidden value. At the Keefe, Bruyette and Woods conference management showed the following slide pointing to the carrying value of their assets. The company carries these assets 68% of current collateral value, with the clarification that by current collateral value they are referring to the appraised market prices of the homes.

If you do the math, there is $620mm of embedded value in the distressed portfolio – or almost $10 per share not included in book.

The other interesting business that PennyMac is dipping their toes into is jumbo loan originations. While this business is still small (the company originated $8 million of jumbo loans in the first quarter, versus $5 billion in total volume), it will grow with improvement of the housing market, and the real opportunity is that once (if?) the private label market heals, the company can begin to securitize these loans, taking equity stakes in home loans near the bottom of the market.

Admittedly PennyMac is a bit of grab-bag of mortgage businesses, but I don’t think this is a bad time to be grab-bagging the mortgage industry, particularly where the businesses involved are not sensitive to higher rates. I expect to recognize returns from PennyMac through the dividend (which at the current share price is about 10%) with potentially further gains realized as the market recognizes that this company is not akin to other mortgage REITs and that there is significant value not recognized in book.

NorthStar Realty

NorthStar Realty (NRF) is a bit different then the two aforementioned companies in that NorthStar generates a significant portion of its income from commercial real estate loans. NorthStar, however, is similar to the aforementioned companies in that they have been hit rather hard for their association with the term ‘mortgage REIT’ and the extrapolation that higher rates will be negative for the company, even while their assets are only minimally exposed to the impact of higher rates (on the most recent conference call the company said that a 100 basis point move in the 10-year would make zero difference to their cash available for distribution).

Northstar is a hodge-podge of commercial real estate lending businesses. They generate income from their owned CRE properties, which include healthcare (skilled nursing and home care facilities), lease properties (which are 77% office space), and more recently, manufactured housing. They generate fees and equity distributions on their legacy CRE loan CDOs. They generate some minimal fee income on the CMBS CDOs but most of these are performing quite badly. They have created three non-tradable REIT vehicles, two focused on commercial real estate and one focused on health care that offer their product to retail investors and to which NorthStar collects fee income. And they are opportunistic, as is witnessed by a recent investment in a private equity portfolio of commercial real estate that is expected to be accretive to cash flow by 6-7c in 2013 and 16-18c in 2014.

The investment case for NorthStar is the yield (which is around 10% at the current stock price) with the potential for price appreciation through one of the following events.

- A spin-off of fee generating assets

- Further clarity of returns on their more opaque investments such as manufactured homes and private equity interests

- Collapse of their CMBS CDO’s to free up cash for accreditive investment

- Accretive gains from a recently acquired private equity portfolio

The number of moving parts at NorthStar justifies a more detailed post in the future where I will dive further into the details. Each of the above points is worthy of a few paragraphs.

In addition to these specific events, NorthStar is also somewhat of a generic bet on the ability of management to create opportunities in commercial lending. A similar statement could be made for all three of these names. While each name has been chosen for the make-up of their portfolio, they have also been chosen for the quality of their management teams and I expect that as the economy and credit makrets continue to heal these teams will come up with more ways to create value for holders of the equity.

mREIT investing is the space I play in almost exclusively so I can help you out here. PMT and NRZ look like standard hybrid mREITS to me, and as such are just as exposed to interest risk as the rest of them. Just like other mREITS, it’s all about their hedging skills. A warehoused portfolio of loans in the pipeline before securitization is very very exposed to interest risk.

If you want hybrids I suggest MITT and MTGE.

On NRF I have no clue. Believe me I’ve tried in the past to value it, but was unable to pierce the heavy derivative veil. It’s remains a black box to me, much like PETAX, that spits put dividends. But I can’t estimate it’s risk due to heavy opaque derivative exposure, so I can’t value it and I try not to buy what I’m incapable of valuing. I will be very interested to read your follow up article on NRF, perhaps after reading that it won’t be such a mysterious black box to me.

############################

A little update in case you’re interested. I recall that we both bought coal stocks around the same time. My update is tat I scored a 2x bagger on the JRCC call options, broke even on BTU shares, and am now deeply underwater with 36% unrealized losses on ANR. ANR is my last remaining coal position and I plan to grumpily wait it out for years if necessary to at least a 10% gain.

Taymere NRZ is a mreit. But it’s portfolio of MBS securities is just used as a qualifier for REIT status with the IRS. If you follow that closely then you would have noticed based on the presentation for NRZ that a 100 bps change in rates adds another potential 2 to 5 cents in income. Since that presentation rates have increased by that amount. Even though they paid a divvy of .07 for the qtr that represented only half the qtr. and last as money committed gets used then this .07 can easily turn into .14 to .17. Last if compared to HLSS a supported yield of 7% is attainable. But your point of NRZ being a mreit is true. But to add only for REIT qualification. The bulk of the income will come from MSR’s and the consumer loan portfolios. Lsigurd is just fully right to notice this dislocation by the market.

Thanks Kookie, I now agree that NRZ is very exposed to MSR, and should be valued differently on interest rate risk than PMT and the rest of the hybrid mREITs. But just how should that valuation be made? Although I follow mREITs closely I am new to MSR valuation so please bear with me here. The 100BP change that you refer to for NRZ is on short term rates, rates indexed to LIBOR or such, and therefore to be held down firmly by the Fed for several more years, and not relevant to the current mREIT taper talk sell off. That 100bp shift is not the standard instantaneous parallel shift in rates that mREITS usually disclose in their interest rate sensitivity tables. What is more relevant to the current taper talk interest rate risk valuation of mREITS is mid term rates such as 10 year UST yields in the the “bear steepener” scenario.

I don’t see any disclosure from NRZ about how their earnings would respond in a bear steepener scenario, but they do show the BV effects of discount rate changes on p.36 of their 10Q. Rising 10 year UST yields would increase the discount rate for from the current ~17.5% that NRZ uses (p.36 of 10Q). Perhaps slowing prepayments would counteract and offset that BV drop, and that is the basis of Lsigurd’s “…mostly agnostic to interest rate increases…” claim about NRZ. Point taken and now understood, thanks for the discussion because without discussion investing is boring for me.

Thanks for the comments from both of you, its been a good discussion for me too. I have some points to make on PMT in response to you Taymere but i don’t have access to my notes as I’m away so I’ll have to wait to respond until early next week.

I guess since rates have moved, then there is no reason for me to speculate on the effect. Results will be out here in a few weeks. But per say the slowing of prepayments have a larger impact than recapture. Plus if the seasoning of the new portfolios come out as the previous ones then we could see a 14% CPR. Or in dollars terms another 12 to 17 million increase. But everything they presented is not truthfully scalar in terms so a mix of slowing prepayments and a higher recapture will result into what will be presented. Another jewel is in the consumer loans. An expansion in this area could be material.

“Robbins Arroyo is investigating claims of self-dealing by PMT’s Chairman and CEO, Stanford L. Kurland. Specifically, the firm is investigating whether Kurland has benefited at PMT’s expense…” http://www.theglobeandmail.com/globe-investor/news-sources/?mid=PRNEWS.20130703.LA42838

I saw this but I’m not too worried. They’ve had a few of these lately since the NYT article.

But do you trust Kurland? I don’t, I think he’s dishonest and that he was a bad actor at Countrywide and still is. Countrywide was a den of thieves. So regardless of whether the courts sanction Kurland I wouldn’t invest with in something he controls.

Really? See to me, everything I’ve read about Kurland suggests he’s a very hardworking, detailed oriented guy, and that the problems at Countrywide had nothing to do with him. In fact, I remember reading in one book in particular, “All the Devils are Here” that Kurland was one of the view voices of sanity, seeing that the housing market had gotten out of control in the mid 2000s, and that his views were minimized by Mozilla’s quest for size and power.

What specific evidence are you referring to when you call Kurland dishonest?

I am not a former Countrywide insider with direct knowledge, and I haven’t read the book that you refer to, but the inferences are quite easy to draw. Birds of a dishonest feather flock together. Kurland worked with Mozillo for 30 years and only left in 2006. Kurland hired Stephen Brandt, who is the guy who ran the politically bribing “Friends of Angelo” program at Countrywide, to be his Managing Director of Retail Production at PMT. He hired his former coworkers to form a new den of thieves after leaving his former den of thieves. They lied through their teeth about representations and warranties, do you really believe that Kurland was ignorant of this deception? Look at the PMT roster, it’s heavily stacked with former Countrywide leadership. Countrywide is empty, all the devils are at PMT now. What is a man who surrounds himself with crooks and liars is most likely to be?

The following article spells it out

http://finance.fortune.cnn.com/tag/countrywide/

I do not doubt that he is hard working, but is he working honestly? Management dishonesty is a deal breaker for me, if I don’t trust them I don’t buy. It’s too easy to cook the books and avoid detection for years, my only protection against accounting control fraud is to invest with management that is honest.

Thanks for the link to the article. I wasn’t aware of Brandt’s history. Nothing here is changing my mind on investing in PMT though. Still sounds to me like Kurland is guilty by association. I like the ventures he’s embarked on at PMT, I like the hidden value in the distressed assets, I like the mortgage servicing rights, and I think the stock is being sold off because its a mortgage REIT without recognition that 2 of its 3 businesses are positively correlated to higher rates. I plan to hold onto my position.

You’re welcome. I loved Friday’s sell off, I added more MTGE and AGNC and opened a brand new EFC position. Are you familiar with EFC mlp? EFC has a substantial short TBA position that they use for hedging, and that hedge has been banking major coin lately. They give monthly BV updates and have thus far sailed through the bear steepener with BV unscathed. Their May 31st intermin BV estimate was $24.74 and their closing price Friday was $21.85, a huge margin of safety.

I admittedly haven’t studied the more traditional mREITs that buy MBS so any insights you have into names like MTGE and AGNC would be appreciated. The little I’ve looked at them made me feel a bit lost evaluating the various securities they purchase and how each is impacted by rates. How do you value them, is it simply a book value calc or is it more nuanced?

Sorry for the delayed response, I started to think up a long treatise reply which was taking awhile and my have never gotten sent so I decided to keep it simple.

I use a near term economic return criteria. I assume that I’ll collect one dividend then exit at current intermin BV. I don’t adjust my BV estimate for the div because the spread income is covering the div. Estimating current BV and estimating what div will be paid are the tricky parts. I use Merill Ross from Wunderlich securities, analyst reports from Credit Suisse and Stern Agee to come up with my estimates. (expected BV+expected div)/(current price) > 1.07 is my threshhold to consider buying. I have a spreadsheet with my current estimates for the 9 mREITS that I am paying attention to right now, give me your email address and I’ll send it as an attachment. Current prices and my estimates place the near term economic return > 1.2 in many cases, I am thrilled with the current opportunity and have gone from being 1/3 in cash to being on margin.

Merill Ross is the best analyst, she’ll send you her weekly reports even if you’re not a Wunderlich client. She recently threw in the towel on the whole sector, she no longer rates anything as buy, and she said the possibility was high for one or more mREITS to go belly up this week in a margin call induced forced liquidation death spiral. While I respect her views I also consider that type of analyst capitulation to be a sign of the bottom in prices.

Thanks for the detailed description of your methods. My email is liverless at hotmail.ca

Agree with the premise on NRZ and PMT with respect to MSR and distressed asset holdings – these will improve with a rising economy and interest rates. MSR values are highly subjective as the valuations involve a number of assumption inputs, including but not limited to, cost of servicing (which has been trending higher due to higher compliance costs), mortgage interest rates (not short term rates, but generally tied to 3o-yr mortgage rates), future expected prepayment and default rates, length of time to foreclose on houses, advance rates and cost of advance funding just to name a few factors. Not all of these factors move in the same direction as economic conditions change, but the key factors are the prepayment and default rates. As prepayments slow, MSR values go higher for the simple reason that the MSR asset will generate the servicing fee for a longer duration. When defaults occur, the MSR generally does not generate or accrue servicing fees on those loans, so fewer defaults means more revenue generating loans in the MSR pool. When the economy (and house prices) improve, defaults generally slow and there is a lot of evidence of improvement out there right now. When mortgage interest rates rise, there are fewer prepayments all else equal, and we’re seeing a sharp rise in the Fannie/Freddie 30-year rates. So on the basis of MSR valuations, and despite the opaque and subjective nature of these valuations, we should see improvements in the asset. I like PMT and NRZ and have positions in both. I think the sell-off was based primarily on an industry grouping rather than a fundamental view of the business and underlying assets.