Waiting for Novus and adding more Canadian Oil Juniors to the Portfolio (Pinecrest, Palliser)

I have been adding more Canadian oil junior positions.

If you recall, I started my endeavor into the domestic oils a month and a half ago, when I purchased Lightstream Energy and Penn West. That didn’t last long; I quickly jettisoned those names after doing more research, deciding that neither was particularly cheap, and recognizing that there were other, smaller names that were more attractive.

The first names I went with was Novus Energy and that was followed by Longview Exploration, and Rock Energy. Of the three I felt the most comfortable with Novus and made that position the largest. This week, an article came out in a Hong Kong paper (I believe if was the Economic Times) that Novus was about to be taken out by a Chinese company called Yanchang Petroleum (you can access the translated article here, and one version of the original here). The news was clearly leaked, Novus wasn’t ready for it to be released, and the stock has remained halted for the last 3 days.

If the article is to be believed, the value of the transaction is going to be a windfall for shareholders. According to the article the purchase price is $500 million, which after subtracting debt and accounting for stock options would still mean over $2 per share. Given that Novus is an 8% position for me, this would be a huge gain.

I’m not going to spend much time speculating on the validity of the article. It seems that pretty much everyone who owns Novus believes the takeover price and everyone who doesn’t thinks its a mistake. I would only point out that the article has details like the termination fee, which seem unlikely to have been made up, that the transaction would value the company at about $120,000 per flowing boe, which is pretty much what Equal got for their Lochend Cardium (a number of other recent transactions in this range are tabled by Andrew McCreath on this BNN segment), and that the metrics are pretty consistent with what Raging River is currently trading at (Raging River is a Viking producer that I used for a peer comparison in my write-up). So we’ll see.

The news gave me the courage to step up my bet into unloved Canadian oil juniors with two new names; Pinecrest Energy (PRY.v) and Palliser Oil and Gas (PXL.v). These are two quite different stories but they are held together by the common thread of being beaten down and, in my opinion, quite cheap. For the rest of this post I’m going to focus on Pinecrest.

Pinecrest Energy

At 42c Pinecrest has a market capitalization of $90 million and an enterprise value of $210 million. Based on last quarters production (3,615boe/d, with 97% of that being oil, and $16.4 million in operating cash flow) the stock trades at $58,000 per flowing boe and 3x EV/EBITDA.

This used to be a $3 stock when everyone was in love with carbonates and their hz multifrac potential. But the reality of steep declines and long tails to recover the well NPV kicked in, and it became clear that a steep growth trajectory was not achievable through drilling without accumulating a significant debt load. It didn’t help that Pinecrest muddled through a failed merger with Spartan.

The opportunity, I think, is that with rose colored glasses taken off, investors are ignoring the potential incremental net asset value that can be attained through the implementation of waterflood. While the return on investment of Slave Point wells is only slightly better than marginal (between 28% if you use Pinecrest’s type curve and 52% if you use the type curve of their new open hole completion technique – All this information is in Pinecrest’s corporate presentation), the returns for waterflood appear to be much higher. Below is a snipit I took of waterflood economics from the latest Pinecrest presentatio:

Now if I am interpreting this correctly, the above table is estimating that the incremental capital required for waterflood is $2 million per section (assuming 5 wells cost $3.7 million to drill and the total section capital as specified at $20.5 million), and that the return on investment for the section is between 67% and 240%. In a footnote its stated that the estimates are based off of the Pinecrest type curve well, so it should be compared against a pre-waterflood return on investment of 28%.

Now if I am interpreting this correctly, the above table is estimating that the incremental capital required for waterflood is $2 million per section (assuming 5 wells cost $3.7 million to drill and the total section capital as specified at $20.5 million), and that the return on investment for the section is between 67% and 240%. In a footnote its stated that the estimates are based off of the Pinecrest type curve well, so it should be compared against a pre-waterflood return on investment of 28%.

This is a lot of incremental value for a small amount of extra capital. Maybe I am misinterpreting the table, but if I’m not, the company can generate a lot of extra upside by spending a few extra dollars.

Waterflood made up 0% of proved and only 3% of proved plus probable reserves in the 2012 reserve report. So none of this upside is reflected in the NAV.

Will it work?

That’s the big question. And to some extent we just have to wait and see. But the evidence available is constructive.

First of all there are the historic waterflood results from Slave Point. These pools were drilled with mostly vertical wells, and likely had a higher permeability than the areas that Pinecrest is drilling, so admittedly the analogy is not exact. Still it is a worthwhile data point to note that waterflood resulted in a 2x to 3x production increase and a 50% to 133% increase in recoverable reserves.

Second, there is an interesting slide from the last Pinecrest corporate presentation that details the response of existing wells from the frac-ing of adjacent wells (slide 16). This slide could easily be misconstrued; it shows a short blip in production followed by the continuation of the low production trend. However, what the company is trying to convey is the communication between the offsetting wells. The frac-ing of a new well creates a short lived spike in pressure, and the corresponding spike in production at the adjacent well is evidence that this pressure is continuous from one well to the other. A waterflood is simply a more sustained version of such pressure support, and so a similar response could be expected. One of the biggest question with waterflood is whether there is reservoir continuity, and here is the evidence that there is.

Third, waterflood is has been proven to work in these tight rocks elsewhere. Perhaps the best example is Swan Hills, where Arcan has been successfully waterflooding their Deer Mountain Unit, which is a carbonate rock just like Slave Point. But more generally, tight rock in the Shaunovan, Bakken, and Cardium are all being seen as responsive to waterflood.

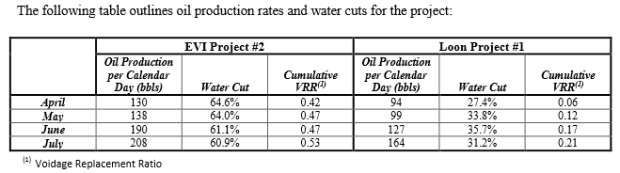

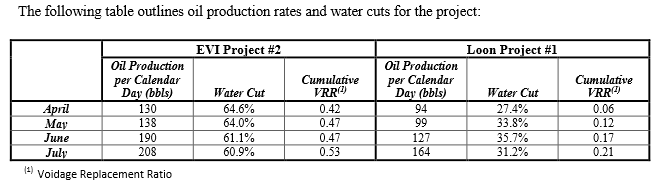

Fourth, the early evidence is promising. In their second quarter update Pinecrest provided the following table demonstrating the response to waterflood at their two pilot projects. In both cases production is up more than 50% in four months, continuing to increase, and within the range of the company’s expectations. Full response isn’t expect until 12 months.

Conclusion

Conclusion

Pinecrest isn’t a perfect story. It doesn’t have me salivating the way Novus did, where I saw a stock so mispriced that I didn’t feel there was too much in the way of downside, only a question of how much upside. With Pinecrest the company’s debt levels are fairly high, the decline on their primary production is steep, their wells are expensive to drill and they are running up against the limits on their bank line. But the stock has also fallen 90% from its highs. There is a point where you can start to ask the question, if the company survives as a going concern, is it all in the stock? I think we are probably close, if not at, that point. There is certainly zero upside being baked in for the waterflood. In my opinion, some positive results and the stock will quickly move back to at least 60 cents, if not higher.

Extensive discussion with interests on your PRY at http://premium.investorvillage.com/mbthread.asp?mb=17397&nhValue=16114&nmValue=16154&dValue=1&tid=13086664&showall=1

Does the change in the business plan positively or negatively effect your opinion on PRY? Seems to me like it had to happen.

Yeah I would say its constructive in the long run. I think it will be interesting to see what the stock does tomorrow. I mean, clearly the guidance reduction is massive, but we all knew it was coming, and the 3,100-3,400 exit number is flat to slightly up compared to Q3 on $25mm in 2nd half capex.

Wish that they made the Peters and Co presentation tomorrow available to the public. Would be interesting to hear what they say. I guess going into 2014 they will have the cost reductions kicking in, 7 waterfloods with production inclining and 4 more that they currently have identified for implementation. Just on the back of those 11 floods they should be able to grow a bit yoy for very little capital.

I think they did. The presentation on their website is Sept 10th. Also gives a little more detail on waterflood but it appears to just be July numbers which we already knew.

Hi,

Curious what you thought of PRY’s most recent Q. Are you revising your estimates, and if so in what way?

I did reduce my position some (I think it was about 10-15%) after the quarter. I tweeted this at the time. But really, I reduced as much as anything because the stock didn’t go down and I really thought it should have. It wasn’t a great quarter but really we have to wait till next year to find out more about the waterflood results. It’s really a wait and see story here. I probably got in too early but one never knows how quickly these things will go.

Hi,

Curious what you thought of PRY’s most recent Q. Are you revising your strategy and if so in what way.

Thanks