Another Leveraged Play: Dex Media

I’ve had a position in Yellow Media (Y.to), for a number of months, but until this week I had not dived into its American counterpart Dex Media (DXM). The reason was timing; I didn’t get the chance to look seriously at the company until the middle of April and shortly after I looked Kyle Bass recommended the stock at Ira Sohn, the stock price took off, and I was reluctant to chase it.

I’ve waited patiently since then thinking that the stock would come down once the shine wore off. This week I was rewarded and able to pull the trigger in the $14’s.

Before I go any further on this one let me just give a hat tip to Glen Bradford for all the work that he has done. Glen has discussed Dex Media and its predecessor companies Dex One and SuperMedia in detail on his website and on Seeking Alpha, and much of my own research started by reading his work.

The story at Dex Media is, of course, not unlike Yellow Media, but its also quite similar to YRC Worldwide, and fits in with my big idea for the year of investing in leveraged companies while the sun still shines. To illustrate the comparison to YRC Worldwide, when I bought the stock it was a $50 million dollar equity with over $1.3 billion in debt. You had a tiny sliver of equity that stood to act in a highly leveraged way if things played out right. Same thing with Dex Media. The equity currently sits at a little over $150 million. The company has debt of over $3 billion.

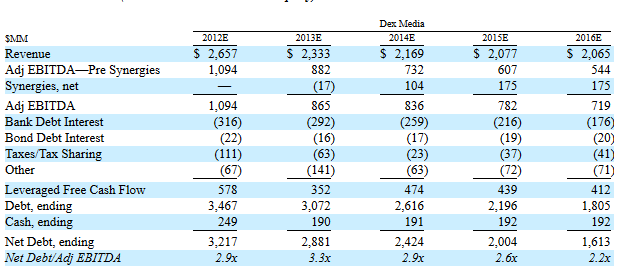

Unlike YRC Worldwide (but much the same as Yellow Media) the company has a free cash flow forecast that is impressive (but also declining). Take a look at the table below, from the Supermedia/Dex One merger prospectus filed February 8th. The forecast was compiled from internal management pre-merger forecasts by Supermedia and Dex One. When reviewing the numbers keep in mind that the combined Dex Media entity has 17.1 million shares outstanding.

Based on the 2013 estimates the entire company is trading at about 3.9x EBITDA. This could be attractive in its own right, but the print business (phone books) is in terminal decline and there are questions that need to be answered with respect to longer-term sustainability of the on-line business, so it is probably not unreasonable given the state of affairs. What is more interesting is that because the equity is a literal sliver of the enterprise value the impact of debt repayment from free cash flow results in large increases to the equity even at a constant EV/EBITDA ratio.

Follow me through a little thought experiment. Let’s say that the company can meet the earnings forecast laid out above. Lets also make the assumption that investors will continue to value the company at a distressed 3.9x EV/EBITDA level. On those assumptions, debt would be paid down by $350 million and the value of the equity would triple in the next year. And so on and so on.

The only two ways that this doesn’t play out are if:

- Investors continually assign a lower EV/EBITDA number to the company has time goes on

- The forecast assumptions are optimistic and business declines at a faster pace than anticipated

The only way I can see the first one happening is if the second one does. If the company shows the kind of stabilization suggested by the forecast, and at the same time is reducing debt by 15-20% per year, I can’t conceive of the EBITDA multiple actually declining.

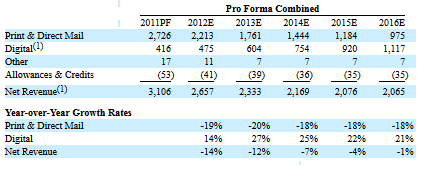

So it all rests on the outlook. Here is the revenue growth of Dex Media’s digital business, and the declines in the print business, that the forecast is based on.

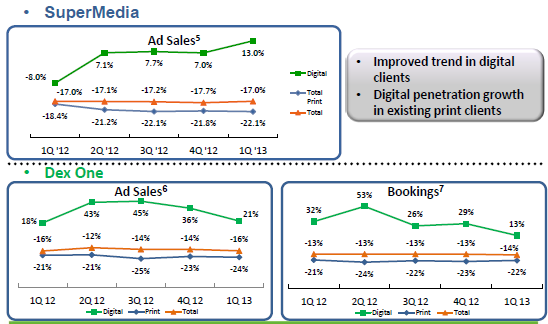

Really this is such a similar story to Yellow Media, a declining print business and a new, growing but not entirely trusted digital business, that I don’t want to repeat myself again here. The comments I made in my write-up of Yellow apply equally here. I don’t think its a beneficial exercise to feign expertise and try to predict the evolution of the digital business. Instead let’s focus on how things have played out so far:

Really this is such a similar story to Yellow Media, a declining print business and a new, growing but not entirely trusted digital business, that I don’t want to repeat myself again here. The comments I made in my write-up of Yellow apply equally here. I don’t think its a beneficial exercise to feign expertise and try to predict the evolution of the digital business. Instead let’s focus on how things have played out so far:

It looks like they are being somewhat aggressive on their forecast compared to the historical precedent, though their forecast is in-line with what Yellow Media has already been achieving, so it is by no means unrealistic. My plan will be to simply watch the numbers over the next number of quarters and see how things play out.

The key metrics going forward are the growth rates of print and digital. These are the numbers that you want to watch when the quarter comes out on Wednesday, and what to focus on going forward. Are declines in print and is growth in digital sticking to plan? If they are, then this stock is going to be a good one.

I don’t like Dex Media quite to the extent of Yellow Media, which is partly because the restructuring left Yellow Media with a lower debt level, partly because I haven’t done the work on Dex that I did on Yellow, and probably partly because of home bias. Right now its a 4% position, and I look at it as an excellent candidate for my strategy of doing more of what’s working, as I will add to the stock as the story plays out. Also as usual, I give myself a 15-20% cushion to the downside and then I humbly admit my mistake and start to lighten up.

Any thoughts on going long the DexMedia debt?

My canadian brokerage accounts dont easily allow me to do that (which is something I really have to get around to changing) so I haven’t really considered it but no question there is upside there, particularly on the subordinated side. I like the equity because I am still in the stage of my life where I am trying to accumulate capital and this is the sort of multi-bag potential stock that can accelerate that.

hi

i really appreciatte your work at this blog

if you like leveraged comapnies you should look at WTW

http://gannonandhoangoninvesting.com/blog/2013/8/3/what-led-to-the-weight-watchers-wtw-purchase

😉