Aercap – full value of ILFC acquisition is not in the stock

I got the idea for Aercap (AER) after listening to a Bloomberg Taking Stock podcast with Martin Sass. Sass recommended Aercap along with American Airlines (another company I am in the process of looking at) as he’s gone from hate to love on the airline industry. He called Aercap’s deal to acquire ILFC “transformative”, pointing out that it “will make Aercap Holdings the #1 aircraft leasing company in the world”, and yet that “it’s trading at only 8x earnings.”

On Thursday I tweeted a few reasons justifying my position in Aercap. You want to read these from the bottom up.

In this post I am going to follow up on that tweet with a more detailed description of my investment thesis.

What they do

Aercap is an aircraft leasing company. Its a pretty simple business; they purchase aircraft and then lease them out to carriers. They profit from the spread between the lease rate and their cost of capital. In many ways its not that different than an apartment REIT or commercial REIT. Its just that in the case of Aircap, the asset being rented out is a plane.

In the past Aercap has been a smaller second-tier player in the business. But this changed in December when the company purchased ILFC, the aircraft leasing business of AIG. With that purchase Aercap will become the #2 platform in the business behind GECAS, which is owned by GE, is the other large player.

There are a number of benefits that accrue from the purchase of ILFC:

- According to the company, they purchased ILFC at $6 billion discount to the independent fair value assessment. The stock has traded up from $23 to $40 since the purchase date, so say about $3.6 billion in market cap has been added since that time.

- The transaction is accretive to earnings. The company expects to generate earnings from the combined entity of $1 billion, which works out to about $4.70 per share.

- There is further embedded value in the ILFC order book. This is what Aercap had to say about the order book, which they called “the crown jewel” at one point on the acquisition conference call.

And turning to the order book, we believe that the order book is extremely attractive as I mentioned. The delivery slots is crucial. These are fantastic delivery slots to get them at this point. If you go to the OEMs today, it will be decade later on average before you get this stuff. If you try to order 350s, your average delivery stream will be probably 2023, 2024, same for 787. That results in massive price escalation. These are at a perfect spot in the delivery cycle, right at the front of it, the pricing is exceptionally attractive and it’s the most in demand aircraft in the world. So, we feel very good about that.

- Because of deals that ILFC was forced to get done in the dour days of 2009, they have a much higher cost of capital than Aercap. On the conference call management said that Aercap’s average debt cost is around 4%, whereas ILFC is around 6%. Over time Aercap should be able to refinance this debt at rates closer to the former. If you could get half of the ILFC debt down to a 4% average, that would save $200 million in interest costs annually, or about $1 per share.

- There could be the opportunity to generate some immediate gains from asset sales of some of ILFC’s older aircraft. The company suggested that would be selling about $1 billion book value of aircraft once the deal is complete. Given the hefty discount to book that they paid, this may result in gains on sale that will increase earnings in the near term.

- ILFC assets will be moved to Ireland where Aercap resides, and there be subjected to a fairly low tax rate regime, with expected income taxes of around 12%

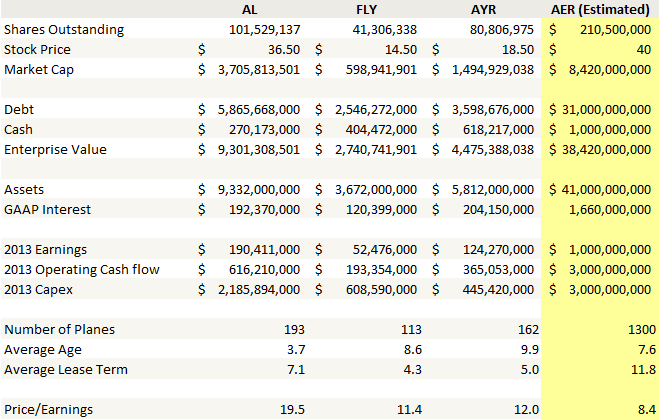

How does Aercap compare to the competition?

Doing a comparison with competitors is spotty because GECAS is owned by GE and some of the other players are private. Nevertheless the results allow for some conclusions. Here is the comp.

What to expect

Given Aircap’s size (they are either going to be the leading or next to leading platform) one would expect Aircap to trade at a premium to its smaller competition. But on an earnings basis Aercap trades at a discount to its peers.

Now of course much of this is because the deal has yet to be consummated and those earnings have yet to be realized. But I don’t think the hurdle is too high; I expect that in the next 6-12 months as the two businesses are integrated, the comfort level with the $4+ earnings run rate should grow and the company should begin to trade in-line or even at a premium to these peers. This would suggest a stock price in the $60 range is reasonable.

What is going to make or break Aircap is whether they can smoothly integrate the ILFC assets. If they can, and they can prove that their target earnings of $1 billion are achievable, then the stock is probably going to move significantly higher.

Risk and reward

The biggest risk here in my opinion is simply a general economic downturn. Aircraft leases accounting for 30.1% of revenue expire between 2013 and 2016. While this actually compares quite favorably with their competitors (Fly Leasing and Aircastle have 55% and 47% of their leases expiring in the same time frame respectively), it nevertheless remains significant, and whether they would be able to get the same terms in a declining economy is questionable.

The company also has a significant amount of aircraft leased out to emerging market customers (47% as of year end, albeit this would be pre-ILFC), which increases their leverage to a general malaise even further.

Moreover, obviously the company is extremely dependent on favorable financing. The requirement of significant capital to fund their purchases is #1 on the list of risk factors in the company’s annual filings. A tightening of credit conditions would be negative to their outlook.

But things have been good for the airline industry for the past number of years. As I mentioned in my post on Air Canada, we have had 4 straight years of improving profitability for the airlines, and 2014 is so far shaping up to be a 6th. The credit quality of the lessees is better than it has been for some time.

Apart from something bad taking place in the economy, this looks to me like one of those stories where we have a short-term mispricing brought on by a transformative acquisition that hasn’t been fully digested by the market yet. How many people look at the stock, see that its risen nearly 100% ILFC was acquired, and immediately think it has to be all priced in? Yet I don’t think it is.

I took a large position here, its nearly 6%, which is unusual for me but shows my comfort level with owning the stock below $40. I hope to see $60 by the end of the year.

Just to confirm, the numbers listed under AER(estimated) are estimates for post-acquisition combined AER+ILFC? Also you touched on financing being one of the risks. Any idea, how much is the debt compared to cashflow? How much earnings have to decline before debt servicing becomes a problem? Most importantly, how does Enterprise value compare to Intrinsic value?

This is my first post on your blog. I must thank you for what you are doing — share your ideas for everyone to benefit from.

The numbers are for the combined entity. They come from CCs and presentations. They expect operating cash flow of $3b. I don’t know what intrinsic value means.