Yet another airline stock: Transat AT

I made a number of portfolio changes today, reducing positions in a few stocks that haven’t been working out as I had hoped. I sold the last of Pacific Ethanol, sold out of Syncora and reduced my position in Chipmos. In part I made these changes to raise cash because I have been adding to my position in Transat A.T.

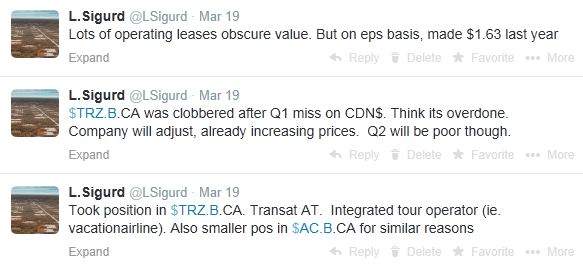

I first bought Transat A.T (TRZ.B) on March 19th and have added to it a few times since then. I made the following tweets at the time (read from bottom to top):

What they do

Transat provides both chartered and scheduled flights originating in Canada and France. They operate three main service routes.

- Charter flights to Sun destinations for Canadian vacationers

- Transatlantic flights from Canada to Europe

- Vacation destination flights in France

They are #2 in market share in the Canadian vacation business (29%) and #2 in the transatlantic business (23%). Their competitors in the Canadian vacation business are Sunwing (#1), Westjet Vacations (#3) and Air Canada Vacations (#4). In the transatlantic business Air Canada is the biggest player, while Air France, British Airways and Lufthansa are all smaller than Transat AT.

What makes Transat a good investment?

There are 3 points to be made here:

- First quarter earnings were hit by the steep fall of the Canadian dollar to which they could not adjust fast enough. I believe this impact is transitory and will be absorbed by price increases over the next 6 months.

- Before the foreign exchange hit, the stock was trading in the low teens and price targets were in the high teens. This is because the company earned $1.60 per share last year and has significant operating leverage to incremental improvements to both the cost side and utilization.

- The historical results suggest that there is room for further improvement in the results.

What happened in Q1?

The Canadian dollar went into a mini-free fall.

Because the drop began in January, which is after the start of the winter season (which begins in December) the company couldn’t adjust prices for the winter season fast enough. Both the first quarter (already reported) and second quarter are going to show the impact of the foreign exchange hit.

Because the drop began in January, which is after the start of the winter season (which begins in December) the company couldn’t adjust prices for the winter season fast enough. Both the first quarter (already reported) and second quarter are going to show the impact of the foreign exchange hit.

The drop in the loonie led to a detrioration in EBITDA when compared to the first quarter of 2013 (when comparing the year over year numbers below note that the first quarter is seasonly the weakest. It has shown negative EBITDA for the past 6 years).

The company quantified the impact of the Canadian dollar drop in this slide deck. The fall contributed negative $14 million to the results.

The second quarter impact is expected to be even worse. In the same presentation the company estimated it would be negative $28 million. Transat has levied a 5% foreign exchange fee in Q1, because the full effect of this is not expected to be felt until the summer season. On the first quarter conference call (in February), management suggested that it would take around 6 months for the currency shift to work their way through the supply chain.

Is the Company Cheap?

I think so.

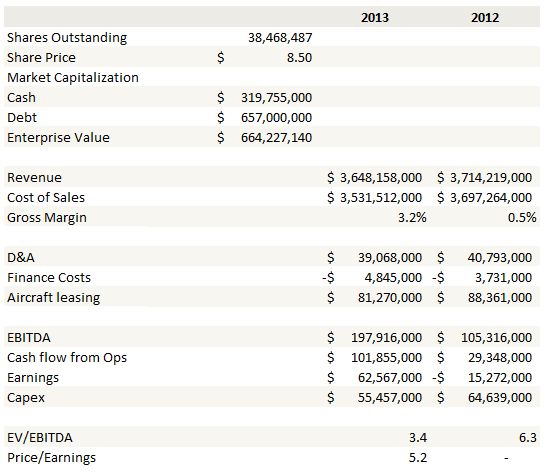

The reason I am willing to take the risk is because the valuation seems very reasonable to me. On the most basic level, the company is trading at a little over 5x last years earnings. Below are the 2013 results and a few metrics to evaluate them by.

I am somewhat optimistic that Transat A.T can still match their earnings from last year. While the first quarter was worse year over year, it was not that much worse; the loss was $1.7 million larger. The second quarter will see a larger currency impact but also the benefit of increased prices year over year and some benefit from the foreign exchange levy. It will also be worse than last year, but again, perhaps not that much worse. Going into the summer we should begin to see the foreign exchange levy work its way through on the revenue side which should mitigate the impact in the second half of the year. Its worth noting that all of Transat A.T’s competitors have levied similar fees.

In the shorter term the stock could go two ways with the release of the second quarter results. It could drop further because the results are going to be poor, or it could rise on the expectation that the worst has passed. It may turn out to be worthwhile to waiting for the earnings release to buy shares, but I didn’t want to be left out so I bought shares and am willing to take the risk.

At the end of this post I have included my enterprise value assumptions. The calculation of enterprise value for Transat A.T is more difficult than most companies because of restricted cash, operating leases and other off-balance sheet liabilities. I thought it best to explain what I am assuming and let readers come to their own conclusions.

Conclusion

If earnings this year can be in the same neighborhood as earnings last year I don’t think Transat AT is going to stay a single digit stock. If you back to before the 2008 financial crisis, when things were “normal” (between 2005-2007) the company averaged a 14x multiple.

But one needs to be wary of a further, quick depreciation of the Canadian dollar. The company can handle a gradual depreciation like we saw through most of 2013, but another spike down and more pain would be felt.

The other metrics to keep an eye on will be load factor and overall revenue. Because of the focus on cost reduction and a return to profitability the company has lost some market share over the last year. Competitors in both the sun destination space (Sunwing) and the transatlantic space (Air Canada) have added capacity. The company has suggested that there is too much capacity right now. It will be important that prices hold. As well, there is an expectation that the foreign exchange levy will have some impact on demand, and I think that when the company suggested 6 months for the ripples to settle, they were speaking about such effects.

As for a positive surprise, there was some talk in January about a potential takeover of Transat A.T. This wasn’t the first time. Being an independent operator of vacation travel, Transat seems to get linked to takeover rumors on a regular basis.

But the main catalyst here is simply delivering on their earnings power. If the currency headwinds abate, I don’t think $2/share in 2015 is out of the question. At a 12x multiple that would be nearly a triple from here.

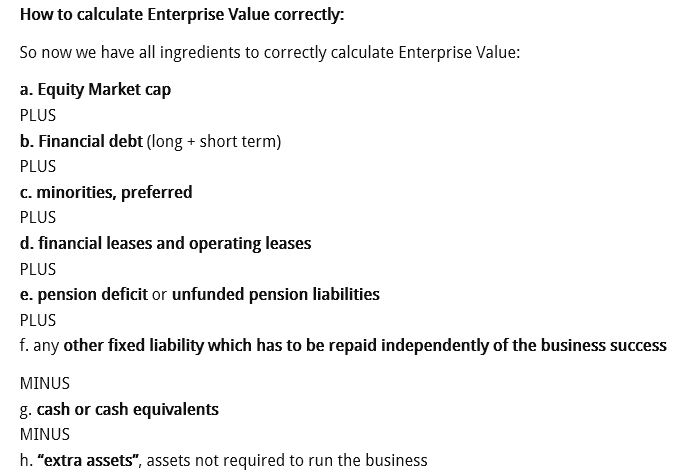

Appendix: How I am calculating Enterprise value

I’ll be perfectly honest. I’m not sure how to come up with the correct estimate of enterprise value for Transat AT, so what I am going to do here is run through what I think it is and then you can agree or disagree.

I’m going to go with a traditional definition of enterprise value as describe from this source. The elements of the calculation are:

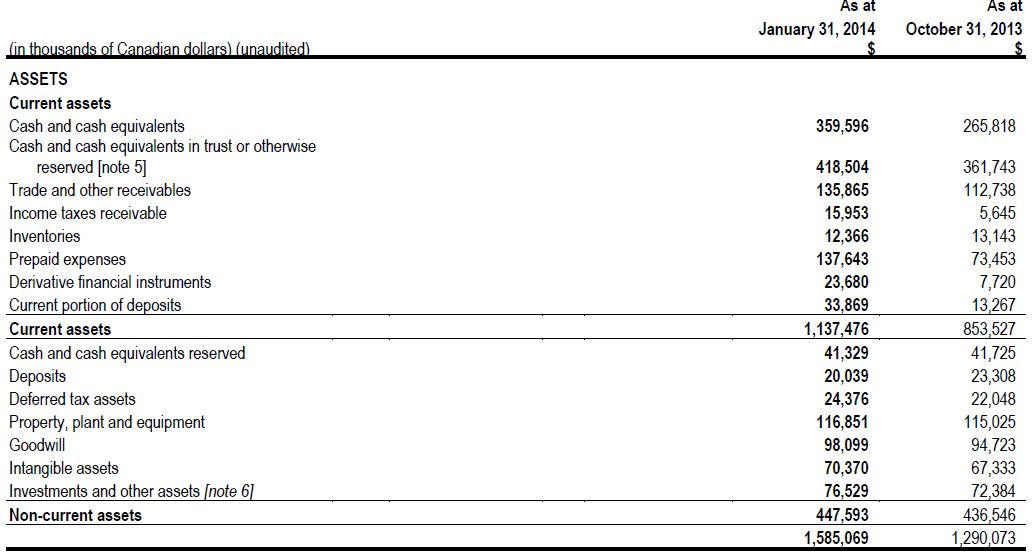

The tricky part of this calculation for Transat is determining what the cash is. And the reason its tricky is because there is a huge amount of cash on the company’s balance sheet. Below is the Asset side of the balance sheet.

Including deposits there is a total of $832 million of cash on the balance sheet. But much of this cash is restricted either in the form of a deposit or as restricted cash. This shouldn’t be included in enterprise value.

That leaves the unrestricted cash, which still is a significant $359 million. Now part of the reason that Transat AT has such a large cash hoard is because collects cash in the form of bookings before it pays the costs when the vacation takes place. But according to the standard definition of enterprise value, as long as this cash isn’t restricted (and the $359 million isn’t) its fair game, and should be subtracted from enterprise value. So that’s what I did.

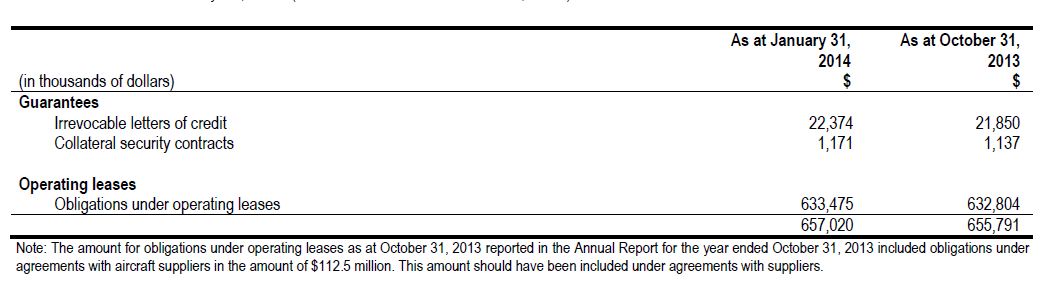

The second tricky part of the enterprise value calculation is the operating leases. The company has an odd way of calculating its operating lease debt (at least I have never heard of it).

I’ve never heard of this before so I am going to ignore it. If you take the simpler approach of looking at the total obligation under operating lease you get something I bit larger.

I am using the $657 million in my calculation.

However I have to say I have some reservations about this. What bothers me is that if this was long-term debt, there would be a principle payment and interest. But with an operating lease, it seems to me that the interest is rolled up into the obligation. So I question whether an enterprise value with significant operating lease obligations overestimates the debt level when compared to if the same assets were owed via long-term debt.

I note that if you look at Canaccord’s research, their debt figure is consistent with the “adjusted operating lease” methodology that the company uses, and so they come up with $400 million of debt.

I have not included any of the company’s agreements with suppliers. As of the end of Q1 there was about $200 million outstanding in this bucket. While the definition of these is not completely clear to me, I believe they constitute agreements to pay for a certain level of hotel, food and beverage, and tour services. I don’t think this kind of obligation should be considered as debt.

At any rate, if you add up all of these assumptions you get the above estimate of enterprise value.

I am curious why you chose to reduce IMOS now. The discount is still pretty fat and they appear to be on track to distribute their cash and become a clean ADR within a few months. Is there a new wrinkle?

No new wrinkle but I added shares a few weeks ago because I thought we’d get an immediate pop from Taiwanese listing and we didn’t get that. So moving my position back to its normal level. Maybe I am too impatient but I only have so much capital and I wanted to have a larger position in TRZ.

Is this post incomplete? It ends with “…you get the following estimate of enterprise value.”

Not incomplete. “following” should be “above”. I am referring to the above estimate of EV in the table in the post.