Week 149: Earnings Update on a few companies

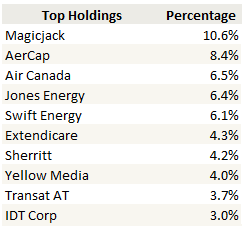

This isn’t a complete portfolio update. I won’t be posting my performance or trades; I will leave that for another week. I just want to give a short update on some of the earnings reports that have come out or are still to come out while the thoughts are still fresh in my mind. Here is a quick snapshot of the top positions in my portfolio as of Friday’s close.

MagicJack

MagicJack earnings come out Monday after the market close. I’m nervous about them, because the stocks action has been poor, it is a large position for me and because I’m not convinced the numbers will be great.

The company lowered advertising spend significantly in the quarter in anticipation of the release of the new version of the device and the app. That will help costs, but it will also probably hurt revenue. On the fourth quarter call the company said that they expected the first half of the year to be “soft”.

I am hoping the market focuses instead on other elements of the business. In particular I am looking for the following:

- When will they release iOS app? The Android app has been out for a month but there is nothing for iPhone yet. I’ve gone through the reviews from GooglePlay and the iStore and the reviews of the Android app are much better. The company originally said they would release both apps in April, so this is a miss.

- What will app user count be? This seems like the most important metric to me. It was 6.9 million at the end of the year. As far as I am aware magicJack is the only company that has free app to landline calling. Viber and Skype allow you to call to another app, but calls to a landline cost money. So there is a significant value proposition here. But the numbers have to continue to bear that out.

- Will the company have other ideas for monetizing app user? magicJack has to keep the basic service of the app free; the value is in offering free calls that no one else does. But they also need to generate revenue. Device users generate an average revenue per user (ARPU) of only about $2.50 per month. This is not a high hurdle to generate relevant rev from app user

- Has the up-sell of international minutes to app users gained any traction? An international device caller generates an ARPU of $9.50 versus the $2.50 average.

- What is impact of the Radioshack troubles? SeekingAlpha had a short piece on Radioshack on Friday. The stores aren’t doing well and magicJack sells in those stores.

- They are supposed to be adding 10,000 locations. Its not clear to me when we should expect a contribution from these locations but some sort of update would be helpful.

- Is this fellow claiming to be Borislow on the message boards right? Borislow is the former CEO of magicJack and he has (surprisingly if it is him) been all over the Yahoo and SeekingAlpha comment boards saying negative things about the company. The quarter results will provide some insight into whether he should be listened to.

Air Canada

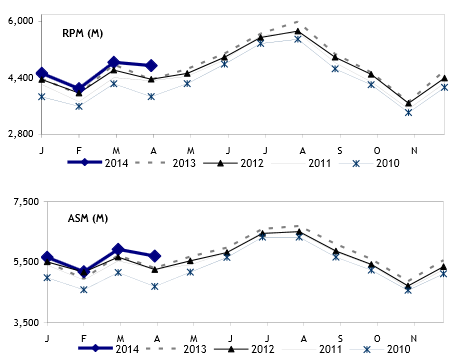

Air Canada reports earnings on Thursday. From what I can tell, things are really going well at the Canadian airlines. April’s traffic numbers were extremely good, well above the estimates of the analysts I have access to. I’m going to steal this chart from one of the research reports that demonstrates the year over year performance. The top graph refers to revenue per mile and the lower to average seat miles flown.

I don’t expect the first quarter results to be blow-out, but I think the forward guidance could be. The first quarter started slow, fare prices were down year over year in January and part of February, and the Canadian dollar was a headwind. But so far in Q2 pricing is up significantly, as is traffic. My biggest worry is simply that the stock has moved quite a bit in not very much time, and so there is always the chance that some bit of negative news will catch the attention of the momentum crowd and lead to a sell-off in the stock. Nevertheless, the immediate trend of the business is clearly positive, so the stock I will hold.

I don’t expect the first quarter results to be blow-out, but I think the forward guidance could be. The first quarter started slow, fare prices were down year over year in January and part of February, and the Canadian dollar was a headwind. But so far in Q2 pricing is up significantly, as is traffic. My biggest worry is simply that the stock has moved quite a bit in not very much time, and so there is always the chance that some bit of negative news will catch the attention of the momentum crowd and lead to a sell-off in the stock. Nevertheless, the immediate trend of the business is clearly positive, so the stock I will hold.

Yellow Media

I went into Yellow Media’s earnings Friday with nearly a 10% position in the stock. I came out yesterday with that position down to 4%. As is too often the case with my winners I have been slow to react; I should have been reducing my position over the last few months. But I didn’t.

I have a tendency to look at stocks that have gone up significantly with rose colored glasses. I find that I don’t think hard enough about valuation and the business until the stock starts to decline. In some cases this thinking hardens my resolve (ie. magicJack) but in most cases it makes me realize that the thesis that led to my original purchase has played out.

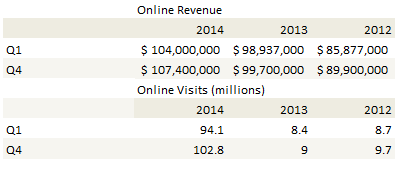

There was nothing fundamentally wrong with Yellow Media’s quarter. I went back through past first quarter reports and confirmed that the sequential weakness is consistent with other years, and the year over year strength of both Digital and Print (Print was actually a 2% improvement over 2013) was steady.

(note that Yellow Media changed the metric for online visits from unique user views to total digital views in the first quarter this year).

(note that Yellow Media changed the metric for online visits from unique user views to total digital views in the first quarter this year).

I believe the market got spooked by comments on the conference call that it would be 2018 before revenue stability. I think that is wrong thinking; its just the math. If you stretch out 20% print declines and 8% digital growth I calculate that it isn’t until 2019 that revenue starts to trend up. So the company is actually factoring in something a bit better than that.

But it is what it is. The stock is still cheap. Just not ridiculously cheap. I believe the story from here is less about a ridiculous valuation and more about execution. That will take time to play out and I don’t have a great analogy to form my mental map of how it plays out so really, its a whole new ballgame. When I have something without a lot of evidence I don’t like to have a lot of my portfolio tied up in it. So I reduced my position to a reasonable amount and will watch it play out from here.

Extendicare

It feels like I have been waiting forever for something to happen with Extendicare. And that in fact is, at least in investing time, close to the truth; its been a year since I bought the stock and we are going on five months past the deadline when the review was supposed to be complete. But with the first quarter results and the ensuing conference call, we got some clarity on the status of the process that gives me optimism. The relevant excerpt (via SeekingAlpha) is below:

As we announced last quarter, we are working with the prospective buyer and have had negotiations relating to a transaction involving the sale of the U.S. business in a tax efficient matter. However, these negotiations are dependent in part on the satisfactory resolution of the previously announced Department of Justice and Office of Inspector General Investigations.

If the investigations can be resolved in an acceptable manner to us and the perspective buyer, we expect that the separation of the businesses will be affected by way of a sale of the U.S. business. If not, we will nevertheless proceed to separate the Canadian and U.S. businesses, utilizing one of several alternative techniques that are being considered and analyzed by the strategic committee. The status quo is not an option.

A lot of my Yellow Media money was piled into Extendicare. Here’s an event driven situation where management has spelled out that something is going to happen, where there is good evidence that what will happen will be accretive to the stock price (see my original post on this for some detail on that), and that what is going to happen is going to happen shortly (they said they will get the indication they need from the OIG by the end of June). This might not be the multi-bagger I thought it might be when I bought it, but I bet we see $9 before this is all said and done.

Jones and Swift

I put these two stocks together because they are both large bets on energy and natural gas. But they are quite dissimilar in most other respects.

Jones had a great quarter. Great quarter. The production numbers beat guidance handily. They have lots of cash to grow in the coming quarters – they raised significant high yield debt at 6.5% (high yield?), and lots of land to grow by.

They are getting ready to drill a Tonkawa well, a formation for which they gave more color during the conference call. The Tonkawa is oilier than the Cleveland, which is good, and they think they can drill the wells for a little over $3 million, which, if they can produce results like they have shown in their presentations (400-500 bopd IP30 with a little less than an MMscf of gas) it would be quite prospective.

The update on the new frac design was also positive. When Jones said on their year end call that they would wait until summer to make a decision on the frac design I think the market took that as “oh that means the frac designs a dud”. It appears that what that actually meant was that they were going to wait until the summer to make a decision on the frac design.

I appreciate that. Look, they had a new design and a theory of what it would do and some analogies and a few calculations to justify giving it a whirl. But as with most things with oil drilling, its really just an educated guess. So they wanted a full suite of results before drawing a conclusion. This is exactly the approach you take when you are doing solid engineering work. You don’t jump in until the data is conclusive.

Here we are a few months on and the company is seeing what they expected. Overall volumes are at or above the type curve and, more importantly, the volumes are oilier. It makes sense; you frac more area at a higher density, you free up more oil and increase the permeability to make it easier for the oil to flow. That was the theory and the hopeful reality that is looking more to be the case.

Swift, on the other hand, can’t seem to get traction. They did a joint venture on the Fasken for $175 million. The joint venture is for 36% of the Fasken property, which is about 8,300 acres. I’m not sure which way to value this but one technique would be to look at the number of proved undeveloped locations Swift has on the property (58 at year-end 2013) and calculate the value per location. That works out to $9 million per location, which is a lot. On a pure acreage basis it works out to over $50,000 per acre, which is also a lot.

Of course the market thought less of it, at least since the initial pop in the share price. The problem is that A. Swift is over-levered with too much debt and B. a Fasken JV was always a plan B type of transaction, with the real positive catalyst being the sale of its non-core Louisiana properties. When you JV one of your top producing core area, there is a negative spin that can be made. It also doesn’t help that they egged the analysts by announcing the joint venture a few days after a conference call where they were sufficiently vague about its probability to engender downgrades from around table. The analysts I read hedged their comments on the sale, in my opinion mostly because they would look extremely foolish to give a rah-rah review after downgrading the stock only 1-2 days before.

I’m holding this stock because the results in the Eagleford (Fasken and McMullen counties) have been very good and I am still hopeful that they will sell Louisiana and de-leverage themselves to some degree. What they need, aside from the Louisiana asset sale, is a really solid quarter where they beat estimates handily, thus proving that their Eagleford acreage is not fully priced in. I think that could happen in the second quarter. Many of their first quarter wells came on in March and they are timing their second quarter wells such that they will be on-stream by mid-May. So the second quarter could see a strong result of a lot of flush first 90 day production.

Sherritt

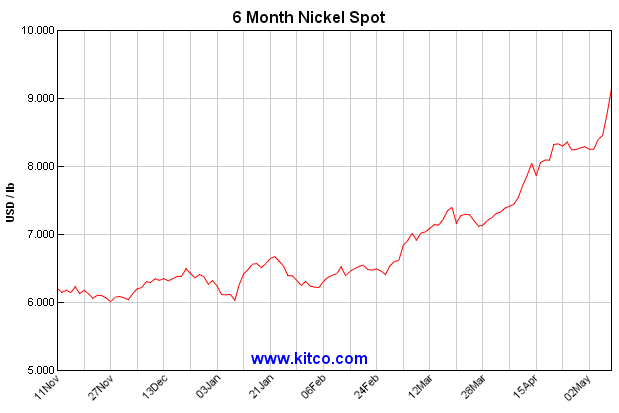

Sherritt has been consolidating for the last few weeks. Since Armoyan was defeated in the proxy vote (I voted for him) the stock has sold off, which could be nothing or maybe he’s getting out himself. All I know is that nickel keeps going up and the Indonesian government has yet to cave.

When nickel is over $8 Sherritt begins to make a lot of money from its nickel mines. In 2012, when nickel averaged $7.80, Sherritt had EBITDA from its Moa mine of about $125 million. In 2011, when nickel was $10, EBITDA was over $200 million at Moa. Today Sherritt is producing at about the same level at Moa, and once fully ramped up they will have a similar level of production at Ambatovy. The longer nickel is able to stay at or above these levels (which is wholly dependent on the ability of the Indonesian government to hold its ground on exports), the less likely it is that Sherritt will stay at these levels.

When nickel is over $8 Sherritt begins to make a lot of money from its nickel mines. In 2012, when nickel averaged $7.80, Sherritt had EBITDA from its Moa mine of about $125 million. In 2011, when nickel was $10, EBITDA was over $200 million at Moa. Today Sherritt is producing at about the same level at Moa, and once fully ramped up they will have a similar level of production at Ambatovy. The longer nickel is able to stay at or above these levels (which is wholly dependent on the ability of the Indonesian government to hold its ground on exports), the less likely it is that Sherritt will stay at these levels.

Just curious, is there any proof that the poster calling themselves Borislow is actually Borislow? Seems like it would be an effective tactic for someone to take if shorting the stock.

Thats a really good point. I don’t have any information that could confirm with certainty that its him. Its just another moniker on SA and Yahoo.

Go call on CALL? Traded off on the quarterly earnings announcement. Time to buy?

I didn’t think the report was that bad. Everyone seems to be focusing on lower revs, lower eps, lower subs. but I didnt think that was a surprise. They are just a month away from a new product launch, they reduced add spend quarter over quarter, they havent seen the impact of the 10,000 new doors; I’m not sure what the shock is.

The one negative that I saw is that while app installs was up big (21% qoq) but their actual active users only increased 200,000. They aren’t actually gaining users yet at a very fast rate. I hope that changes with the new updates to the apps for iPhone and android.