Week 153 Update: Investing by a Thread

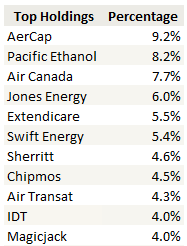

This is not a full update of my portfolio so I will not be providing all the details of my current positions and trades over the last few weeks. I’ll do that again in the next week or two. Below are my current top 10 holdings and their percentage weighting in the portfolio.

In this post I want to write about the tenuous nature of most of the stocks I hold. While I make many purchases based in part on the judgment that an undervaluation exists, I’m not really a value investor in any strict sense of the definition. I don’t really look for stocks that are simply cheap to their intrinsic/discounted/net asset value and then wait for something to happen to change that.

In addition to cheap I’m always looking for a catalyst. Something that will change perception of the stock and where the stock has enough leverage to the change to make for meaningful upside.

Because of these two criteria I find that I am drawn into an inordinate number of cyclical, indebted, tenuous or heavily capital dependent businesses. They are not great businesses over the long-run. Their true value is usually wildly erratic depending on the assumptions used. While this characteristic represents the opportunity it also means I have to continually re-evaluate the thesis and sometimes admit that I am wrong and give up.

I did that with magicJack recently. I am considering that with Swift Energy, as I will explain below. With the other stock I will walk through in this post, Pacific Ethanol, I am aware of its shortcomings and will not hesitate to reduce my position on the slightest indication that my thesis is not holding up.

Pacific Ethanol

I rebuilt my position in Pacific Ethanol a couple of weeks ago. I started buying at $12 and added up to $13. Its currently one of my larger positions.

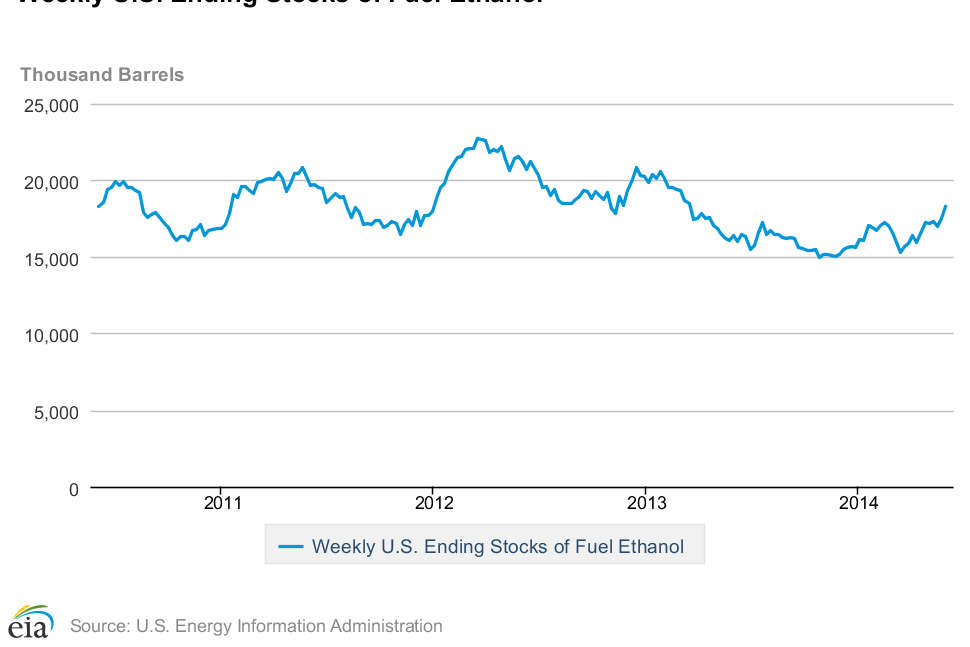

Admittedly, it may be too large. Why? Ethanol inventories have been rising the last couple of weeks. In the spring inventories should be declining. I’m not sure if this is being caused by ethanol that had previously been stranded due to rail car issues finally making it to market or something else, but it is a bit concerning.

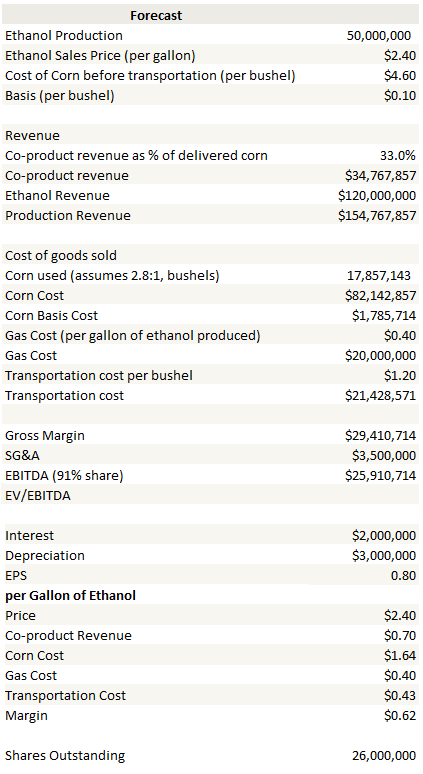

I renewed my bullish stance on Pacific Ethanol because corn prices have fallen back from their five dollar plus peak. Right now corn is below $4.60/bushel. CME ethanol prices have held up in the range of $2.10-$2.30 per gallon, and NorCal hub ethanol, where Pacific Ethanol sells much of its product, has been even stronger, getting into the $2.80’s earlier this week.

I’ve updated my earnings model on Pacific Ethanol. The company can achieve somewhere between $3-$3.50 earnings per share if ethanol and corn prices stay in their current range.

So the upside story is simply a strong Q2 report and some positive expectations for Q3 and the stock could easily break $20. Nevertheless the stock and industry remain volatile and I won’t be buying more unless I start to see a down tick in the weekly inventories again. But clearly if we can see stability in ethanol margins at these levels (or higher), the stock will likely move up.

Swift Energy

As a way of introducing the issue with Swift Energy, let me first talk about Jones Energy. Jones Energy, like Swift, is an E&P. The company takes a beating on twitter, in my comment section and in emails I receive because, like most-every oil and gas company it doesn’t show particularly strong free cash flow or earnings.

My response to these comments is not so much that I disagree, but that I don’t think those metrics are particularly relevant. From my experience as long as an oil company is growing production, its free cash flow and earnings growth are not at all correlated to the share price. In fact, it seems that by the time an E&P achieves decent earnings and is spending within its means, most of the share price growth has finished.

Far more important seems to be well performance, acreage and the availability of funds. As an example, take a look at Clayton Williams (which I have been watching closely and am terribly amiss that I did not pull the trigger) and their share price over the last 4 months. The company certainly fails in terms of free cash flow and earnings, but possesses excellent well results, acreage and the funds to develop it.

Now back to Swift Energy. The problem with Swift is that the growth stalled out along with the funds. Just as there is a virtuous cycle on the way up, there can be a vicious one on the way down.

I have been hoping (and I believe hope is the unfortunately operative term here) that Swift could (can?) pull off a divestiture of its Louisiana assets that would change that equation. But that has not happened. At the RBC Capital Markets Global Energy and Materials conference the company said that they would have an update by mid-year, but not an agreement. So on it drags.

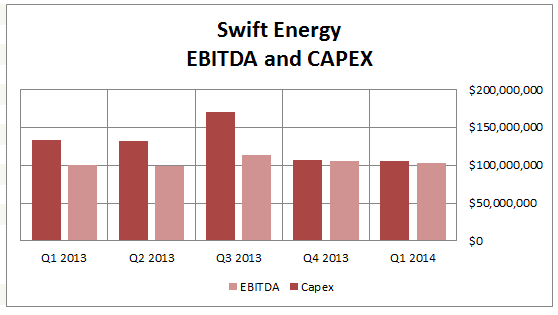

On an EV/EBITDA metric Swift Energy remains at a discount to its peers, trading at almost exactly 4x EV/EBITDA based on its first quarter results. So its comparatively cheap, but as I continually have to relearn with E&Ps, just as with free cash and earnings, cheap is not really an indication of future performance.

At this stage the company needs to show it can grow without taking on new debt. To that end, they have tried to rein in spending. Over the last year Swift has gone from far outspending its operating cash to spending within its EBITDA.

The problem is that with the accumulated debt they are still not generating enough cash to cover their interest charges. The result is that debt, while having slowed, is still increasing.

The problem is that with the accumulated debt they are still not generating enough cash to cover their interest charges. The result is that debt, while having slowed, is still increasing.

I remain long the stock, but am coming around to the idea that this will maybe languish at these levels indefinitely. If the asset sale of Louisiana is not going to occur in the short-term, the immediate catalyst (either up or down) will be the second quarter results. This is the other leg of the thesis: the Eagleford results, especially at Fasken, have been very good. The second quarter could show quite decent growth and that alone could propel the stock. Could.

I need to decide what sized position I am willing to risk heading into the report, because Swift has been known for its surprises and they are not always positive one’s. The opportunity cost of holding Swift since December has been significant. I’m essentially flat on my position, but only because I added to it in the $9’s after originally buying in the $13’s. When I look at some of the other places that money could have gone (Clayton Williams being one place, virtually any mid-cap Canadian E&P being another) it makes my stomach churn a little. Again, I lack the patience of a true value investor.

magicJack

As I tweeted a few weeks back, I reduced my position in magicJack substantially. Two reasons behind this reduction.

A. Its not working. The stock can’t rally to save its life. It could be just the impact of short-sellers creating exactly the environment that will cause (weak?) hands like me to cave, but I’m not omniscient enough to know what the future holds and have been burnt enough times to know that it is better to do less of what does not work.

B. The reviews I on the new magicApp are mixed. Last year, when I bought magicJack at $12, it was under the thesis that the stock could go to $18 on some positive news. The stock went to $18 (and well past that), but I became convinced that the magicApp, which allows you to connect your home phone and smart phone to the same number and call for free within North America (including to other landlines) could deliver growth for the company and send the stock even higher.

I still think that idea has merit, but the truth is that the app they have released for Android and iOS is getting only mediocre reviews (read here). You saw the impact of that in the first quarter, where the app installs grew from 6.9 million to 8.4 million, but the active users only grew by 200,000.

Now it does appear that magicJack is actively improving the app; they put out a new release on iOS in mid-May and just released one on Android a couple of days ago. So maybe it will turn the corner. But I need to see an up-tick in sentiment before I make a bet in that direction. Without the app changing the business model, the device business and cash on hand is probably worth about what I thought it was last year when I first bought the stock.

Illuminating as always. You understand how you think, which gives you a big advantage as an investor and blogger.

Hey LSigurd,

Always appreciate your work. For CALL have you looked at their pending lawsuit?

http://www.bloomberg.com/article/2014-05-21/akh7wqGunf4s.html

Not an expert in patent law by any means but

http://www.google.com/patents/US8243722

seems to cover the magicjack plus. Specifically the ability to connect the device directly to the modem, then to the internet…

I really liked this company back when it was trading at 12 and showed up on my FCF screen. Watched it go to 24 and kicked myself for doubting my analysis but when I saw that lawsuit I didn’t have the stomach for the binomial outcome of either status quo or a real dropoff… Even at its amazingly low ev/fcf and simple business model… Just thought I could hopefully give back to you after you’ve given so much to me.

I read through the lawsuit on scribd a while back and I didnt get a strong sense one way or the other of how likely it is to be a problem. The patent details are helpful thanks. Doesnt patent refer to a wireless connection device? I dont think MJ has that. Maybe I’m reading it wrong.

More generally, I dont know whether I should be putting more emphasis on this but my first thought is realistically, is it going to impact how CALL performs in next 3-6 months? Do you think lawsuit will resolve in that timeframe? If not will the share price be negatively impacted by the lawsuit in that timeframe. I have found in the past these lawsuits take much longer to play out. So that makes me wonder if I should be making an investment decision based on something that is likely to occur in a timeframe outside of the time horizon of my investment. Would appreciate thoughts on what may happen in next 3-6 months that would cause patent litigation to impact CALL share price?

I wish I could offer an educated response to that but I can’t. I know what you mean about the shorter term time period though… But it goes against all my nature as an investor!

You’re getting a nice little bit of a pop here so that’s good.

noticed yellow media has dropped off the list. Have you bailed/further reduced or is it simply lagging progress relative to other holdings that have grown?

I did sell a little more when it got up near $21. Its about 2.5% position now versus a little over 3% at the end of May