Taking advantage of the disappointment with Bellatrix

This is a company I should have owned 12 months ago when I was looking around the Canadian oil and gas universe but instead pissed around trying to buy the cheapest thing. When investing in an oil and gas company buying the cheapest thing is simply not the way to make money. I’ve been investing in the sector for 10 years now; every time I walk away and return I have to learn that lesson again. Hopefully that will end now.

Bellatrix Exploration (BXE) is simply a company with lots of land in very prospective areas and a history of being able to grow production on a consistent basis. The stock is on sale because of a bungled private placement and I think that presents an opportunity.

Background about the company

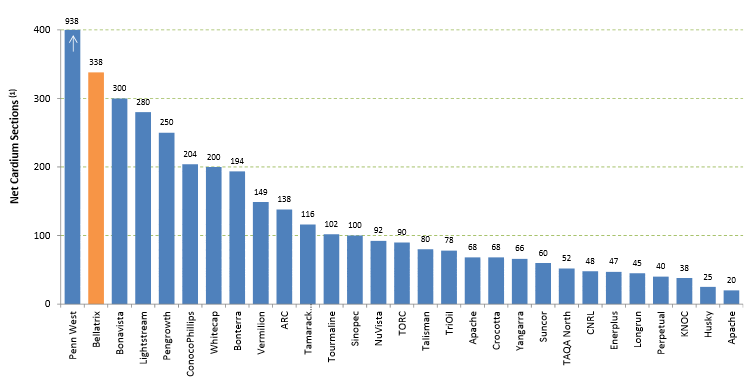

Bellatrix owns one of the largest positions in the Cardium (in Alberta) in the industry.

They’ve proven they can develop that land in an efficient manner. The company has grown its production the last 4 years and expects another strong year of growth in 2014 (note though that the 2014 production number is being buoyed by the acquisition of Angle Energy, which closed late last year).

The opportunity to buy the stock at 20% off the recent highs has come because they bungled a bought deal. On May 27th Bellatrix announced a $250 million bought deal and on the 28th they announced that they had reduced the size of the share offering by over 30% and the pricing from $9.75 to $9.50. This turned off a lot of their investors and led one BNN analyst to call the stock “uninvestable”.

With its shares in free fall the company jumped into damage control and scheduled a conference call shortly after the deal was repriced. The call clarified a few important points:

- There is no problem with production. April production was in-line with expectations, May production was above expectations and June was slightly below expectations.

- Concerns about changes to type well curve at Ferrier (the EUR changed from 660mboe to 510mboe in the recent presentation) was put in perspective. The changes refer only to the rich gas wells of which Bellatrix has drilled less than 5, the remaining inventory is small and those wells are not the focus of current development. Reviewing some of the reports on Bellatrix, I note that Ferrier as a whole, which includes both rich gas and high GOR wells, accounts for around 7-8% of NAV

- The bought deal was initiated to help pay for an expanded gas processing facility and for accretive acquisitions that they have in their sights.

So they basically came out and said there is nothing terribly wrong. Meanwhile the stock is down some 20% off its highs at a time when other Canadian producers have been moving to progressively higher valuations.

Not Expensive

Bellatrix is cheap for what you get. I don’t believe the current valuation reflects the company’s true potential. Based on the first quarter numbers Bellatrix trades at 6x EV/EBITDA and about $55,000 per flowing boe. A comparison that I first heard on BNN was with Paramount Resources. Paramount produced 21,000boe/d in the first quarter (Bellatrix produced 35,000 boe/d). Paramount has a higher exit rate forecasts (expects to exit at 50,000 boe/d while Bellatrix expects to exit at 48,000). Bellatrix has about double the oil and NGL weighting that Paramount has (33% versus 17% based on first quarter production. Yet Bellatrix trades at an enterprise value of less than $2 billion and Paramount trades at $6 billion.

Looking out at the universe as a whole, Bellatrix trades cheaply. The following is a peer comparison (which is hopefully ok to reproduce) that illustrates the disconnect so well:

Conclusion

Of course it could be asked what the heck management was doing issuing paper if their stock is really so undervalued. But as a new investor to the company I look at this as water under the bridge. They raised $172 million at a price 5% above where I have been buying the stock. They will be increasing capital expenditures by $60 million with the proceeds, which will allow them to grow production faster. They will hopefully announce one or more accretive acquisitions. It will take some time for the market to move past the botched offering but I think it will happen. When it does I expect at least $12 per share on the stock.

Even more so than “what the heck management was doing issuing paper if their stock is really so undervalued,” what I want to know is why wasn’t there much demand for their paper if it really was undervalued ? Kinda questions the entire thesis doesn’t it?