Week 159: Blog Days of Summer

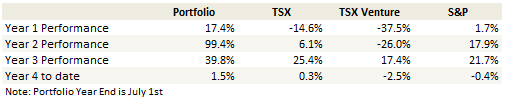

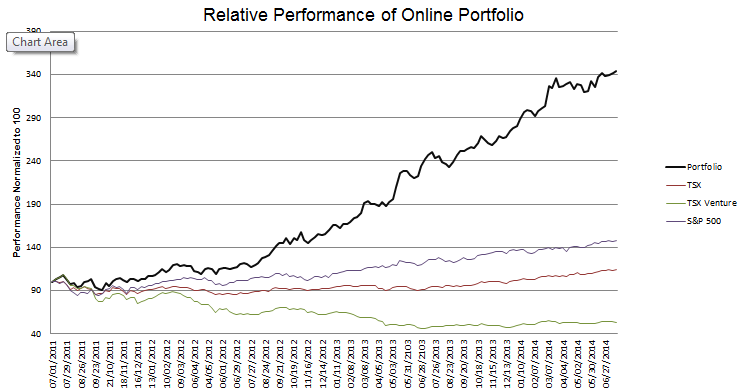

Portfolio Performance

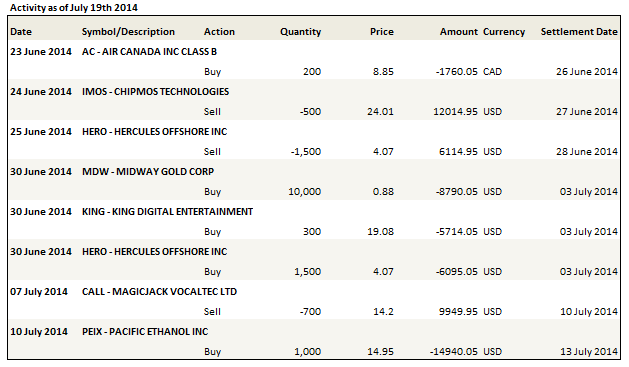

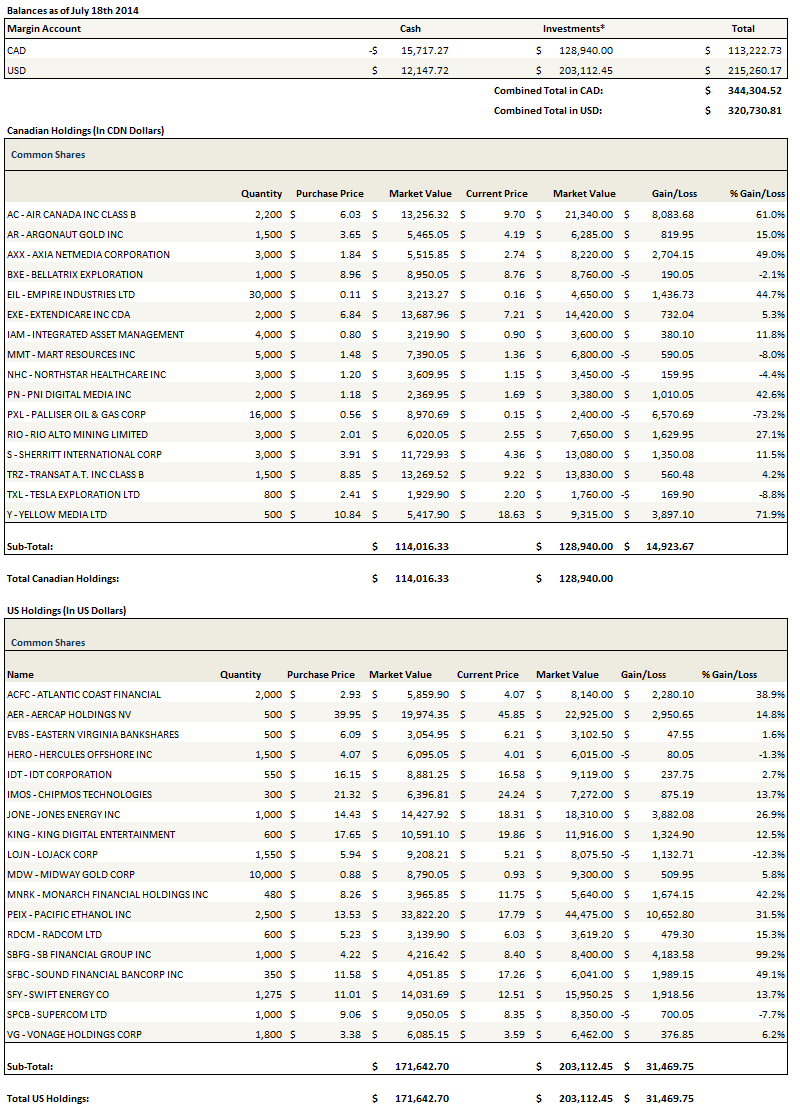

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I haven’t done a lot of writing since my last portfolio update four weeks ago. I have made only a couple changes to my portfolio, and added only one new position, Midway Gold, which I wrote about last week.

I remain reluctant to add positions. As I stated previously (here and here) I remain wary of the market reaction to the post-QE era. So far nobody seems to care, tapering has had no negative impact on stock prices, and we continue to march to higher highs. Nevertheless I’m not convinced. I don’t have a lot of insights into the specific mechanism by which quantitative easing leads to higher stock prices or how the end of it will cause them to go lower but I know from experience that you can’t overstate the importance of liquidity, particularly where small and micro caps are concerned. Now we’re in the process of draining a bunch of it and I just don’t think that is a great time to be too far out on the ledge. Why take the chance when you don’t have to?

I’m also not having an easy time finding stocks that I want to buy. I’ve spent the last four weeks rather diligently investigating new ideas. I’ve probably gone through 100 names. Nothing I have looked at has stood out as something I have to own.

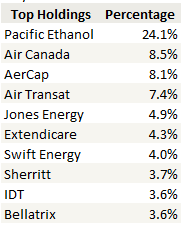

In fact, I’ve come back to old names. In particular, I’m currently betting the farm on Pacific Ethanol. Below is a list of my top ten positions. Pacific Ethanol was a 20% position that has grown to 24% because of price appreciation.

Pacific Ethanol

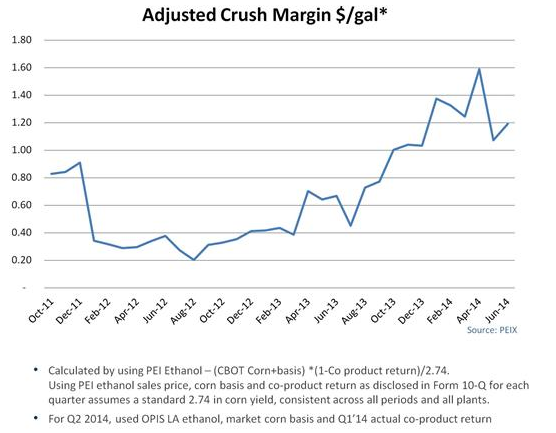

Why am I taking such a large position in an admittedly easily distressed and exceedingly volatile industry whose economic justification still rests on a government mandate? Its that they are quite simply making money hand over fist. In particular, what seemed to slip past many investors (or maybe its just that nobody cares about an ethanol company) is that Pacific Ethanol basically telegraphed their earnings in a recent presentation at the Global Hunter Energy Conference via this slide:

I don’t think the above margins include gas costs, which usually are around $0.40 per gallon. Assuming they don’t, that would mean all-in margins are around 90c. That should guarantee even fully diluted earnings (roughly 26 million shares fully diluted) of $1 per share.

I know the ethanol industry is full of questions but I also have found from experience that in the short run, as profits are piling up, that doesn’t matter much. Some simple extrapolation of $4+ annual earnings might be a better reflection of what to expect from the share price in the next couple of months than a long-winded analysis of the margin of safety (or lack there-of) presented by the ethanol industry.

Gold Stocks

As I remarked in my last update, the positions that I have been taking of late have been gold stocks. This turned out to be well timed, though I every day I question whether I have overstayed my welcome. My three original positions, Argonaut Gold, Endeavour Mining and Rio Alto Mining, were all up 30%+, but Argonaut released some crummy second quarter results and the stock has fallen since. I was so close to selling Argonaut when it was hovering around $5; I know it has mostly mediocre deposits and yet trades at a premium to its peers. I also know that it can have a very strong move up when the price of gold goes up, which is why I bought it. But I should have remembered it was a trade and not gotten greedy trying to wring a few more cents out of it. Its one of those lessons you have to learn on a recurring basis. I sold it today at $4.10, for a 12% gain, instead of the 30% I could have had a couple weeks ago.

Back into Supercom

I wrote in my last update how I exited my position in Supercom with some trepidation and how I hoped to enter back into it lower. I did that, I got back in at $9, and then I promptly watched the stock fall another dollar over the rest of the week, which, ironically, is the price I said I would wait for in my previous comment.

I am hopeful that Supercom will have good earnings through the rest of 2014. The company has booked $29 million in business over the last number of months, they expect much of that revenue to be realized in the following three quarters and my annual revenue estimate before these new contracts was only about $25 million. The caveat is that I am a little unsure of whether there is overlap between the new contracts and the existing book of business so the revenue figure might be somewhat less robust than first glance. Still, I think it could be quite a good number, and there is potential for more contracts to be announced.

So I bought back into the stock too early, not wanting to miss out on the upside. I was able to add a little more at $8.

Shorts

I’ve been looking for shorts. There are plenty of stocks out there that appear stretched to a valuation that even robust forecasts would have trouble growing into. Taking the opposite side of a few of these positions seems like a good way to hedge myself through the summer and fall. One article that was forwarded to me and that I found particularly interesting was this Bloomberg piece titled Whitebox Shorting Never-never stocks in Graham Reversal. I’ve looked at a few of the ideas from the article, and in particular Shutterfly and Advisory Board look somewhat interesting. I already have a short position on Yelp, which, while not mentioned in the article, I would argue would fit the criteria expressed. While I understand they’ve gotten an early lead on a neat idea that drives a lot of traffic, I don’t really get how Yelp is going to generate enough earnings from the model to justify their valuation.

But I have to admit, I’m not sure if chasing pricey stories is the right approach. Never short on valuation I am told. And indeed, these companies are all growing revenues. They just have no or little earnings. That alone probably isn’t enough to send the stocks down until the market itself takes a tumble. Given that I am wary this may be on the horizon, perhaps that is not a bad thesis. But its probably important to realize what the bet is; that these valuations are sustainable and even expandable as long as the market continues to go up.

I would be more content to wait on their eventual slippage if it weren’t for the possibility of a takeover. Some sort of heavy premium keeps me from taking anything other than micro-positions in these names. That is the thing that really scares me here, and keeps my positions small.

Portfolio Composition

Click here for the last five weeks of trades.

Agreed, never short on valuation as someone could come along and buy out at a ridiculous premium either using as a loss leader or to help protect their business (something that GOOG has done). In the article as a short, OPEN was bought out by PCLN a few days later. While OPEN is profitable, OPEN was purchased with a 50x PE and annual revenue growth of 15-20%. PLCN trades at less than half the multiple while also forecasting higher annual revenue growth of 20-25%.

Thanks for the writeups, I really enjoy and appreciate your work. I have one question about PEIX. What are your thoughts, if any, on the high short interest?