Week 161: Earnings so far – Pacific Ethanol and my other ethanol plays

I agreed to this deal with Seeking Alpha where they post my articles from the blog and I don’t have to do anything. Its a pretty fair deal; the reason I never published them before had more to do with me being lazy then anything else. The only downside is that everything I write will get posted and I don’t want everything I write to get posted because much of what I write is blog-worthy but not publishing-worthy. Sometimes I just want to post my thoughts here, and not have to reference and review every data point to make sure I have all my t’s crossed. Therefore I created a simple rule whereby if I put the words Week XX in the title of my post they do not get published on Seeking Alpha. And that is the long winded, paragraphical description of why I continually make the rather banal observation of how many weeks I have been writing this blog in the title of so many posts.

With that out of the way, lots of earnings reports for companies I own came out this week and I am going to give my thoughts on a few of them. We will start with the biggest of the bunch, at least in terms of my own P&L: Pacific Ethanol and my other ethanol plays.

Pacific Ethanol

This is a very large position for me and so obviously I was paying close attention to their report on Thursday. I was a little surprised that the earnings per share number was below a buck. It turns out that I had missed a couple things.

First, I didn’t realize that the company wasn’t able to utilize their net operating losses (NOLs) in the second quarter and would therefore have to pay tax. This was mentioned in the Q1 10-Q but I didn’t read through the details carefully enough. So the company was taxed at 30% and that was a big reason the earnings per share number did not hit the magic $1 mark that I had expected.

Second, gross margins came in lower. I thought at first that this was because of one time costs due to the Madera start-up. The company had said in a previous call that they had expected $7 million start-up costs for Madera, and that was pretty much the amount I was off by (my model was off on gross margins by about $6 million). As it turns out, while Madera’s start-up appears to be the cause of some of the discrepancy, according to another investor and message board poster who I have followed for a long time and who called the company, a bigger impact was caused by the marketing division. Pacific Ethanol markets ethanol for third-parties and receives a small stipend for their troubles. I had mostly ignored this segment in my model because my numbers for Q4 and Q1 were pretty close to the actuals without it. Turns out that this segment can at least lose a material amount of money if ethanol prices drop precipitously in a quarter, as they did in the second quarter. If I assume that the Madera start-up contributed about a million to the cost of goods sold, I am left to conclude that the marketing segment lost around $5 million.

Apart from that the quarter was about what I had expected. It was still very good. The stock did pretty much what I expected as well, selling off on the opaque miss and then recovering once everyone had a chance to digest what had actually happened and realize that plant profitability was extremely good. The conference call was fairly boring, no one even bothered to ask about gross margins, which leads me to believe that either the professional investment community understands the company’s P&L much better than I do or no one cares about Pacific Ethanol. I lean to the latter.

One interesting question that was asked on the call was what the impact would be of the changes to rail car requirements for ethanol. Ethanol is getting lumped in with light oil as a flammable liquid and will soon require stricter standards for the rail cars used for its transportation. Pacific Ethanol is one of if not the only significant ethanol player that does not rely on rail cars to ship its product. Because of the plant locations, corn is shipped via rail to the plants, but ethanol is trucked to the customers. We should expect higher differentials in ethanol prices between regions if the changes pass into law and the differentials should be favorable to Pacific Ethanol. Corn, at least so far, has escaped the scrutiny of regulators, though I can attest that corn left on the BBQ too long will indeed burn, so maybe we aren’t out of the woods yet.

Ethanol Exports

In my opinion the best news for Pacific Ethanol and the other ethanol producers came from the Green Plain Renewable Resources conference call. The company presented a very bullish picture of ethanol supply and demand going into 2015. In particular, the export picture looks very strong. Green Plains said that they have already sold 16% of their Q4 2014 and 14% of their Q1 2015 production for export and are seeing export demand from both new and traditional market. They also pointed out that if Brazil continues to experience drought, things could get even more interesting.

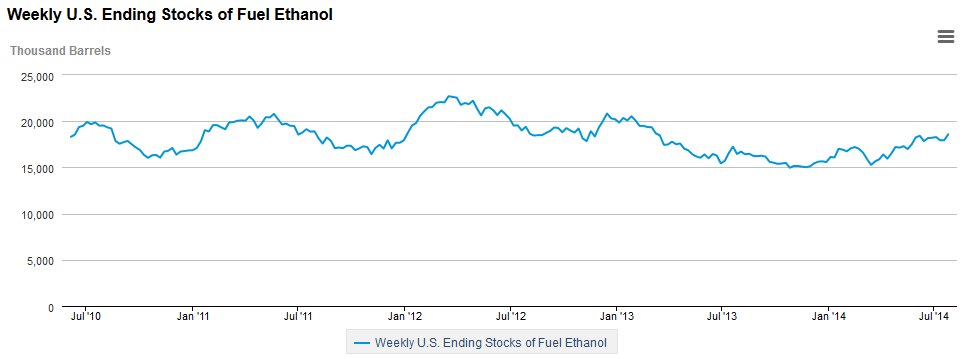

This is good news because the one thing that has me worried about my ethanol plays (while I don’t own Green Plains I have, in addition to my position in Pacific Ethanol I have taken a reasonably large position in REX American Resources Corp (REX) and in MGP Ingredients (MGPI), which I will discuss briefly below) is that the inventory is yet to fall along with the summer driving season. Here is a snapshot of the recent 5 year chart. Note that there was yet another up-tick with a build this last week after a few weeks where it appeared that ethanol stocks would begin their annual draw down.

I’m still looking optimistically at the inventory changes. The winter season saw almost no up-tick compared to prior years and I attribute that partially to the reduced rail availability. It could be that the inventory changes we are seeing now are from the stranded winter production trickling in.

My Other Ethanol Plays

As I mentioned above I have added another pure ethanol play in REX American and another more corn oriented play in MGP Ingredients. MGP Ingredients (hat tip to @17thStrCap for pointing this one out to me) is pretty interesting and worth a look in my opinion. The company has a stake in an ethanol plant in Illinois that boosted earnings in the first quarter, but I don’t think we’ve seen the full impact of what earnings can be yet. This is because the company owns another plant that produces distillery alcohols from corn and other grains. The first quarter was a good quarter for the ethanol producers because the price of ethanol was through the roof. To some extent the second quarter and to a large extent the third quarter are good quarters for ethanol producers because corn prices have collapsed. The food alcohol business for MGP Ingredients stands to benefit from the latter, not the former, so I am hopeful of some good earnings going forward.

I’m still working through the details on this one, in particular I’m still having trouble nailing down the pricing power of the food alcohol business and whether they can capture the full extent of the margin expansion implied by falling grain prices. In the mean time though, I’ve learned enough to take a position in the play.