Week 181 Doing ok but not loving this market

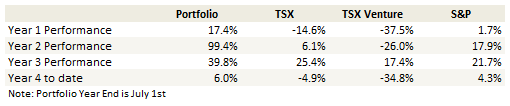

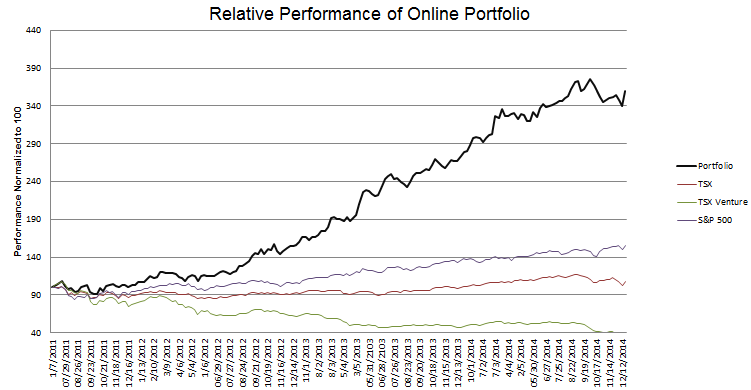

Portfolio Performance

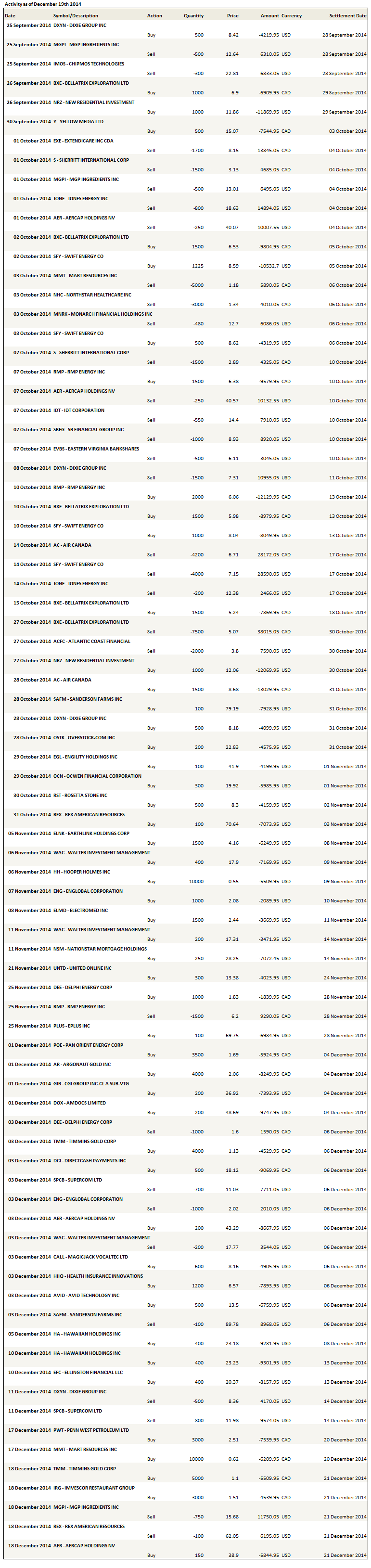

See the end of the post for the current make up of my portfolio and the last twelve weeks of trades (its been a while since I did a full update).

The last few weeks have been a rollercoaster. It was less than a week ago, on Tuesday night, that I was deliberating whether I should be making dramatic cuts to my exposure the next morning. By the market close Friday my portfolio was back to the post October peak.

The gyrations have not been due to particular volatility in the stocks I own. Over the last month I have basically been tracking the market, doing a little bit better but not much. Its just that the market is going up and down like a yo-yo.

While I am happy to have gained back the losses I took over the past couple of weeks, this whole dynamic makes me uneasy. Too many extremes for my liking. In my investment account, which is where most of my risk is and the one I track here (its also by far the most fun one to write about) I’ve taken down some exposure over the last few days by reducing some positions that seem to be the most prone to gyrations in this market. Stocks like Ocwen, Nationstar, Aercap and the like (note that I wrote this over the weekend and had reduced my servicing positions before the Ocwen settlement today. Today I sold Ocwen entirely at the open, being a little surprised that it was trading at $19+, bought back some Nationstar at a little over $28 later in the day and then bought back a bit of a position in Ocwen at the end of the day on hope of a short term bounce).

Overall, my exposure to the market is not as high as this blog often makes it seem. I blog about one account and that is the one where I am willing to take the most risk. I press in this account because I also will change my mind and cut my losses without remorse if things turn sour. In some of my other accounts I take care of I have a much more conservative bent; most are around 30% cash right now. My own RRSP account is close to fully invested, but everything there pays a dividend and very little is what I would call speculative (as an aside, New Residential is the largest position I hold in that account). I am not so sanguine about the outlook as my positioning here sometimes suggests.

What I worry about

On the contrary I am quite torn about which way we go from here. There are positives. The US economy is picking up. 2015 could be the year that household formation in the US finally makes its long-expected uptick. Lower oil prices will have a positive impact on spending, on emerging economies, and, if everything were to turn out just right, could be the boost needed by Europe and Japan that accelerates them out of their moribund state.

But there are also negatives. There is that same moribund state of the economies of Europe and of Japan, the questions about China and the rest of the emerging world and their mostly weakening growth rates. One could argue that all the slack in activity is responsible for the plunge in oil in the first place (the demand side has just not lived up to expectations).

I also am sympathetic to the “how can oil fall $50 and nothing else blow up?” thesis. We already saw a tremor on Tuesday, as the Russian Rouble went on tilt. I’m still not sure what pulled Russia off of the brink the next day (which likely led to the 3 day rally that we saw); it seemed that the Russian Central Bank actions were universally derided. I saw only one analyst comment that it was the right thing at the right time. Most said it was far too late, though admitting the magnitude of their move as being quite impressive. But what appeared to be a burgeoning crisis just kind of died away in the night and everything was ready for takeoff the next morning. Maybe it was just lucky timing as oil seemed to bottom that day. I don’t know. It does illustrate how quickly things can go sideways.

The other thing that continues to worry me is what is going on in Japan. While reading this months edition of the High Tech Strategist (a newsletter I have subscribed to for years) I was taken aback by what Japanese officials are saying.

First, Prime Minister Shinzo Abe, in response to critics that have been questioning his Abenomics policies (essentially Japan’s own massive money printing program), said “I am aware that critics says Abenomics is a failure and not working but I have not heard one concrete idea of what to do instead… Are our economic policies mistaken or correct? Is there another option?

A second comment, from Koichi Hamada, known as the ‘godfather’ of Abenomics, got to the heart of the matter; “In a ponzi game you exhaust lenders eventually, and of course Japanese taxpayers may revolt. But otherwise there are always new taxpayers, so this is a feasible ponzi game, though I’m not saying its good.”

Taken together I would condense these thoughts into the following comment: The highest ranking Japanese officials admit that they are running a ponzi game, that the primary reason to keep doing so is because there really isn’t any other alternative and that the stakes of it not working are extremely high.

I am not one to monger fear and am usually the first to look at skepticism when I read the usual suspects with their dire warnings of impending doom, but comments like these are scary stuff. Quite simply, there is a reasonable chance that things do not end well. And if they do not end well, given the size of the Japanese bond market, the size of the economy, the size of the Yen currency market, the consequences could be quite bad. While I do not profess to know enough to say when or how it will end, I mean Kyle Bass has been talking about the denouement of Japan for 4 years now and yet here we stand, I do know that these sorts of things tend to end with such speed that adjustment is difficult.

95% of my capital is allocated in positions that I can liquidate it without causing a market disturbance. If I wanted to I could wake up tomorrow morning and have almost everything sold by market close. These may sound like somewhat absurd precautions given that markets sit only a few points off of new highs. But I feel caution is prudent right now.

Changes to Positions

Hawaiian Holdings

I took a position in Hawaiian Holdings. I am late to the game on this one; I started looking at the stock in October when it was 40% lower, got scared off of it and other airlines because of my unfounded fears about Ebola, and then began to look at it again in late November. I watched it continue to go up, waiting for a pullback that never happened, and finally added a position at $21 in the fist couple of days of December.

When I added the position I tried to ignore the fact that it had already moved so far, so fast and focus on why I think the move might only be half done. Hawaiian Holdings remains cheap compared to its peers, trading at a little less than 5x its trailing twelve month EBITDA. So even before the move we saw in oil, one could make the argument that there was upside left in the stock. With the move in oil, that argument is made all the more stronger. For instance:

- From the third quarter 10Q: As of September 30, 2014, Hawaiian Holdings had hedged approximately 65% of our projected fuel requirements for the remainder of 2014 with heating oil puts and swaps.

- Again from the 10Q, Hawaiian Holdings total amount of fuel derivative contracts were 93,000 gallons as of Q3, so presumably there is about about 39,000 gallons hedged for Q4. That means that about 54,000 gallons out of 260,000 gallons are hedged for 2015

- Here is their fuel consumption and costs in Q3:

- Gulf Coast jet fuel is trading at about $1.80 right now

In rough terms, for 200,000 gallons of fuel used in 2015 Hawaiian Holdings will see a benefit of more than $1/gallon. All else being equal the benefit to free cash would be $200 million. The market capitalization of the stock is about $1.3 billion at Friday’s close.

Its pretty straightforward to connect those dots and conclude that if oil prices hold in the $60’s for a few months, and the perception begins to materialize that they are going to stay at these levels indefinitely (whether or not that perception turns out to be flawed is another story entirely, but a lot can happen from here to there), that Hawaiian Holdings could see a material re-rating on this additional cash flow generation potential.

The obvious counter-argument is that all the gains will be diddled away by pricing pressure. That might happen at the margin, but I don’t know if its going to happen quickly or near the full extent of the gains from reduced oil prices. Load factors are at 10 year plus highs, and as the chart below (which shows U.S. Airline load factors) suggests, I think we are running into a top end limit of just how high load factors can realistically go, while the bottom end has already been squeezed significantly as seat management from the airlines has improved. Given their strong position, I’m not sure how many airlines will feel the short term benefits of passing on fuel cost improvements to customers outweigh the revenue declines.

Adcare Health Systems

I also took a new position in Adcare Health a couple weeks ago. I took my position before this SeekingAlpha article came out, but between the article and the comments it does a decent job of explaining the idea. Adcare owns and operates skilled nursing facilities throughout 8 states scattered throughout the eastern United States. If we were still in the pre-Extendicare deal period, I might be inclined to look at the number of beds that Adcare owns (4,200), look at the the enterprise value of the company (its about $225 million after the recent jump up that occurred after the SeekingAlpha article), say that $53,000 per bed is a pretty low valuation so there’s lots of upside and leave it at that. But as we know from Extendicare (as well as some of the other deals done over the last 12 months), a bed is not a bed is not a bed. It’s all about profitability of the bed.

With that in mind, what makes Adcare interesting is that they are changing their business model from an owner/operator of skilled nursing beds to being simply an owner of the facilities, to which they will lease out to other operators. A model that will be much more profitable for the company. Adcare identified the benefits of this transformation in the following slide of their July strategic shift presentation:

If Adcare can achieve their EBITDA goal, the business is trading at less than 10x EV/EBITDA. Competitor leasing companies seem to trade at anywhere from 13x to 20x EBITDA. The multiple is high because as a strictly leasing business, the risk associated with operating the facilities, lawsuits from patients, and all that good stuff is removed from the equation, yet the underlying occupancy is relatively immune to economic gyrations. We’ll have to see where Adcare winds up being valued, but I think its reasonable to think it will be attractively higher than it is today.

Avid Technology

I took a position in Avid Technology, a beaten up software company after I got the idea from this SeekingAlpha article. Avid develops software for creating video and audio content. This is higher-end software, something used by professionals and serious enthusiasts.

In 2013 Avid had to restate its financial results due to problems that were found with revenue timing. The lengthy delay of any new financials caused the company to lose its compliance with NASDAQ, which led to its delisting from the exchange. The stock collapsed to as low as $6 per share as a result.

I took a position after the company had finished restating its results but before it was listed back on NASDAQ. My original hope was that there would be a pop with the NASDAQ listing. This unfortunately didn’t happen; the stock had been moving up in the months before and I guess that move captured the inevitable relisting.

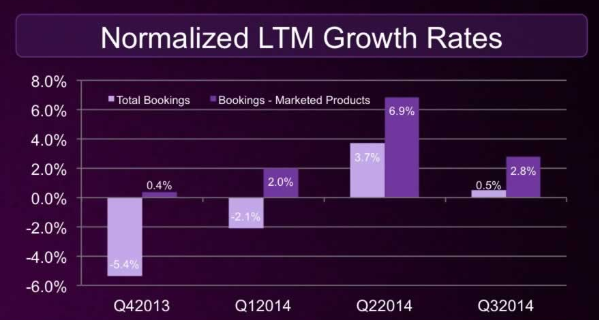

Nevertheless the stock remains cheap enough that I plan to hold onto it for the time being. The new management team appears to be turning the ship around. Bookings have stabilized, as the chart below indicates.

More importantly, bookings from marketed products, which refers to the remaining active product line (current management purged a number of lower margin products after taking over the reins), have been in positive territory for three quarters now.

In the third quarter the company generated $17 million from operations before working capital changes. Capital expenditures were $5 million. The company has a market capitalization of about $530 million, so if they can prove that a free cash flow run-rate of $50 million is sustainable, I think there is still upside left in the stock.

Oil Stocks

In the last few weeks I took my oil exposure up but a lot of the increase is a trade and I don’t have a lot of conviction it will stay this high. I moved my exposure up not because I saw the rally coming, but because a few stocks got down to levels that I had trouble passing up. I figured that when a bounce did come, they would probably be able to bounce above the levels I was purchasing them at.

I took a position in Mart Resources after it dropped to 58 cents. This, somewhat amazingly, was still nearly 20% too soon as the stock would continue to drop into the 40’s in the ensuing days. Nevertheless it just seemed that given the news flow coming out of Mart (the new pipeline, new zone, ramping production) the price shouldn’t be dropping so precipitously. I also ran some numbers and figure that at $60 oil, with the additional production from the new pipeline and new wells, they should be able to maintain the cash flow level they had when oil was $100+.

I also added Penn West. I’m following Nawar Alsaadi into this one. He’s written a number of interesting posts on the company on investorvillage, with this one being particularly insightful with respect to what might come next.

I still look at both of these positions as being rentals more than investments. They both have been clobbered, they are both companies I follow reasonably closely and have some confidence that nothing company related is going to whipsaw me in the short term, and so I thought they were primed for a bounce. We’re getting that bounce and I don’t know if I’ll hold either for much longer.

Ellington Financial (EFC)

I took a position in Ellington Financial after the company dropped twice, once before they announced their book value for December 1st, and once after. I actually bought this one at a little over $20 and then doubled up on it in the $19’s. The yield on the stock is over 13%, the book value that led to the drop was $23.35, which means that I was buying the stock at a 15% discount to book.

Ellington is typically considered an investor in residential mortgage securities, and while this is still their main business, they are in the process of expanding their scope into other asset classes. In addition to residential mortgage securities they have positions commercial mortgage backed securities, commercial loans, asset backed securities, non-performing loans, loan originators and a number of short positions in corporates via default swaps and in REIT equity. Because Ellington is not a REIT they really don’t have any limit on what they can invest, with their argument being that this frees them up to hedge their positions more appropriately and go after the opportunities where ever they lie.

Admittedly the company is a bit of a black box to me. I am really relying on the track record of the management team and the assumption that the track record can be projected forward. That track record is quite good.

One of the reasons I took the position was that the company has a reasonable sized short on corporate CDS. Their corporate CDS short was $170 million at the end of the third quarter, about twice the short on MBS and about 22% of their non-agency long position. I got the impression listening to the third quarter conference call that some of that hedge is in the high yield indices, which were collapsing last week before recovering along with the rest of the market. If oil stays down at these levels I would expect this short to move more sharply to the downside then their non-agency longs.

DirectCash Payments

Finally I took a new position in another Jason Donville pick. I really like this one and am going to write it up in more detail later.

Argonaut Gold

I broke my rule by adding to a losing position with Argonaut Gold. The fall in Argonaut has been something to behold. I bought the stock at a little over $2 and then watched it fall to under $1.40. At that point, having kept off the trigger the whole way down, I decided to double down because it was just getting ridiculous and I suspected it wasn’t coincidence that the move coincided with tax loss selling and the removal of the stock from a TSX index. While this has often proved to be a bad move, this time it wasn’t, at least so far, and the stock has recovered some. I also started a small position in Timmins Gold. This may or may not be the right time to invest in gold stocks. I am treading into these waters because the stocks have been pummeled while the price of gold has been extremely resilient in the face of a very strong U.S. Dollar over the last few months. If gold was going to crumble, wouldn’t it have done so by now?

As for stocks I sold, I exited my position in Rex American at a loss. I got into the stock at $70 and exited at $63, so I took a 10% loss overall. As much as I want to believe in the ethanol story, that more gasoline consumption will necessitate more ethanol demand (given the 10% blending margin), I just can’t do it with RBOB gasoline trading only a little over $1.50 per gallon. Meanwhile corn prices have been surprisingly strong and right now at $4.10 we would need to see ethanol back over $2 to really make these stocks viable investments. That seems unlikely to happen. It really goes to show what a volatile industry this is; profits can go from one extreme to another in a few months.

I also reduced my position in MGP Ingredients. This has been a great stock for me, has more than doubled since my purchases in August/September. But it is also a horribly illiquid stock and I have lived in fear of a bad event that would leave me a bag holder. Do I wish now that I had held my entire position the whole way up and been able to book the extra gains? Of course, but that simply would have been too much risk. At this level with my original position size the stock would be a 15% position, of which the result would be a lot of tossing and turning in bed at night.

Finally I exited my position in Dixie Group. Dixie remains a decent turnaround story and if it dips I probably buy it again, but when I reviewed where the company was at I still saw at least another quarter of slogging before we start to see some really positive results. Based on the current numbers its as easy to make a case for $7 as it is for $10. In this market this is the kind of stock I want to be really careful with. So I sold.

Portfolio Composition

Click here for the last twelve weeks of trades.

{kind=link}

Note that subsequent to posting I updated the post with a short comment about DirectCash Payments. DCI was another stock I bought in the last month but forgot to mention in the original post.

I am shorting Avid. I think that their accounting was fine before the restatement and egregious after the restatement. The deferred revenue doesn’t make sense. If you buy an Avid product, you hope that Avid will continue to release patches and updates. However, if Avid does not do so, I do not believe that the customer has any recourse (unless you’ve bought a service plan, which most Avid customers don’t).

If management didn’t suck, I would not be shorting Avid. There are some great assets there (or used to be). But clearly management destroyed the golden goose behind Sibelius (all of the developers left or were fired). Avid isn’t innovating as quickly as its competitors, and it has a lot of competitors. It no longer makes ‘big iron’ systems that cost five or six figures… which is what it originally did.

Thanks for the heads-up Glen

I love your blog Lane. I’m glad to see that you’re back. I definitely understand how this investing game can be frustrating from time to time, its a fickle mistress :).

I was the one who was posting in the comments section of the ADK article about the conflicts of interest in the board and the questionable track record of the CEO. Make sure to keep a close eye on them and their execution. I am very long ADK as well, though not as long as I would be if I was more comfortable with them.

You might want to take a look at CORR. that’s another one of my bigger holdings. There’s a couple of articles on it over on SA that I suspect you will find interesting.

In case you’re interested, I blog about special situation investment ideas over at The Mötley Fool from time to time. I love this stuff.

http://caps.fool.com/Blogs/ViewBlog.aspx?t=01001019292467236494

Happy Holidays!

Jason

Thanks for the info and the link to your blog. I’ll review CORR for sure. I did read your comments about ADK, certainly worth keeping in mind. The business plan seems so clear though, and on the last CC they seemed to be rigidly sticking to the script of what they were going to do and so thus far at least I’m pretty happy with what I’m seeing.

notice you also exited Jones. You were very positive about it. Might you be considering a re-entry?

I still think the company is a very good operator and the wells they continue to drill look to be excellent. But as far as companies I am looking at as a way of playing the bottom in oil, I am less inclined to go with them because they rely on natural gas and condensate prices quite a bit and I am much more inclined to think that the price of oil recovers in the next number of months than I am to think that ng stages a rally.

would be interesting to know why Cohen increased his stake: http://www.insidermonkey.com/blog/jones-energy-inc-jone-silicon-motion-technology-corp-simo-and-rcs-capital-corp-rcap-point72-asset-management-increases-stakes-337382/