My REE Bet: Lynas Corp

When I was looking for ways to play the price rise in rare earth elements (in particular neodymium and praseodymium, or NdPr) I almost skipped by Lynas Corp. It traded on the Australian market (where I cannot buy stock) and the OTC market in the United States (where I don’t like to buy stock). It was a penny stock. And when I dug into the story I found there were over 4 billion shares outstanding!

It didn’t strike me as an ideal vehicle.

But after scouring through the REE universe, I came back for another look. I had to. The thing is, the company is pretty much the only miner of rare earths outside of China. I found some companies with deposits, and some with technologies for better extraction, but there aren’t really any other options if you want a company that is going to see direct upside from the price rise of NdPr in the near term.

Background

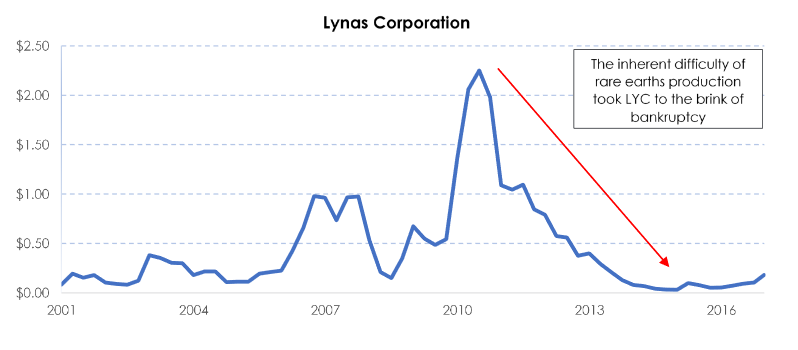

I mentioned in my last post that mining rare earths is difficult. The history of Lynas is an example of that. The company started mining at its Mt. Weld mine in 2013. It was immediately plagued with operational problems. This wasn’t helped by collapsing prices for rare earths. The stock, which peaked at over $2 during the rare earth boom of 2011, collapsed into its current penny stock status:

As I read about the company’s history the theme that came across was that they were an operating disaster until the current CEO, Amanda Lacaze, came on board and began to turn things around. Since that time she has slashed production costs and restructured a crippling debt burden.

“When I joined, production was unstable. We had high costs and were very cash consumptive. We had to reset our cost base and improve our operating performance while dealing with a market that was significantly less profitable than before.”

The company started to see better results in 2016. Then, in October 2016, they restructured their debt and reduced interest significantly.

Unfortunately, along with the restructuring came dilution. The strike price on the existing convertible debt of $225 million USD was reduced to 10c AUD. This meant that full conversion of the debentures would result in 2.67 billion shares being created.

But that’s what you get when you are trying to survive. The important thing is that they did survive. Now are the company best positioned to thrive as the REE market recovers.

Capitalization

Fully diluted Lynas has 7.1 billion shares. Once the convertible debt is gone (it undoubtedly will be converted into the stock) $200 million in long term debt will remain. The fully diluted market capitalization when I bought the stock (at 16c) was about 1.1 billion USD. They have $67 million ASD of cash.

Operations

The company has a single operating mine, Mt Weld. The mine produces material via the Central Lanthanide deposit. Reserves at Central Lanthanide are 9.7Mt of rock at a 10.8% rare earth oxide (REO) grade (from this report). Below is a table of reserves at Central Lanthanide:

In addition to reserves there is another 15Mt of resource at Central Lanthanide at 8.8%. A second, underground deposit called Duncan has 8.2Mt at 4.7% REO grade.

The deposits host a fairly typical distribution of REOs:

Ore is mined from the Central Lanthanide deposit and taken through a flotation circuit on-site to get a rare earth oxide concentrate.

The concentrate is shipped to Malaysia for processing. The company has an advanced materials plant in Kuantan, Malaysia where the concentrate goes through chemical processes like cracking and leaching and solvent extraction to separate the individual REEs from solution and create an end product oxide.

The plant in Malaysia has been controversial. Some locals in Kuantan don’t want an REE processing plant in their back yard. At the time it was built, maybe in part because of the REE mania that was in full force, it became a media story. The protests held up development. As this report points out:

The campaign managed to attract a lot of international media attention and stopped bigger contracts being pursued by major buyer. Lynas share values plummeted due to negative publicity and financial risks and because prices of rare earth elements dropped.

I can’t be sure of course, but it seems like some of the conflict has died down. I can only judge that the media stories I have read (which admittedly are in English and so may not be representing the entire picture) are more balanced and less common in the last few years. However I did see a comment that the upcoming Malaysian election this year could refuel some of the protest

Production

As Lynas has gotten the levers of production under control, volumes have improved. At the same time direct mining costs have dropped by about one-third since 2015.

The Mt Weld mine produces 2kg of other REEs for every 1kg of Nd. In Fiscal 2017 the mine produced 5,200t of NdPr.

While NdPr accounts for one-third of the production from Mt. Weld, it is the source of most of the revenue. Sales in 2017 were $257 million AUD. Sales of NdPr were around $225 million.

What’s the Upside?

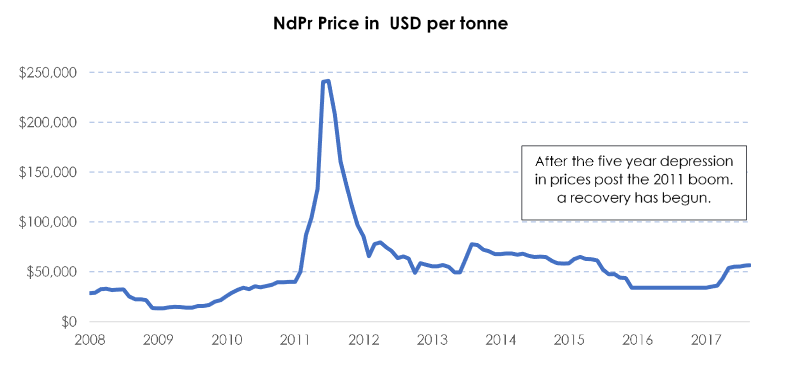

The upside here is leverage to NdPr price increases. Below are NdPr quarterly prices from the Lynas full year report ending June 30th.

There was a slow but steady uptrend in prices. Since June, however, prices have jumped significantly. I talked about reasons for the jump in prices in my last post.

FOB prices excluding VAT reached $65 USD/kg over the summer.

What’s really fun about mining companies is that their costs are essentially fixed with volume. So when a company sees a step change in price, the incremental revenue goes straight to the bottom line (less any taxes of course).

Every $10/kg change in price with 5,200 tpy production is about $50 million USD of extra operating cash (before tax) beyond what they currently generate. Lynas is hinting that they can get to 6,000 tpy of production, which would add another $8 million USD per $10/kg on top of that.

Here was an estimate I found from one analyst that gives a picture of sensitivity of net asset value to changing NdPr prices.

A second analyst, Newgate Capital, forecasts $230 million of free cash flow using $70/kg for NdPr prices.

A second analyst, Newgate Capital, forecasts $230 million of free cash flow using $70/kg for NdPr prices.

Worth noting is that in the Newgate estimate assumes a 30% tax rate. In note 12.2 of the year end financial statement the company notes the very large unrecognized deferred tax assets that are carried ($785 million ASD, from years of losses). I am not positive how efficiently these can be utilized, but they should represent significant tax credits. So I think (and I might be wrong) that most of the operating cash flow will go straight to the bottom line for at least a few years.

Buying the stock on the OTC

There are two symbols for the stock, LYSDY and LYSCF. The former is an ADR and the latter is an OTC traded share. I don’t think there is any real difference between the two; they are both 1:1 Lynas share equivalents. But the ADR is typically more expensive. I think this is because it’s more liquid. I haven’t had much luck buying the OTC traded share, even when I put in a bid above current it often gets ignored. Maybe its my brokerage? While I have a few shares of LYSCF, I have mostly paid up for the ADR.

Conclusion

There are risks here. One risk is that Lynas Malaysian plant has not been without controversy. There is always the chance that Lynas becomes a political football in Malaysia, especially given any upcoming election.

A second risk is that REE mining and extraction is hard. It’s the bull case and the bear case. Just as I think its going to be difficult to see much of a supply response, there is always the potential that Mt Weld has a hiccup.

There is also the potential for technological advances that limit the use of permanent magnets in the growing electric vehicle or wind turbine applications.

A fourth risk, maybe the biggest, is that the whole story depends on China. There’s no question that China can derail the REE rally if they decide to loosen the reins on illegal mining or flood the market with stockpiles.

But as I pointed out in my previous post, there are reasons to believe that won’t happen. I’m coming around to the idea that the price of NdPr has, over the last few months, not so much as spiked as it has started to re-establish a supply/demand equilibrium that will encourage investment that is not illegal and not environmentally toxic. If that’s the case, then its sustainable, and there is a lot of upside in Lynas in my opinion.

Keep in mind that even with the jump in prices, NdPr is still below what it was at a few years ago and not even close to the bubble levels it reached in 2011.

I don’t want those bubble levels to return. That wouldn’t be in the best interests of anyone, as demand would be destroyed. But I would be fine with a consistent rise on the back of rising magnet demand.

As well, given that Lynas is the only producer outside of China, and given that in the past various governments have raised the issue of REE dependency. There was this 60 minutes segment from 2015 (as an aside, sort of, I would highly recommend tuning into this documentary, in particular to check out the horrible scenes of the landscape around Chinese REE mines and description of the “relocation of entire villages” around the 6 minute mark. It gives me resolve in my thesis that China will be firm about ending this sort of mining).

More recently the DOD looked for ways to manage the “national security risk” posed by the REE supply chain. The collapse in price has mostly alleviated these concerns. But with prices rising again, it would see to me that a company like Lynas, with operations outside of China, should command some sort of a “rareness” premium (pun intended).

Look, I could be wrong about this. Lots of things could go sideways. I’ve tried to outline a few. But if they go right I think the stock has significant upside. So I’m willing to make a bet.

FWIW just saw this artlcle this morning. Not much detail, who knows what costs will be and surely years away but technology always going to be a risk: https://phys.org/news/2017-10-magnet-deficiencies-conventional-samarium-neodymium.html

I’m biased because I own a lot of shares, but for a similar type of story but much earlier in the process I’d recommend taking a look at GeoMegA Resources (GMA.v). With about 80 million shares outstanding and priced around 8 cents per share, we’re looking at a very highly leveraged REE story. Until a few days ago I’d have been harder pressed to make a strong case for GMA, especially given several bumps along the road these past few years which have understandably tested investors’ patience and caused the market to question the company’s credibility. But, with the recent news that Geomega’s prototype can now seperate 1kg per run at 95 percent purity built with off the shelf equipment its now emerging as a real contender with its proprietary seperating technology that will allow GMA like Lynas to control its own fate. Next up GMA needs to achieve 99 percent or greater purity. Then build it much bigger and move beyond the prototype phase. I think the very small pool of investors aware of GMA expect this will take a long time and prove expensive. I’m a bit more optimistic. For me it isn’t hard to imagine GMA trading many multiples of the current share price over the next couple years as it advances its technology, scales and proves to the broader investment community that it can use its technology to generate meaningful cash flow through processing Industrial residue all while moving forward with plans for a much larger scale mining operation in North America via its very large Montviel deposit that should eventually show a very healthy Npv.

Thanks I will check it out.

As long as you are looking at mining companies it might be worth looking at MOGLQ. Coking coal miner in Mongolian that exports to China. Production is way up this year with ban on NK coal to China and China reducing its production of coal.

Sure Thanks!

This one is unrelated to electric cars, but Data communications management looks interesting. $26m cad market cap, and adjusted ebitda this year of 18-20m, and probably higher next year. Boring business that seems to have been stabilized, and looks like it could be a big winner once income statements clean up. Insiders participated in recent share offering as well.

Thanks I’ll check it ou

What is your take on CleanTeQ (from your retweet)?

Basically a Cobalt/Scandium play, but I wonder how much is already priced in. The stock had a big run already after this summers consolidation…

I don’t actually know anything about the company. I was just retweeting the slide which was showing how much nickel demand would grow. Is CleanTeQ a miner?

Rather Explorer. Their Ressources are basically Cobalt, Scandium and Nickel. AND they have a proprietary extraction method.

Here is a SA article about them.

https://seekingalpha.com/article/4071608-clean-teq-friedlands-nickel-cobalt-scandium-gem

By the way: Nickel. Take a look at Norlisk Nickel. High dividend yield and insider ownership.