Sticking with Zargon

I have owned Zargon Oil and Gas for almost two years now and it has been one of my worst performers. I bought a small position after the company announced the sale of its South Saskatchewan asset in July 2016. I added to the stock early in 2017 after the company announced a redemption auction for its convertible debentures whereby they would either redeem the debentures in full or exchange them for longer dated (December, 2019) lower strike ($1.25 per share) debentures.

Neither of those purchases have worked out so far. I thought the asset sale would reduce debt and bring back interest in the stock. I thought the debenture exchange would be a catalyst. Maybe most importantly I thought the environment for oil stocks was improving, so it seemed a reasonable bet that Zargon would benefit.

As it turned out I was about a year too early. The stock languished through much of 2017, falling from 80c to under 40c at one point.

Why Zargon?

Zargon is not my biggest oil position. It’s one of a basket of stocks I have been holding and adding to. In the last few days I added Black Pearl Resources and ProPetro Holdings to that list.

So why am I choosing to write about Zargon and not my other larger holdings? Well for one, apart from a few Seeking Alpha articles Zargon doesn’t get much attention. I could write about Whitecap or Gear Energy but you can get all the information you need from brokerages reports already.

Second. with the prospects for oil improving I decided to really dig into Zargon again a couple weeks ago. The stock has under-performed for so long and I wanted to come to a conclusion as to whether to keep holding the stock or move those dollars into another E&P.

I decided to stick with Zargon. Here’s why.

Zargon operates 3 assets. They produce about 500 bbl/d from their Little Bow enhanced recovery project, another 300 bbl/d of conventional heavy oil at Little Bow, about 400 bbl/d of medium/heavy oil from North Dakota, and another 1,200 boepd from various assets around Alberta.

Little Bow ASP

The Little Bow asset would be considered Zargon’s flag ship. The company produces 20-21° API oil from the Mannville formation at Little Bow, Some of this production is conventional, and some of it is an advanced waterflood technique called Alkali-Surfactant-Polymer (ASP) recovery.

An ASP is a waterflood recovery where the additional “A-S-P” chemicals are added to the water. The chemicals thicken the water and turn the oil into a more mobile foam. Together the thickened water and thinned oil mean that the oil moves more effectively than a traditional waterflood alone.

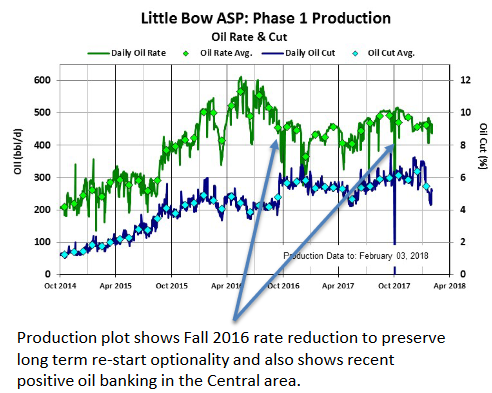

The problem with an ASP flood is that it’s expensive. The chemical costs alone are $6-$8/bbl. Zargon has corporate operating costs of $20/bbl and while they don’t break out the cost of the ASP, I am certain its around the same level. When oil was extremely low in 2016 Zargon suspended Alkali and Surfactant injections at Little Bow and shut in higher water cut producers.

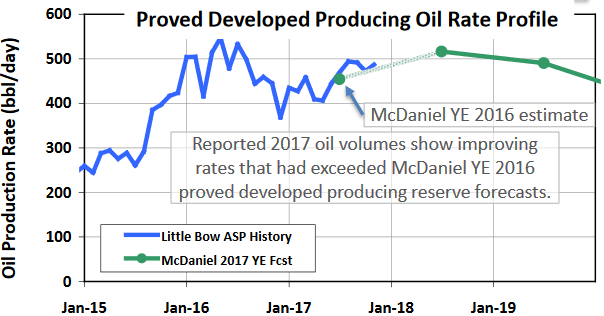

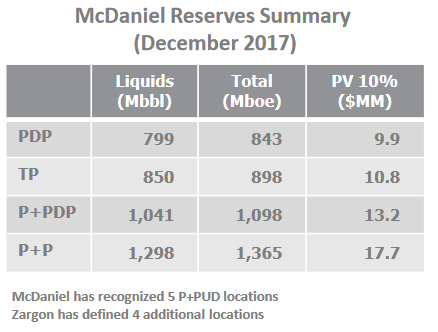

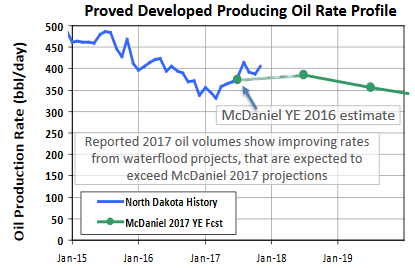

The good news is that ASP at Little Bow is long life and has a low decline. Zargon has examples in its presentation of a Husky Taber ASP waterflood and Gull Lake ASP waterflood where production has been fairly close to flat for 10 years and counting. Proved reserves for the Little Bow ASP were a little under 2mmbbl and proved plus probable (which includes the yet to be developed Phase 2) is 3.9mmbbl. At 500bblpd this is 11 year reserve life index for proved and 21 years for proved plus probable. In their 2017 reserve report McDaniel is forecasting an increase in production in 2018 as Zargon reinstates the full ASP flood and brings back on previously shut-in wells.

Little Bow Conventional

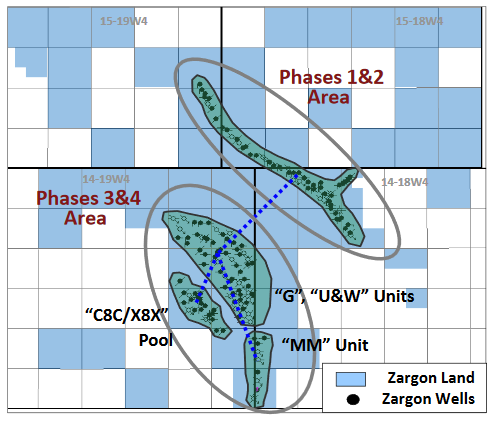

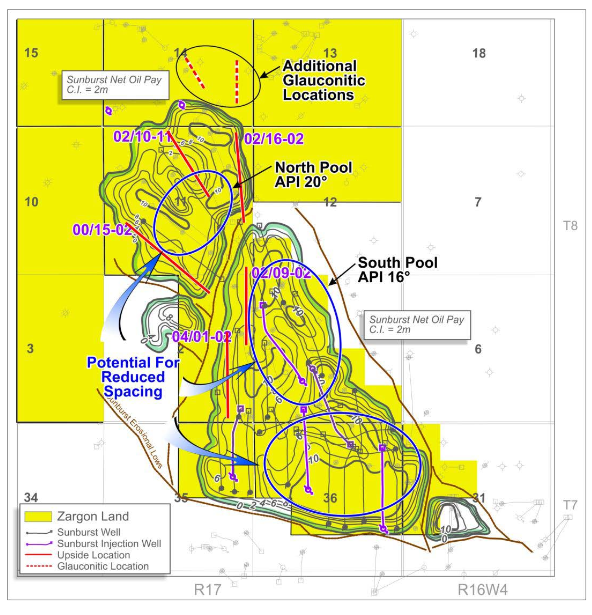

Zargon also has conventional oil production at Little Bow. This is from the “G” and “U” units in the map below.

Both the G and UW units are targeted as Phase 3 and Phase 4 stages of the ASP development. But for now the land is produced conventionally.

Together these pools produced 285boepd in 2017, 65% liquids. The company doesn’t list additional locations anywhere that I can see, so I have to assume this asset is going to continue to decline until the ASP flood is implemented.

Bellshill Lake

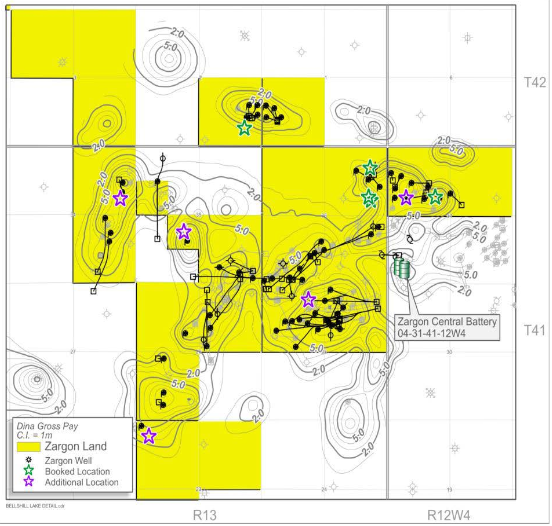

Zargon owns 21.5 sections (13,760 acres) of land at Bellshill Lake. Bellshill Lake is in East-Central Alberta, very close to Hardisty. They produce out of the Dina sands formation there.

Bellshill Lake produced 409 boepd, 94% oil in the fourth quarter. Bellshill oil has an API gravity of 27°API, so its firmly in the medium oil category.

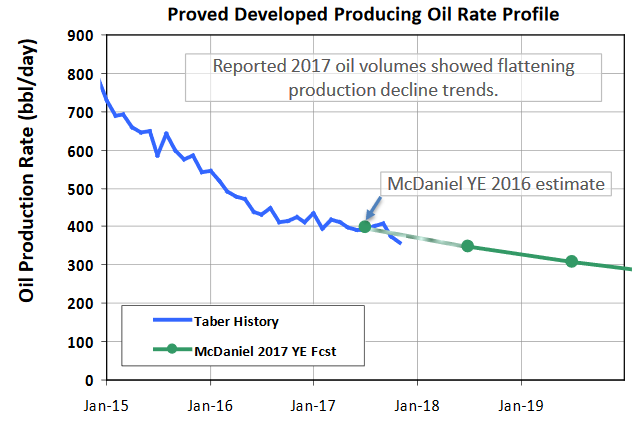

This is another low decline property. Based on the McDaniel decline (below) it looks like the decline on the field is 10-11%. According to the company the area has aquifer support, which helps support the low decline.

Zargon hasn’t drilled the property since 2014. The McDaniel reserve report booked 5 undeveloped locations and Zargon says they have 4 more. I believe these are all vertical locations. In the fourth quarter Zargon expanded the water handling at Bellshill Lake which will allow multiple “low risk, low cost well pumping optimization projects” in 2018.

Its worth pointing out that before the collapse of the price of oil in late-2014 Zargon was able to keep production at Bellshill relatively flat at 550-600 bbl/d.

Proved reserves on the property are 850,000 bbl of oil.

Taber

It looks like Zargon has about 90 sections of land (57,600 acres) about 30km south of the town of Taber. I say “it looks” because I’m counting sections of the map so I might be off give or take.

Zargon produces from a part of the lower Mannville Group called the Sunburst Sand. There are two pools that they are producing from, North and South. Both these pools are receiving pressure maintenance from waterflood.

The North Pool has a little ligher oil, 20 API, then the South at 16 API so again this is heavy oil. Both these pools are fairly mature, having produced over 50% of the expected ultimate recovery.

Zargon has drilled 30 wells into these pools since 2007, of which 5 are injectors. McDaniel has 3 more horizontal locations booked and Zargon has an additional 5 they have identified. I don’t believe they have drilled any wells here since 2014. They have also identified a Glauconite oil pool north of Sunburst.

Taber South is another low decline property. Based on the McDaniel estimate it looks like the decline is around 13%.

Proved reserves at Taber South stand at 1,144mbbl.

North Dakota

Zargon owns a scatter of land across Haas County, Truro County and Mackobee Coulee County in North Dakota. This was originally part of a larger land package that extended into Saskatchewan, but the Saskatchewan portion was sold in July 2016.

This isn’t Bakken land. I believe the focus on these lands is the Mississippian but I’m not sure which others are contributing. They have 97% working interest in 18.78 sections (12,000 acres) of land.

They produce about 400 boe/d from North Dakota. These are low initial rate, low decline wells.

The decline on existing production is very low, varying between 11% at Mackobee Coulee to only 4% at Haas.

Strategic Initiatives

Zargon initiated a strategic alternatives process in August 2015. Since that time they have sold the Saskatchewan assets for a pretty good price (at the time) but not done much else.

To be fair, that was perhaps the best choice. I’m sure that the value of their assets has risen significantly in the marketplace over the past few months. Even if the stock market doesn’t agree.

With the value of the assets rising, part of my expectation is that we start to see asset sales.

I don’t have many good analogies for the North Dakota assets. I searched but I didn’t see any sales in Bottineau county. In September 2017 Halcon Resources sold non-operated Williston Basin assets for $104 million of cash for $45,000 per flowing boe. But this acreage is in Montrail, Mckenzie and Williams county, and prospective for the Bakken, so I doubt its analogous.

With such low decline base production and a land package that can support more drilling I would think that the North Dakota assets should fetch at least $40,000 per flowing boe in the current environment. There are plenty of cases of oil assets in general selling for more than this (like the Cardinal purchase from Crescent Point of South Saskatchewan assets for $64,000 per flowing boe which I realize is not a great comparison).

If they can get $40,000 per flowing boe, that would be $20.5 million Canadian.

It might be worth noting (it also might not) that the company took down their February corporate presentation a number of weeks ago and has yet to replace it.

Paying off the Debentures

After the conclusion of the debenture redemption auction Zargon has $42 million left outstanding. These debentures pay 8% interest (works out to $3.68/boe) and mature at the end of 2019.

The need to work a deal for these debentures in the next year and a half make me think that asset sales are probable. The North Dakota assets seem like the most likely target.

I think these debentures are a real overhang on the stock. Zargon has over $40 million of debt but only a $15 million market capitalization.

Paying off a significant portion of the debentures would go a long way towards improving market confidence.

Heavy Oil

A big knock against Zargon is that they are a heavy oil producer in Alberta. And they are small. This makes them vulnerable to the swings in Western Canadian Select (WCS) pricing.

It’s also going to hurt their first quarter results. I am braced for a bad first quarter. WCS spreads were huge, which means the price that Zargon got for its heavy oil was not very much. To make it worse, Zargon seems to have hedged WTI on 1,000 bbl/d in the first half but not the spreads.

So it’s something to consider when trying to time a purchase. On the other hand it should be well known at this point, and spreads have come in dramatically in April.

In fact I’ve been doing some work on heavy oil and drawn some interesting conclusions. While pipelines are by far the best way to transport oil, rail cars are not a death knell to the industry. According to an RBC report that came out a few weeks ago, rail transportation costs are $11-$15/bbl whereas pipelines are $8-$9/bbl. That’s high, but its not crazy, “I have to shut-in my production and go home” high. Especially at crude prices like what we are seeing now.

In fact with the Canadian dollar at 77c USD or whatever it is at today, these Canadian heavy oil producers are probably doing better now then they were the last time oil was this high, when the CAD was closer to 90c.

The pipeline story gets so much attention that these details get lost. It made me rethink things, and made me add another heavy oil producer in Black Pearl in addition to Zargon and Gear.

Cheap compared to its peers

The other consideration that made me decide to stick with Zargon is that its quite cheap. Especially if oil prices can stay at these levels.

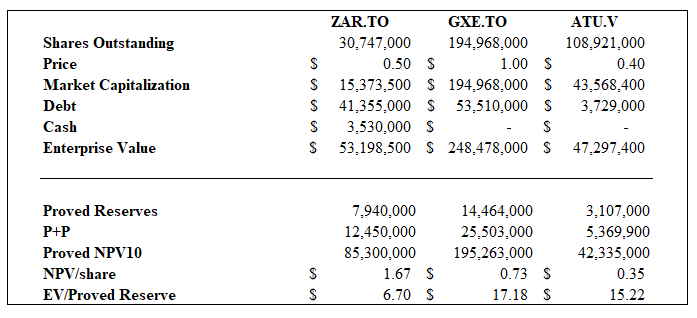

I am comparing the stock to two relatively close peers, Gear Energy and Altura Energy. Neither of these stocks could be considered expensive in its own right. In fact Gear is owned and touted by a number of funds as a cheap way of playing oil. GMP recently listed Gear and Altura as two of their cheapest names. I chose Altura because it does get brokerage coverage and because its roughly the same size as Zargon.

Now for the first half of 2018 Zargon is partially hedged at lower WTI and with no corresponding hedge on WCS spread. So first half results are not going to look nearly as good as this comparison.

But come the second half of the year, if oil prices and spreads hold, things should work out to about this level.

Yet Zargon appears pretty favorably, even cheaper than these two. The comparison below is at $65 WCS, so roughly $10/bbl higher than the fourth quarter. Costs are based on the fourth quarter costs of each company. I also estimated spreads off of heavy and light oil off of their fourth quarter pricing and for NGL pricing for Gear and Altura I just added $10/bbl to their fourth quarter pricing. I might be wrong with the royalties, I added $3 to the fourth quarter royalty because I didn’t want to dig into the complicated calculation of figuring out how it escalated with price.

Based on proved reserves and net asset value again Zargon looks pretty good.

Based on proved reserves and net asset value again Zargon looks pretty good.

Looking at cash flow, on an EV basis Zargon is comparable to Gear and Altura. On a per share basis, Zargon has a lot more torque. In fact they trade at about 1x P/CF on these price assumptions. On a reserve basis Zargon is very favorable, trading well under the value of its proved reserves.

Looking at cash flow, on an EV basis Zargon is comparable to Gear and Altura. On a per share basis, Zargon has a lot more torque. In fact they trade at about 1x P/CF on these price assumptions. On a reserve basis Zargon is very favorable, trading well under the value of its proved reserves.

The discount was justified when oil prices were low. Just look at the operating costs to see that Zargon is by far the higher cost producer. But if we really believe in these oil prices, I think you can make the argument that it’s time to peel it off.

Conclusion

Look I realize Zargon’s assets are not best in class. They are high cost operating assets mostly in land locked Alberta.

They are also extremely profitable at current oil prices. At $65 WCS the stock is trading at 1x cash flow.

Zargon spent $8.9 million on capital expenditures in 2017. On those expenditures they kept production pretty much flat (in the fourth quarter of 2016, after the sale of the South Saskatchewan assets, production averaged 2,449 boe/d). In the AIF McDaniel estimated $6.4 million in capex in 2018 in their proved reserves NPV calculation.

With cash flow of nearly $15 million (once the hedges in the first half run off) at $65 WCS, that works out to somewhere between $6-$8 million of free cash flow on a market capitalization of $13 million.

I decided that was worth sticking with. I actually even added a little more.

I think Altura (ATU.V) is a tough compare because they have an unlevered balance sheet that they could choose to accelerate growth and because they are proving up their biggest play this year they haven’t booked a lot of reserves.

That being said, I agree that ZAR is very interesting if they are able to sell an asset to redeem the debs or sell the company. The debs, ZAR.DB.A, also look good with about 50% upside to maturity (~25% YTM) and participation in the equity above C$1.25).

Yeah its true: the GMP report has Altura growing to 1,750boe/d by 2019, which seems a bit aggressive to me but nevertheless it is to your point. Whereas Zargon isn’t going to grow, at least not meaningfully.

You don’t like Altura because its reserve life? Because it trades at an incredibly cheap forward EV/CF multiple.

Sorry but what? I didnt say any of that did I? Where did I say or even imply that I didn’t like Altura?

I figured you didn’t like it because you don’t own it and it looks really cheap. While it is on your radar 🙂 . So I guess I assumed that by omission from your portfolio you like other oil names better for whatever reason.

I do own it, and you seem to know more about the sector, so that was why I asked.

Ok, I actually do own the stock just not in the account I try to track here.

If we could get to and stay over $70 WCS then I would think ZAR should be able to do at least $20mm corp cash flow (field likely up to $30mm). Don’t think it would be unreasonable to buyback 20% of the stock up to $0.70/share (6 million shares times $0.70 = $4.2 mm cash outlay with Dutch auction substantial issuer bid) At same time buyback $5mm of the debentures in the same fashion < $90. Use the other $10mm corp cash flow for low risk high return drill projects & water flood.

I would think it’s irresponsible to do a share buyback before the debentures are retired or they have a bank line to deal with them. Buying back the debentures also removes the potential conversion to shares at $1.25 so it’s like a buyback and it’s capital you have to spend anyway. Perhaps if they can get enough cash together they can come back to debenture holders and try to extend and redeem some like they did last time.

I’ve been telling them to do a buyback for a year now. But they said they can;t do it because of debentures.

Hi Lsigurd, I have two questions:

1) Are your “$ numbers” for Zargon in USD or CAD (Im having the same doubt when reading Zargons own quarterly statements)?

2) How do you arrive at the $1.67 for the NPV of Zargon. I assume you figure the convertibles will be converted at $1.25 (thus adding $42M from debt to NPV), whereby I get: NPV=(85.3+42)/(30.7+42/1.25) = $ 1.97.

What do you think happens to the converts? Will it have sufficient cash to pay at maturity? Issue more converts? Another restructure?

Well my hope* is that it doesn’t get to that and they sell the company or at least enough of it to pay back the converts before they come due. A lot is going to depend on the oil price. Its no sure thing, especially if oil prices come back down. I mean ZAR basically has no cash and no working capital, so its not the best cash flow situation. But thats also why the stock is so cheap. Its just that I think the upside is worth the risk for myself.

Curious if you have any updated thoughts? Stock price has drifted down with lower oil price and WTI-WCS differentials blowing out again to 30+ with ZAR now unhedged. Still seems like ZAR trades at material discount to oily-E&Ps (market seems like 40-60k boe/d) but seems like ZAR is capital constrained to do much of anything unless oil prices recover significantly…and the 2019 convert maturity is out there. Not sure what mgmt is waiting for on the strategic alternatives?

I just gave up on Zargon. I guess I’m just admitting I’m wrong, but its also because I have GXE and ATU that have the same heavy oil in Alberta issues. I am frustrated that I might be dumping it at just the wrong time but what can you do?

Fair enough, appreciate the honesty. What areas do you think went wrong? Any news which would change your mind?

I really didnt think spreads would be this wide. I also didn’t expect that they would have such high costs and that production would weaken as much as it did in Q2. They had kinda implied that what happened in Q1 was a one-off but it seemed like Q2 was a continuation of it.

So I know you have abandoned Zargon common but do you see any value in the debentures at this price?

Sorry about the slow response. I assume you mean in terms of the worst case scenario where the company goes bankrupt. Its really the only debt so the debs should be worth whatever you think the company is worth. The assets are worth something. At 50c on the dollar I would think Zargons assets are worth at least $20mm even in this crappy WCS environment. So my guess is that there is value in them.