Liqtech: Getting a Boost from IMO 2020

I owe this idea to @teamonfuego. He brought it up to me a couple weeks ago. Unfortunately, I was on vacation and I was slow to the punch. As it was I ended up picking up the stock at $1.10 on average.

Liqtech has been your typical little energy technology company. They have an interesting technology but have struggled to sell it into established markets that aren’t all that interested in new ideas.

The consequence is that the stock has spent years bouncing around with no real upward momentum, every year losing money and raising capital.

What they sell

Liqtech sells a suite of silicon carbide filter products. They’ve tried to break into oil and gas, into mining, even into pools and spas. But they’ve only had moderate luck. They have a small but fairly steady business selling diesel particulate filters (around $8 million a year of revenue). Beyond that they sell a few filter systems a year but never enough to break-even on a consistent basis.

From what I can gather, their lack of success is not because of the product. The silicon carbide filter is a better product for many industrial waste/purification applications than what is used right now. But that doesn’t always guarantee a win.

The problem has been getting a foot in the door. This article, from way back in 2014 with CEO Sune Mathiesen, describes the problem that the company has had in the past:

My initial, and most important focus point was to turn the Company around from being a supplier of membranes into a supplier of complete water treatment systems. Since LiqTech started commercializing its membranes in 2009, it has proven very difficult to convince system integrators to invest time and money in developing systems around our membrane technology. The reason is simple, most engineers know how to build a system around sand filters, polymer membranes or other well-known technologies, but they don’t know how to handle our silicon carbide products.

Beginning in 2015 Mathiesen made the transition from selling membranes to selling filter systems. They began to research and invest in building a full filter assembly so they could by-pass the system integrators.

Three years has passed and the stock hasn’t exactly lit the world on fire. But they’ve been slowly built out a product line of filter systems for various applications. And now one of those applications appears about to take off.

IMO 2020

IMO 2020 refers to new regulations from the International Marine Organization that come into effect in 2020. These regulations change the pollutant requirements of bunker fuel, reducing the maximum SO2 concentration in marine fuel exhaust from 3.5% to 0.5%.

About 60-70% of the shipping fleet uses a bunker fuel that has >0.5% SO2. The most common bunker fuel has SO2 of about 2.7%. The ships that use this fuel will have to do something about that by 2020.

The ship owners don’t have many choices. They can either switch to a more expensive low sulphur fuel or install scrubbers that clean out the SO2 from the high-sulphur bunker fuel.

The economics around fuel switching versus scrubbers is in favor of the scrubbers. Here’s a quote from Rudy Kassinger, consultant at Veritas Petroleum Services, from this article:

The cost of installing scrubbers is somewhere between $3 million and $6 million depending on the ship (though I have seen estimates that use a high-end number as much as $10 million). The payback on scrubbers can be 1-3 years. Most of the articles I’ve read peg the number at 2 years, which is not too bad.

So how does this impact Liqtech?

Liqtech filters are installed as part of the scrubber assembly.

Scrubbers can operate in open loop, closed loop or hybrid configurations. When a scrubber operates in an open-loop, sea water is used to remove pollutant from the exhaust stream. The sea water is then discharged back into the ocean.

But in harbors and in some regulated waters seawater discharge is not possible. In these areas a closed loop or hybrid system needs to be used where no polluted water is discharged.

The closed loop requires that the effluent water be filtered for re-use. This is where Liqtech filter systems come in. The silicon carbide filter is ideal for the application (in terms of durability, temperature resistance, corrosion and operating performance).

The opportunity for Liqtech is large. Each scrubber installation needs a filter. Ships require on average 1.6 scrubbers (so some need 1, some need 2). The shipping fleet is about 70,000 vessels. Some percentage of those ships will be retrofitted for filters. As well more new builds will include scrubbers going forward.

According to Goldman Sachs less than 500 ships have scrubbers installed today. Goldman estimates that by 2025 we should expect to see over 5,000 ships equipped with scrubbers. Other estimates are even higher. The IMO put out its own estimate (quoted in this WSJ article) forecasting 4,000 ships with scrubbers by the end of 2020. Liqtech said on their second quarter call that:

Analysts believe that by 2025 roughly 14,000 vessels are roughly 20% of the global fleet with have a scrubber.

Whatever the number, its meaningful to Liqtech. Liqtech sells the marine scrubber filters for about $450,000 a unit. At 1 scrubber per ship, the total addressable market is somewhere between $1.8 billion and $6.3 billion.

Liqtech has 72.7 million shares outstanding and no debt. So even after the latest run, its only a $87 million market capitalization company. The addressable market is truly multiples of the capitalization.

The obvious question is what sort of market share can they capture? Things look pretty good so far.

- In March they announced a framework agreement with “one of the world‘s largest manufacturers of marine scrubbers” for “an initial term for 2018 and 2019 and provides that more than 95 systems are estimated to be delivered”

- In April they announced a second framework agreement for “a minimum of 35 systems are estimated to be delivered during the initial term” of 2018 and 2019.

- Also in April they announced a letter of intent with “one of the world’s largest marine scrubber manufacturers”. This was extended in July. On the second quarter call they said the LOI was for 95+ systems.

On the first quarter call Liqtech said they were working with five or six of the largest scrubber manufacturers. They said on the second quarter call that they are expecting to see orders coming from other sources as well:

we believe that we see a lot of the orders in the future come directly from the shipyard operators. It doesn’t necessarily mean that — or it doesn’t mean that we’ll not see orders coming from scrubber manufacturers, it just means that I have told to several sources for orders in the future.

I’d make a guess that the 95 system framework agreement is with Yara, which is a large scrubber manufacturer. Liqtech has previously disclosed they have been working with Yara. A look at this Yara video shows a filter that looks pretty much the same as what Liqtech shows in their own presentation.

I’m not sure who the other 35 systems or the LOI are with. The list of scrubber manufacturers includes: Alfa Laval, Wartsila, Saacke, Yara, Puyier, DuPont, and Feen Marine. Liqtech has said there are 10 major manufacturers in total.

So what kind of impact is this going to have on the bottom line?

I think its going to be significant. Here are a few points to consider.

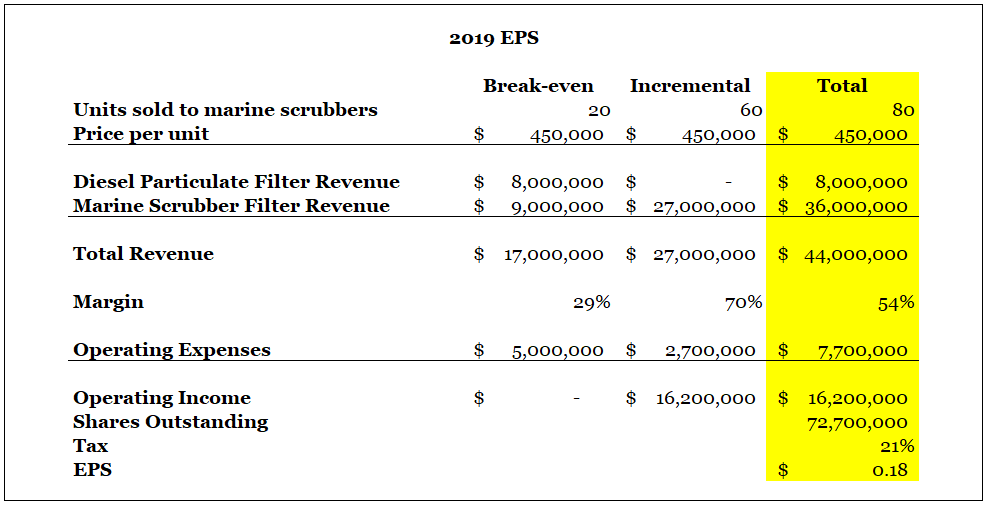

- The company says their break-even is $16-$18 million of revenue, on the sale of about ~20 filters systems for marine scrubbers

- On the second quarter call they said incremental systems sold should expect 70-75% gross margins and they have also said they expect 65% contribution margin from incremental sales

- The current expense run rate is $1.25 million per quarter

- There are $14 million of NOLs in the US and another $6 million in Denmark

I’m assuming they need to sell about 20 systems in 2019 to hit a break-even point at current run-rates. If the two framework agreements come to fruition they will sell 130 systems, heavily weighted to 2019. Let’s say they sell a total of 80, so 60 that are incremental to the break-even number.

I’m throwing in the 21% tax rate even though they shouldn’t be taxed through most if not all of 2019. Un-taxed EPS is over 23c with these assumptions.

Conclusion

One downside is that sales of filters to the existing marine scrubber fleet is not going to last forever. There are limits on ship-yard capacity which will extend the retrofits out to 2025. But probably some time around then (maybe sooner, maybe later depending on how things play out) the installs will taper off.

There will be continued sales from new-builds after 2025. There are 70,000 ships globally. It seems like for most markets (containerships, dry bulkers, tankers) at least 3% of the fleet is added every year. So that’s ~2,000 ships a year. On the first quarter call Liqtech said they expect to see a further uptick on the 30-40% of new-builds that are currently being built equipped with scrubbers. So the opportunity is not insignificant.

Also, by the time the retrofit opportunity is exhausted, and assuming everything plays out positively, Liqtech will have an install base numbering into the 100’s of ships.

I would expect it will be a lot easier to hock their product to big oil producers, power producers, miners, and municipal water suppliers with a resume that includes a major vertical that has accepted their filters in an extreme environment.

But that’s a long way off. For now, its enough to say that the stock is cheap if they can secure the expected number of deals from the existing framework agreements and have those agreements project forward, and it is very cheap if they can capture even more market share from other scrubber manufacturers and shipyards.

A second risk is that they start to see price pressure. They are the only provider of a silicon carbide filter but there is competition by way of centrifugal filters. Liqtech has said before they are the cheaper and better option. But as the higher volumes are borne out you have to expect competition. The margins I’m showing in the table above are admittedly very high, and unlikely to be sustainable in the long run.

A third risk is that IMO 2020 gets delayed. From everything I’ve read I don’t see this happening. But you never know.

The bigger upside is that they capture a larger share of the market. I’m assuming about 80 filters a year. The opportunity size is significantly larger (as much as 14,000 installs according to Liqtech) next 5 years.

The other upside is that I have to think it will be easier to sell into other verticals once they can come to these customers with a portfolio of installs throughout the marine scrubber industry.

Anyways, it seems like a pretty tiny capitalization for such a big opportunity. Worth a portfolio spot in my opinion.

Can you explain your model a bit more? The numbers don’t add up to me.

How do you get the incremental operating income?

You just add up column one and two. Other than that I don’t really know what to say? What are you expecting to see for “unit ecomics”? I don’t think you’ll find the company willing to break down what their costs are with more granularity.

yeah sorry, got something wrong there

just thought you might have found a unit margin somewhere, cause I didn’t

would be interesting to know and what it depends on like silicon carbide prices etc

Oh I see. Yeah I haven’t seen them talk about anything like that. But the 75% gms and 65% contribution margins are pretty much the unit costs after you get beyond the first few systems.

Also the 54% margin number?

CC:”Well, with the new Mark 6 system, we will see higher contribution margins moving forward. We actually think there it will be to realize large concentration margins of around 70% to 75%. Of course not all of that will dropdown but a significant part of it will. As we increased volume, more and more off that will drop down to the bottom line, and probably it’s going to be in the region of 55% to 60%.”

Did you mean these numbers?

Finally

“Unidentified Analyst

And so we’ll start to see the actual unit margins on the systems drop through pretty fully?

Sune Mathiesen

Yes. As we progress, as we see volumes increase, we will see that drop down, that’s correct.”

Do you have an idea about the unit margin?

Nice writeup Lane. The way I see it is its basically a Y2K type event. Just reading the scrubber announcements the past couple of weeks I think some of the shippers are starting to get antsy…as it gets closer to the event and if the spread between low and high sulfur fuel stays wide then I’d imagine the shippers start to panic.

And like we talked about, the ongoing new build opportunity could be $300 to $400M per year. Crazy numbers.

Thanks for the write up. This is a very interesting opportunity. Any thoughts on the odds of this company being acquired by a larger fish? Seems like a ideal acquisition candidate for one of the manufacturers…

I’ve heard others suggest it. I really don’t know. Do you think that being bought by one might lead others to look at technology alternatives?

Could be a possibility. I was thinking that it might limit the market for LIQT since its doubtful the manufacturer would want to sell to a direct competitor (or not without a premium price). Perhaps there are larger direct competitors of LIQT that would be interested? Are you aware of any other write ups on LIQT? I picked up some shares today and we’ll see how this plays out.

Is Australian Vanadium available for you to buy?

http://www.australianvanadium.com.au/

It has almost as much vanadium as Largo, but earlier stage and just 87M AUD market cap.

Thanks, I unfortunately don’t have access to Australian stocks

Do you have any concern that they run out of cash and need to issue shares again? Only having had a 5-min look at their recent financial statements their number of shares outstanding increased from 44.4m at March 2018 to 72.7m at August 2018 and based on their current burn rates their isn’t a large amount of cash on balance sheet. I don’t know at what discount those additional shares were issued but could think of this being a significant risk in the near term.

I do agree with your thesis and overall view on the company and that IMO2020 is more real than many people looking at the marine industry from the outside may expect it to be.

Not sure what you are saying. Why do you think they will run out of cash if the thesis plays out? I’d be interested in understanding how you reach that conclusion. Or are you saying that if things don’t play out positively they may run out of capital? If that is what you are saying I would agree, without question.

Any idea why the sell off?

The WSJ came out with an article on how the Trump administration will be supporting a paper that was proposed by some flag states back in August. The article also described how the administration is concerned about potential impacts of IMO 2020, particularly that it is being adopted in the year of a presidential election and that it might effect the price of oil.

The flag states that wrote the paper issued a clarification on thursday or friday as well. In it they specified exactly what they are asking for. My understanding of this (after having read it 3-4 times at least) is that they are asking for an experience building phase and assurances that ships won’t be penalized if they can’t get compliant fuel come January 1st, 2020.

When I read what the flag states are proposing in the clarification it doesn’t appear to me that it would impact the implementation and enforcement of IMO 2020 come January 2020. In particular their clarification says:

“There is no suggestion in the paper to delay or weaken the general enforcement provisions of Marpol Annex VI in a wholesale manner. Compliance with the 0.50% global fuel oil sulphur standard is expected to be enforced on 1 January 2020 in the same manner as the current 3.50% global standard (and the 0.10% standard within emission control areas (ECAs)) is enforced today.”

However this article (behind a paywall but you can get a two-week trial) suggests that there may have been more behind the flag states proposal than meets the eye. It talks about a coup that failed. It also goes on to say that according to one “prominently placed source in the industry” the [flag state] proposal is dead and won’t even be discussed at the upcoming IMO meetings.

So it is as clear as mud. We also don’t really know what is going on behind the scenes and we of course don’t know if the Trump admin has more at play then just supporting this flag state proposal. It also doesn’t help that other news sites have picked up the WSJ story but framed it that the Trump administration is looking for a “delay”.

I think that the characterization of this as a “delay” is incorrect if we are talking about the flag state proposal. The clarification written by the flag states (that I linked to above) clearly states that there is “no suggestion in the paper to delay or weaken the general enforcement provisions” and that the “paper absolutely does not attempt to change the standard, nor does it seek to delay the 1 January 2020 effective date”.

But I also don’t know for sure if what we are talking about is just the flag state proposal. I don’t think anyone knows for sure what exactly is being contemplated or going on behind closed doors. So when journalists start using words like delay in the headline, its easy to be scared off by it.

My personal guess (and it is a guess) is that a lot has gone on behind the scenes this last week. There was an article back in september about how the US was staying on the sidelines wrt the flag state paper because they said it was too vague. There were other articles saying the flag state paper was vague. My guess is this was intentional as the flag states were looking to get consensus around a bigger change wrt the fuel carriage ban for high sulphur fuel. That the US sided with the flag states one the same day that the flag states released their clarification seems pretty coincidental – it kinda suggests this is what they could get agreement on. And like I said, if I am understanding this clarification correctly, its not really that negative (but I could be wrong, I am as far from an expert in IMO legalese as you can get).

Nevertheless, the market prepared for the worst on Friday, both hammering Liqtech, refiners and fuel spreads.

I’m still trying to wrap my head around all of this. I only figured out much of what I have described here today and I’m still not really sure if I’m thinking about it right. I guess the one negative thing is that Trump’s administration is now involved and they aren’t necessarily predictable. So its hard to say how this plays out. The IMO Marine Environmental Protection Committee meets Monday, so this is all going to get ironed out then. That is also why this all came to a head on Friday with a bunch of articles coming out. There must be lots of positioning going on.

Anyways imo is still on track if not 2020 it Will be 2022 , i still think liqtech is a great oportunity

Offtopic im invested in canadian oil ( prob the worst performing industry right now ) and im wondering if you have any thoughts of wcs wti differentials possibly widening due to the Imo 2020 sulphur cap

Ive read some reports ( Ceri states differentials could go as wide as 32 post 2020 ) , maybe canadian oil is a value trap and wanted to know your take

Click to access LIQT-Investor-Update-Conference-Call-Transcript-10-24-18.pdf

Sounds pretty positive and to address one of the comments about it sounds like they are in good shape as far as cash position goes.

Yeah I think it was positive. There is more risk with what has happened at the IMO. On the other hand the stock has correct a lot which should price that in.

Maybe you can share you thoughts on a couple of questions I have…

Market potential:

1. The adoption of scrubbers has to some extend a self defeating effect for the producers of the equipment. The more ships that adopt the scrubber solution the narrower the spread between MGO and HFO should become in the future, which would then make scrubbers less economically compared tonlos sulfur fuil.

2. Although I see revenues and earnings from scrubbers to take off, I still wonder what a fair multiple for such a company would be given that their growth is concentrated on the next seven years and will massively flatten or even be negative thereafter.

Your model:

3. I read the transcript of the recent call and understand that we have to differentiate between system (450k per unit) and component (230k per unit) sales. So we will see lower sales per unit but a higher number of units with a slightly higher margin. I guess your numbers would not change dramatically for the bottom line, right?

Working capital:

4. The company claims that the current capital base (>4.5 Million) is sufficient to cope with future growth. I’m not sure if that is really realistic. How likely is another capital increase?

Thanks!

Thanks for the questions.

1. A couple points. First, assuming there is a point where its self defeating to install scrubbers I believe that level is high enough that if it happened LIQT will have benefited far beyond what is justified by the current share price. Consider that right now we are talking a couple thousand ships getting scrubbers out of a 70k fleet. And my numbers aren’t even assuming that LIQT gets most of those ships (ie. I don’t have the latest framework agreement modeled in there). Second, are you sure it would be self-defeating? Consider this – What are current HSFO to LSFO equivalent spreads (you have to use a gasoil equivalent for LSFO because there isn’t a true LSFO right now) and what would be the payback on scrubbers at those spreads? I was looking at this a month ago and thinking that at current spreads (so right now, with all ships still using HSFO) scrubber payback would still be pretty good. Isn’t this the worst case scenario for spreads after 2020? To put it another way, the reason ships aren’t installing scrubbers right isn’t because spreads aren’t favorable, its because they don’t have to.

2. First there is the new build opportunity – 60% of newbuilds are being installed with scrubbers. 1,000-1,500 ships a year get built I believe (I’ve never been able to pin that number down exactly, its always given on a DMT basis, not ship basis). So the opportunity is quite large. Second, I think the upside from the ramp could far exceed the share price on its own. Its tough to project because we don’t know yet whether LIQT will hold its market share through the build, how many scrubbers will be closed-loop or hybrid, etc, but if an optimistic scenario holds then the cash should easily exceed the existing share price by a fair bit. Apart from that there are other verticals where the exposure from being used in shipping will help give them a foothold to expand into – such as scrubbers for power industry, oil and gas flowback filtering, and the DPFs maybe. But I think the newbuild opp is going to be large. The bigger question is what does the regulatory regime look like in 7 years and have even stricter environmental regs come in.

3. No I don’t think that’s right. Consider that the new framework agreement is entirely incremental to my model. So you can basically add 80-100 units at $230K and 70% margin (they said higher margin and we know existing units at scale are 65% with the Mark 6 design so that’s my guess). So I think my numbers actually change pretty dramatically with these additions. Also, consider that my numbers of 80 are actually less than the other two framework agreements. I conservatively said 80 but if you read the transcripts LIQT said they expect 120 from these two.

4. Well they just came out and said they don’t need to raise capital this week. They said they had more cash then they had at the end of Q2. And soon they are going to be getting a tonne of cash from orders. I mean I don’t know what they will do and I agree $4mm doesn’t seem like a lot but it would definitely be a surprise to me if they raised at this point.

Thanks that was helpful!!

3. I‘m still confused by their announcements. What you are saying is that their announced three framework agreements? The latest was the one signed on October first which will lead to 80-100 filter components with 230k each in 2019. on top of that are the other two agreements that lead to up to 120 Mark 6 orders for 450k each? Is that correct?

I thought that the agreement signed October 1 was for a prior already announced order.

4. They might get some pre-payments from their clients but is that enough working capital to handle 44mm (modelled above) plus about 13mm from the latest order?

Thats right, they have announced 3 separate framework agreements. The other two were announced early in the year and should be ~$450k ASPs. This one was 80-100 at $230k ASPs. I’m pretty sure this latest one was with Wartsila. One of the earlier one’s was almost assuredly with Yara. Not sure who the second one was with, maybe Alfa Laval, but hard to triangulate with any certainty.

I really don’t know what to say about (4). The company said they don’t need capital. They do have some access to debt and they are getting cash from orders (ie the cash balance being up since Q2). You can believe them or not.

How did you figure out the latest agreement was with Wartsila and previous one with Yara?

With Yara they’ve talked about their relationship a number of times on cc’s. Yara was a partner when they developed the product. With Wartsila the CEO let it slip in one interview that it was the largest scrubber manufacturer, so that would be Wartsila.

I just listened to the Q3 conference call and I‘m still somewhat confused about the product pricing. The management was asked about the current backlog for 2019 deliveries and the respective pricing of these orders. They plan about 50 system deliveries for next year. These are complete filtration systems entirely produced by LiqTech which go for an ASP between 200 and 400k USD each instead of the assumed 450k USD which was published in the company presentation. For the orders from the framework agreements (I remember a figure of 120 over 2 years) LiqTech delivers the filtration component of a system assembled by their partner. Here the ASP is 230k USD.

I don’t think you are right about the framework ASPs. There is 1 framework with an ASP of $230k (80-100 units) and 2 other framework agreements (min 130 units, 95+35, and those are for the entire system so they would be in the $400k to $450k range (I believe Sune gave that range on the Q1 or Q2 call for those framework agreements).

Sune has said in the past (I think it was Q417 call) that the upper range is $400k to $450k. I’m not sure why he said $400k today. Maybe for those 50 orders thats the biggest so far? Maybe they have discounted a bit for a large purchase?

In the presentation you saw it in was it part of the addressable market calc? Thats the only place I’ve seen the $450k referred to.

Yes exactly, I saw the 450k USD when they described the addressable market. From minutes 35 onwards in the replay he comments about ASP‘s.

The stock has revovered from recent lows in Q4. Meanwhile short interest has reached close to 4mn shares. The company will give an operational update on January 14th.

I read the transcript of yesterday’s update call with the management. According to the CEO China will only allow closed or hybrid scrubbers in the future which plays into Liqtechs hands.

They seem to beat their initial guidance and expect record Q1 and Q2 numbers. Cash was at 3,8 mn at year end and they will not need to raise any capital in the near future. Production capacity will be doubled by year end. They reported 110 orders for 2019 so far.

I’m still confused about their definition of what is part of which agreements and what the margin under the different agreements are. Maybe someone here can put bring some light on this.

Where did you find the transcript?

Bloomberg, it should be available on the company website anytime soon

There is a lively discussion on seekingalpha

https://seekingalpha.com/article/4233686-liqtech-attractive-bet-new-ship-fuel-regulation

thanks for the heads up!