What To Do With Gold Now?

Gold had a big move last week. We had a similar move in gold stocks. A number of the names I owned moved quite a bit. As is usually the case, I own a lot of gold stocks. I am left with the question: what do I do with them now?

On the weekend I went back to look at the big picture. After looking at gold supply and demand trends I am left drawing the conclusion that it is a mixed bag. It really comes down to this: the direction of gold will be determined by investment demand for gold, which is largely speculative.

What I do with that – I’m still not sure.

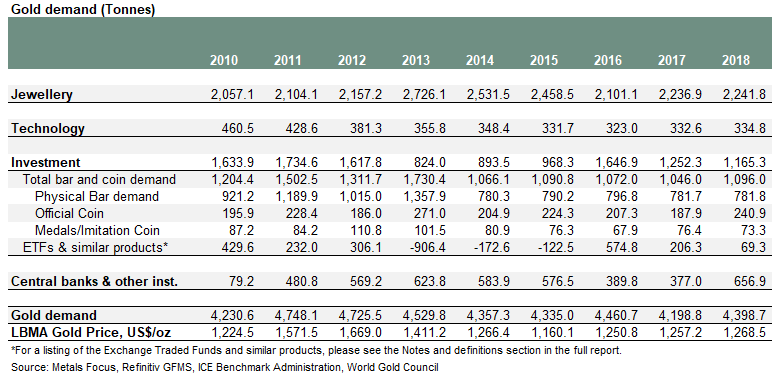

Here is the breakdown of gold demand from its major sources over the last 9 years.

The largest source of demand for gold is from jewelry demand. It makes up a little over 50% of overall demand at 2,241 tonnes last year.

Within that tonnage, China and India make up a large chunk – 743 tonnes and 598 tonnes respectively.

That means that over 30% of gold demand comes from consumers in China and India that are buying it as jewelry.

I would contend that these consumers are most influenced by the price of gold in their local currency.

I suspect that when Chinese or Indian consumers purchse a gold piece, they have in mind a fixed monetary-value they are will to spend, not a specific amount of gold.

So for these buyer what matters is the price of gold in their currency. Thus the US dollar price movements with respect to gold and with respect to their currency are the big drivers of how much volume they purchase.

The second consideration is going to be the economy. Clearly, in better years there will be more money to buy gold jewelry. In this regard, the trade wars and the slump of the Chinese stock market may not bode well for Chinese jewelry demand.

I think this is something that is often overlooked. It is why gold is not quite the counter-cyclical trade it is made out to be. Too much demand comes from jewelry, which is really the ultimate discretionary purchase, one that is correlated with the strength of the economy.

More generally, emerging markets are the big buyers of gold as jewelry, much more so than developed nations. The United States only bought 25 tonnes of gold in the quarter while Europe was only 13 tonnes. These developed regions have a fraction of the demand of China and India.

That makes me wonder about the long-term – will demand in India and China face headwinds as these countries continue to develop?

The US dollar performance is important. Something we already knew. But thinking through how local purchase volumes will rise and fall with the relative strength of the US dollar, it makes sense that gold prices fluctuate with this as well. It doesn’t necessarily have anything to do with the relative faith or lack of faith in the monetary system. It is likely just the anticipated fluctuations in gold jewelry demand.

Overall, I’m left feeling that jewelry demand is going to depend on how well the emerging market fairs economically, and how well their currencies fair compared to the US dollar. That tells me that jewelry demand is not likely going to be a tailwind.

I’m going to ignore technology demand, which has flattened in recent years and I don’t see as a big influence to the upside or downside, and move onto investment demand. Investment demand was 1,165 tonnes in 2018, which is down 7% year over year, up quite a bit from the trough years of 2014 to 2016, but down significantly from its peak.

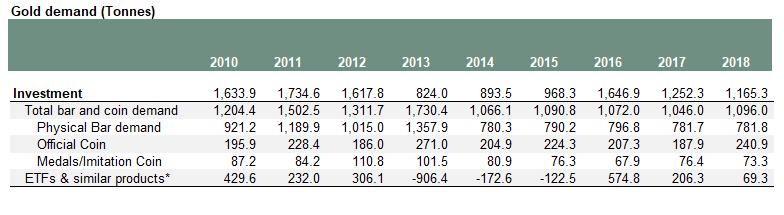

I’ve broken out investment demand with more granularity because I think its interesting to see how different physical demand and ETF demand behave.

Clearly all types of investment demand can fluctuate wildly. Just looking at it peak to trough, it moved 800 tonnes. That is nearly 20% of gold demand.

But ETF demand is particularly volatile. Between 2013 and 2016 it fluctuated almost 1,500 tonnes. That is just a massive amount.

It is a wonder to me that the price of gold doesn’t change more dramatically. Consider that oil can go down $20-$30 a barrel on a ~1-2 mmbbl/d change in supply/demand in a market of 100 mmbbl/d!

Investment demand is really what gold is all about right now. Its a wildcard for the reason that unlike other sources of demand, it is self-reinforcing. Generally, demand self-corrects with price. Investment demand doesn’t. It can actually increase with price, particularly if we get a speculative bubble.

Probably the most important point with this regard is simply that investment demand makes up 30% of overall demand. That is a lot. It means that gold is unique to other assets were so much of underlying demand is made on the basis of price expectations.

If you are betting on gold to go higher, you are betting that investment demand takes off. Considering what seems to be happening with monetary policy, that we are moving back towards something like quantitative easing, and that an active currency war doesn’t seem impossible, maybe this isn’t that farfetched?

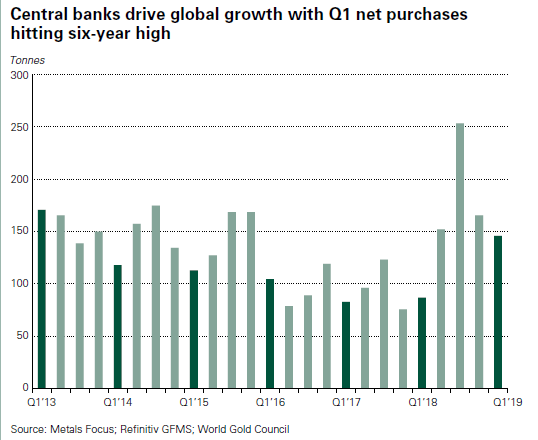

Related to this thesis would be that Central banks step up their purchases. Central banks purchased 145 tonnes in the first quarter. They account for roughly 15% of purchases.

Central bank purchases have been bouncing around without much of trend until recently. But maybe, if you squint enough, you can see that purchases have ticked up over the last year and a half.

Central bank purchases have been bouncing around without much of trend until recently. But maybe, if you squint enough, you can see that purchases have ticked up over the last year and a half.

It makes sense. A consequence of Trumps trade war should be that Central banks look to diversify currency holdings outside of US dollars. At least at the margin. That should add incrementally to gold demand.

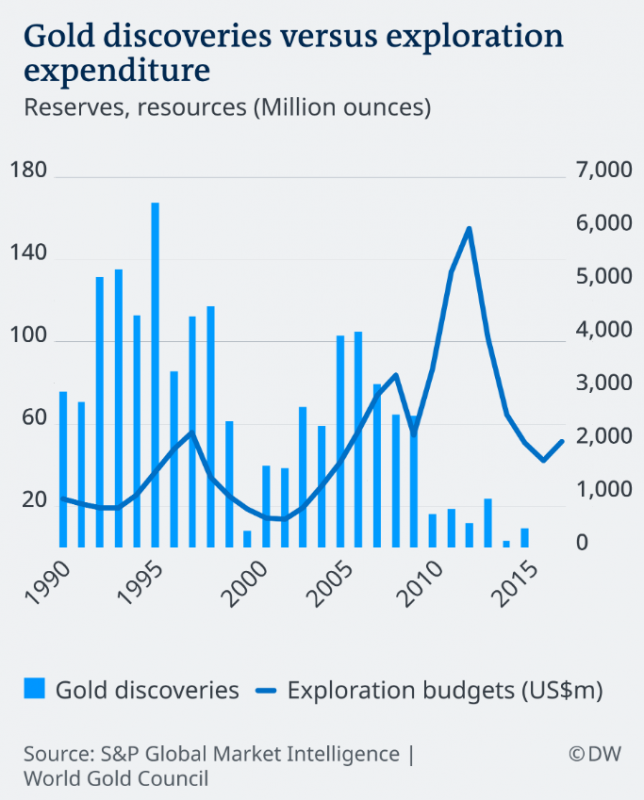

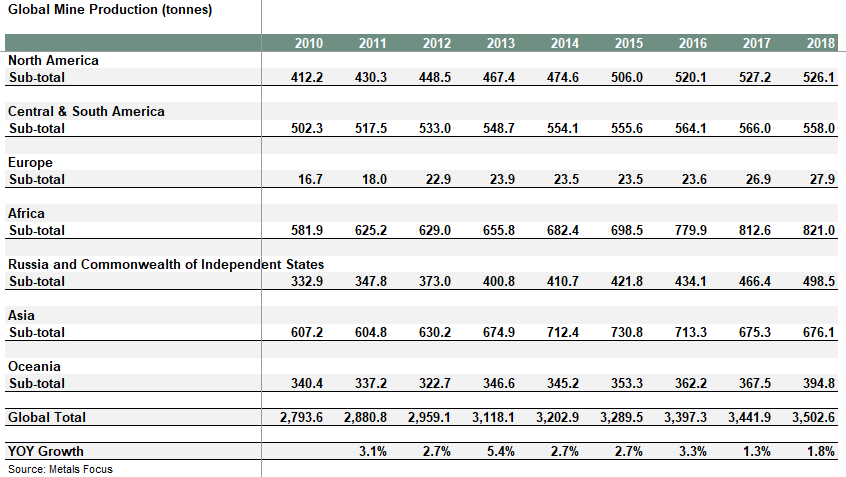

So that’s it for demand. On the supply side, I read lots of talk about peak gold. But to be honest, I don’t see it in the numbers yet.

There is a good basis for peak gold as an idea. Gold discoveries have seen a significant slide over the last few years.

The natural consequence is that we should see a drop in gold supply. There are analysts forecasting this to begin this year.

The problem is I don’t see it yet. Here is a closer look at gold production over the past 5 years. Gold production may be slowing, but its to early to say that its definitively rolling over.

In the first quarter of this year, gold production was up about 1%.

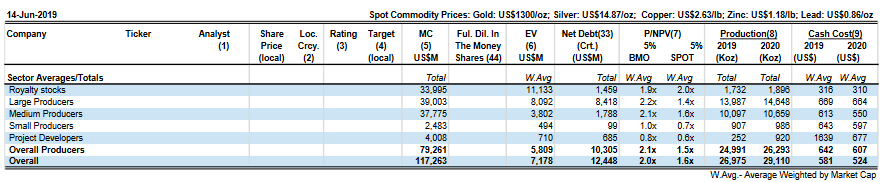

The last piece of the equation is the gold stocks themselves. Where are they in comparison to the price of gold?

It looks to me like there is a big variation between the larger cap stocks and the smaller ones. Take the following table from BMO, which is looking at that net present value (NPV) of large, medium, small producers and developers at $1,300/oz gold.

Small miners are trading at half the multiple of the larger ones.

I can pick out small miners I own that are even less than that. Argonaut Gold is at about 0.5x NPV. Superior Gold is at 0.3x NPV. Even Wesdome, which would be considered the darling of the junior gold stocks, is only at 1.1x NPV. I haven’t done the NPV math on Gran Colombia, Roxgold, or my most recent purchase, Fiore Gold, but I am pretty sure these names are all well below the average.

A last consideration is that Australian traded producers get a premium to those listed in Canada. BMO did a piece on this recently. They pointed out that the average Australian name trades at 10x cash flow at $1,300 gold, whereas the average Canadian name trades at only 6x cash flow. Again, the junior companies that I am invested in are even cheaper.

This combination, both relative value compared to larger producers and relative value compared to their Australian counterparts, should set the table for trans-ocean M&A. We already saw the first arrow across the bough with the acquisition of a name I owned, Atlantic Gold. Even as I have reservations about what drives the price of gold higher, and how sustainable that is, I’m inclined to hold on for now.