Week 419: Picking my spots

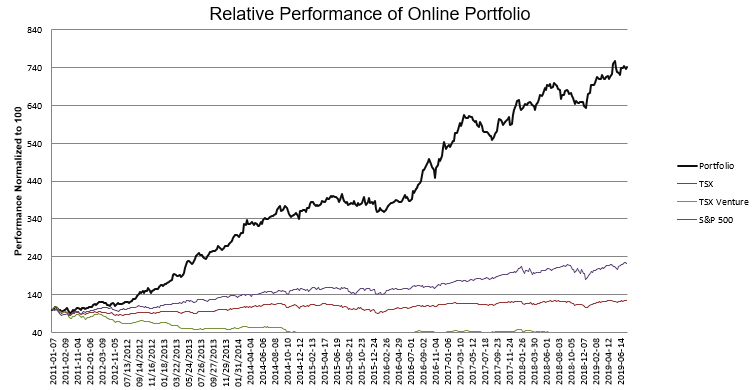

Portfolio Performance

Thoughts and Review

While the prior few months were characterized by performance that was better than it should have been because of the fall in the Canadian dollar, the last month and a half has seen the opposite. My portfolio has done reasonably well, particularly the gold stocks, but I am about flat because of Canadian dollar strength.

Be that as it may, I suppose you could argue that gold stocks would not be performing so well if the Canadian dollar weren’t strong, as the two both move in tandem with the US dollar and that either way I would be standing still. So I might be better to think of it as a hedge than a missed opportunity.

The rest of my portfolio, the non-gold side, is quite dull. I expect that to continue until we get a correction. I have a high level of cash in my account. That cash level is even higher after taking into account the sizable hedges I have in place via a Russell index short and an S&P 500 short.

With flat or down being my tentative conviction, I expect to continue to under-perform the market if it moves higher unless one of the small, strategic positions comes through as a big win.

There are a few signs that maybe I am wrong to be so hedged. The leading indicators have stopped falling, though they are still kind of flat-lining. The Baltic dry freight index has experienced a big bump, though that may just be due to iron ore exports from Brazil coming back. It is tough for me to make a call here, and tough for me to be terribly long when so many stocks seem to trade at valuations that I can’t make sense of.

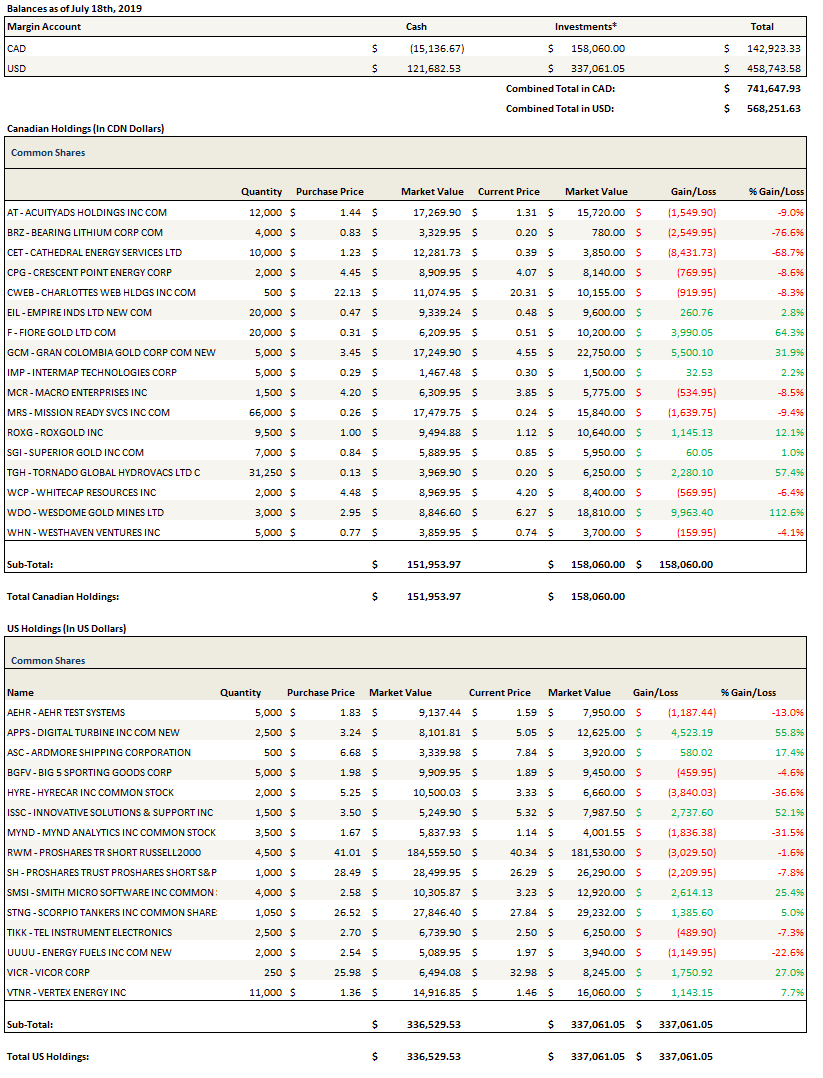

The easiest thing for me to own have been gold stocks. I don’t feel like they have recovered to reflect the current move in the price of gold. Many of the juniors I am in still look very cheap on $1,300 gold. I added a couple of gold names in the last few weeks: Superior Gold, Westhaven Ventures and Argonaut Gold (I seem to have forgotten to add Argonaut to the practive portfolio though).

I did sell a little Gran Colombia Gold and Fiore Gold this week just to get my overall exposure down. The one thing that worries me with gold (in the short run at least) is the Fed. Gold has a terrible tendency to be smacked on Fed days, and we have one of those coming up. Is gold assuming a 50 bps cut or a 25 bps cut? What Fed speak is gold pricing in? Does any of it matter and will gold simply be sold by shorts because it can? All questions that lead me to not want too much gold heading into next week.

I sold out of most of my IMO 2020 trade for the time being (I sold some STNG this week so that isn’t reflected in the portfolio update data). I expect to re-enter the trade. A couple of things led to my departure.

Regarding the refiners, I just feel they are so volatile, and as I said when I wrote about them, there are a lot of elements in addition to IMO rule changes that will lead to spreads. PBF Energy and Marathon both had nice pops after I bought them (after the obligatory post-purchase slide of course) and I thought I would get another opportunity at some point.

As for the product tankers, I was surprised to see that spot MR and LR tanker rates had fallen below $10,000/day. This simply didn’t make sense to me. These rates held up through the height of refinery maintenance season and I just don’t understand why they are as weak as they are now, with most refineries coming back online. I don’t profess any knowledge here other than simply “not getting it”, so I decided to exit these stocks until I understand what is going on.

With all that in mind I kept all of my Vertex Energy. This is probably my highest conviction name, as they seem so perfectly situated to take advantage of what has to a surplus of high sulphur fuel oil with nowhere to go.

The only other real change to my portfolio is that I added to HyreCar when the company was offering stock. I don’t know why they are offering stock. There are folks that say they are in discussions with large OEMs that want to see more cash on the balance sheet and that may be the case. It would align with their comments last quarter. But it seems to me that doing a raise here, especially one without a warrant overhang or any other gotchas, makes this a reasonable place to take a position.

Finally I’m starting to add a couple of oil stocks. I see the start of a change in narrative. The neverending shale growth narrative appears to be wobbling. If it topples, it would be good for Canadian energy stocks.

Portfolio Composition

Click here for the last seven weeks of trades.

{kind=link}

Where do you stand on $APPS? I sold recently after doubling my investment, but I’m still unsure if that was the right move.

I’m still holding it. Its a tough one. I really like it still but its one of these stocks that looks expensive to me. I think what keeps me in it is that these “expensive” stocks are the ones that seem to keep going up. But I would say they have a lot of things going for them that should* let them keep growing. They have the expansion from samsung, this new mobile hub product, and then just the single tap and notifications growth. So my hope is they pick up growth and beat some of the estimates but I can’t say i’m completely confident that will happen. I wish i had more insights.

I feel the same way. I wouldn’t buy it at this price which is why I’m selling. That was a good article you wrote on it originally though, so I thank you.

Hey Lane,

Just wanted to hear your thoughts, if any, on the Vertex Energy financing. I wasn’t expecting them to give up such a large chunk of equity in the Heartland refinery (unless they exercise their option to buy back in the future). Tough to get a read on what kind of potential value this adds, as finding group iii base oil margins data is a challenge..

Thanks,

Jack

On vacation though so I’ll have to dig in more. But the heartland refinery isn’t very big, I think its 20 million gallons, so you give away a bunch of that for $14.5mm that they can repay a lot of the debt that comes due early next year. I think the debt due is around $21mm if I remember right so the $14.5mm plus the $2.25mm in shares gets them pretty close to covering that. The revolver is $6mm or so of that so maybe they can refinance that piece. So they remove the refinancing risk, lose some of Heartland but they can make up for the lost production with the development of Myrtle, which was sitting idly. Myrtle is supposed to be a 50mm gallon facility so it would more than make up for the Heartland loss. The one piece I don’t know is how much of the capital required to bring Myrtle online will the $3mm that Tensile puts in the Myrtle SPV cover? The other piece is that they also want to bring TCEP on, so they just have too many projects for the amount of cash available, so doing something like this makes sense.

Do you have any thoughts?

It looks much better after finding an article that says they paid $16.5 million in 2014 (when refiners were trading much higher than they are now). Not sure what kind of money they have put into it over the past 5 years, but that put it in perspective for me. I agree that bringing idled facilities online can only be seen as a positive, as Tensile must agree that there is money to be made at Myrtle. Interesting to see HSFO cost actually rising at the moment….definitely caught off guard by that and the way that product tanker rates have softened. I am playing Vertex, PBF, STNG, and DSSI into IMO 2020, and riding the tanker dip out at the moment. Nobody on the ASC or STNG calls is wavering on their outlook into 2020, but just pushing expectations back a couple months. I will reevaluate the product tanker positions in the fall if rates stay where they are until then.