New Position in Evolent Health

I have a couple of resolutions for my new portfolio year:

- More concentration in the few names I really believe in

- More bottom-picking for lows

I think back to the years where I put in the best performance. The winners those years were primarily less-than-stellar stocks that had been out of favor.

MGIC and Radian. YRC Worldwide. Pacific Ethanol. Impac Mortgage. IDT. Yellow Media. Heck, even very recent winners like Digital Turbine and Smith-Micro were scrap heap pick-ups when I started looking at them.

These were all stocks I bottom-fished on. They were not picked from a list of 52-week highs. They all gave me some pain before working out. They all were big winners eventually.

Thus, a goal of mine this year is to spend more time looking for bombed out stocks and less time looking at 52-week highs.

I’ve taken a couple very small positions in struggling consumer products businesses in that regard (Big Five Sports and Dean Foods). I’ve also bottom fished a couple Canadian oil stocks (Crescent Point and Whitecap). But my largest endeavor by far into the world of beaten down tickers is Evolent Health. The chart is a poster-boy for such a move.

From what I can tell, the collapse of the stock can be attributed to three things:

- Revenue growth from the platform business has stalled

- Distressed conditions of a few customers have raised alarm bells

- Evolent has taken on an operational role and staked capital into its largest customer (Passport)

Let’s examine each.

The Platform Business

Evolent Health provides a platform that helps health plan providers manage the clinical and administration side of the business. The platform specifically is geared at providers looking to take advantage of Medicare and Medicaid value-based care programs.

Value-based care are a series of relatively new initiatives created by state and federal governments in an attempt to better align the interests of health care providers with outcomes.

What is driving the change is the recognition that government needs to be more effective in their health care spending because the funding dollars aren’t there.

There is a long-term funding shortfall in health care.

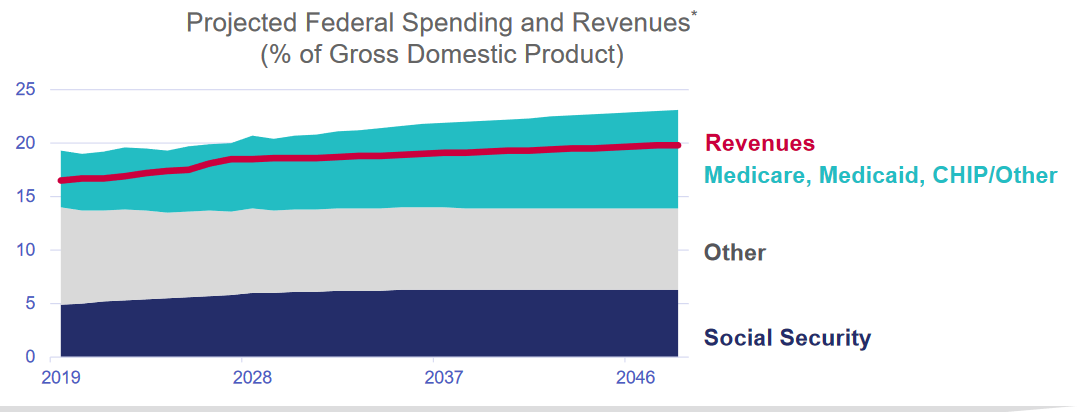

Evolent provides the following slide in their Investor day. It illustrates the relatively flat revenue available from the Federal government (from taxes) and the increasing costs of Medicaid, Medicare and other government health programs.

This disconnect has led government to look at different reimbursement models than just simply paying fees for services.

It is a priority. In fact, value-based health care is considered one of the three top priorities by the Trump administration’s HHS secretary Azar.

The problem is that value-based health solutions are complicated. They require that hospitals incorporate data analytics, automation and a level of administrative, clinical, and financial risk assessment that they are not equipped to handle.

Evolent provides the platform to bridge that gap.

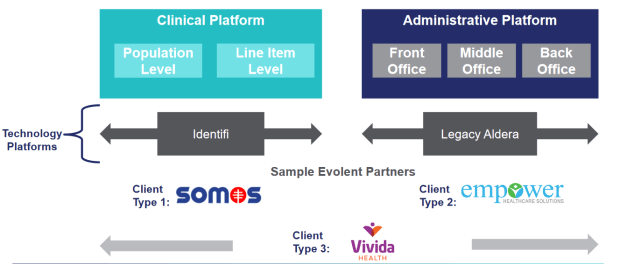

Where Evolent Sits

The Evolent platforms handle the clinical, administrative and financial side of the business They integrate all available data to assess risk and provide a course of action for each life covered by providers and payers.

There are really two connected platforms. The first, called Identifi, handles the clinical side , while the Aldera platform handles the administrative side. The platforms can be integrated and customers that use either or both.

The valuation proposition behind the platform is simple:

- Medicare and Medicaid programs are available that can allow providers to improve their compensation from these programs.

- To capture that margin providers need to be armed with better data and tools.

- Evolent can be the middle-man to provide the data and tools.

What adds value to providers?

With each client Evolent asks the following questions:

- how do we drive clinical value working with very engaged providers, leveraging all the tools that you need?

- how do you help to monetize that?

- how do we get paid for it?

One of the focuses of the Evolent platform is prevention. Engage the patient before they even get sick, engage the provider, and provide resources around the provider to help predict the outcomes before they happen. They call themselves “the best in the industry at determining who is going to get sick”.

Evolent has measured their performance against control groups and estimated that they kept their patients out of the hospital for 41,000 days in 2018.

When you think about the cost of a hospital stay, that is significant for a payer. They reduce total medical expenses by 24% per life covered.

Another value proposition is as a single touch connection between providers and payers – rather than each provider having to handle 5 different platforms from 5 different payers, they can use the Evolent platform and handle one that has portals that integrate with all the payers they deal with.

What happened to the business?

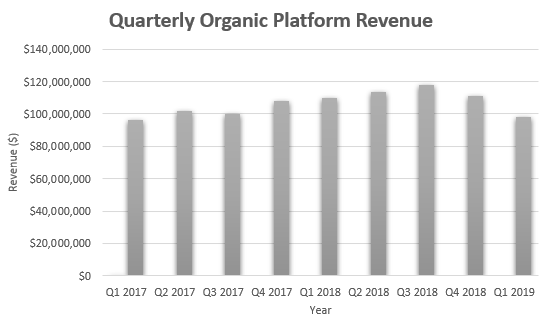

The first reason Evolent has sunk is because revenue from the platform business has stopped growing.

Looking at the financials is a little misleading because Evolent completed an acquisition in the fourth quarter of 2018 – New Century Health. The acquisition added about $50 million of quarterly revenue and makes things look a bit rosier than they actually are.

Without it, we see a decline in platform revenue the last couple of quarters.

The company outlined the reason for the decline on the fourth quarter call.

First of all, the wind down of our early provider-sponsored Medicare plans combined with McLaren’s decision to in-source MDWise’s health plan operations will drive lower same-store revenues in the first and second quarter.

The decline will likely continue into the second quarter. The provider-sponsored Medicare plans were high revenue per patient, which hurt margins as well.

The loss of the MDWise business is because they were acquired by McLaren, which now is integrating them into their own system. MDWise is significant, with 360,000 Medicaid patients.

Together MDWise and the provider-sponsored Medicare plan losses are about $55 million of annual revenue. A significant hit to a $450 million business.

Is this a read-through into Evolent’s performance going forward? Here is what William Blair thinks:

Making up for the revenue loss, Evolent has signed 3 significant new deals (with RCMG, Premera and Empower). These will begin to ramp up but not until the second half of 2019.

While we have one of the most robust pipelines in our history, our new expected deal start dates are more back weighted to the second half of this year. This is largely the result of CMS’s July start date for its Pathway to Success program, which impacted our Medicare line of business as well as New Century’s sales cycle relative to our October close date. The good news is we start the year with 2 closed deals in California and Arkansas, which we expect to fully ramp midyear and several late-stage deals, which are consummated would drive growth in the second half of 2019.

Concern #2: The Customers

The second concern is customer solvency. Evolent Health has a short list of customers. While they cover 3.1 million lives (after removing MDWise) they only have 30 or so partner organizations.

A few of these customers are experiencing a degree of financial duress. Most notably is Passport Health, which made up 17% of Evolent’s revenue in 2018 and is expected to make up 10% of revenue in 2019. Passport has been on the verge of insolvency this year.

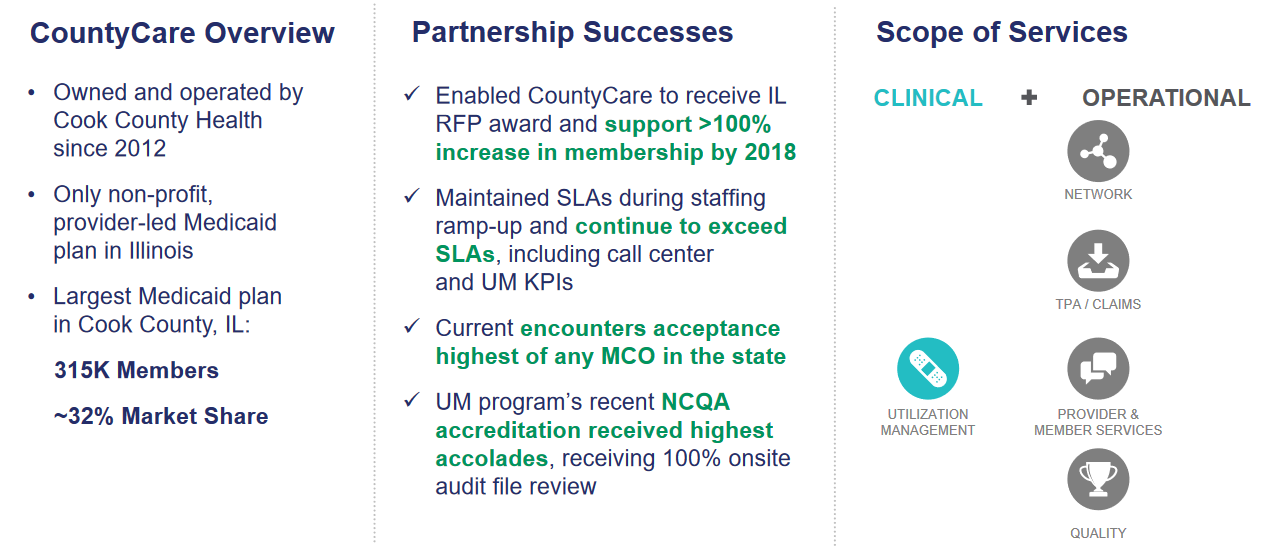

A second Evolent client that has been in the news (negatively) is Cook County’s CountyCare. They were highlighted as a partner in Evolent’s May investor day.

According to this article, CountyCare is far behind on payments and owes $700 million to providers.

Cook County’s Medicaid health insurance plan is so behind on paying vendors that there’s a shortage of pacemakers and anesthesia for surgeries – and some doctors even refuse to treat patients covered by the plan, according to a watchdog report released Friday.

CountyCare, however, refutes the claims.

The Passport Situation

Of the distressed customers, Passport is the immediate worry and the source of the third investor concern – Evolent’s ownership stake in Passport.

Passport is the second largest provider of Medicaid plans in the state of Kentucky. They have 315,000 lives under their coverage. They are a non-profit.

Passport has run into trouble because of rate changes in Kentucky and inefficient operations.

There was a retroactive rate reduction last year that squeezed revenue.

Second, as a non-profit Passport is not as efficiently run as they could be. Evolent described Passport as having “less urgency” than a for-profit company may have.

This combination of factors put Passport on the brink of insolvency this year. They began looking for a partner that could help them both run the plan and be a capital partner.

Making the urgency of situation more immediate, Passport is up for renewal on their Medicaid license in Kentucky.

While the new Kentucky Medicaid contract, which runs through 2025, won’t take effect until next summer, bids are due on July 5.

In all likelihood Evolent was not keen to be a part owner in a health plan. They implied that it was, at the very least, a process on their investor day call.

But Passport represents a lot of revenue to Evolent – over $100 million. That revenue has a significant contribution margin.

Evolent probably felt they couldn’t afford not to take the risk. This comes at a time where Evolent is already facing revenue losses from MDWise and some Medicare Advantage accounts.

The Market Reaction

The market didn’t like the decision to take ownership in Passport. The stock fell 30% on the announcement.

A few reasons for the response. The market does not like that Evolent is getting into the plan operations business. It does not like that the business they are getting into is a money-losing plan. It probably doesn’t love that they are essentially providing financing to one of their customers.

The market is looking at this as risk – to the existing revenue stream that Passport represents and to the $70 million that Evolent sunk into Passport for the ownership stake.

Evolent is supposed to be a platform provider, collecting fees and maybe performance incentives from plan providers. Investors bought the stock to participate in that. Not to see them run a plan themselves!

All fair points. But when I dig into what they are doing with Passport, what seems to be missed is that there is an upside here.

The Upside

Passport is, rather obviously, a money-losing business right now. They have lost $164 million in the last three years, including $60 million last year.

It’s a health plan in need of a turn around. If Evolent really is what they say they are, they should be the ideal partner to create that turnaround. This is a showcase for the power of their platform.

Not to mention a potential windfall if the business turns.

Consider the following:

- Passport’s premium revenue from the 315,000 members is about $1.95 billion right now

- Evolent believes they can take Passport’s medical expenses down to 90-91%

- They also believe they can take Passport’s administrative expenses down to 8-9%

- Together they see operating margins stabilizing at 1-2%

- They also believe they can drive the base revenue of the services they provide to Passport (so essentially the platform services) by 50-75%

Let’s just entertain the crazy idea that Evolent can actually accomplish what it wants to do. In such a scenario Passport would deliver $20-$40 million of annual operating income.

If that happens, Evolent’s 70% stake in the health plan is worth a lot. Wellcare, which is albeit a large plan provider of Medicaid as well as Medicare plans, trades at 20x earnings. Humana trades at 16x earnings. UnitedHealth trades at 17x earnings. Molina Healthcare, which is the smallest of the group at $8.8 billion, trades at 13x earnings.

It’s easy to see how this could explode. If Evolent succeeds, let’s take the high end just for blue sky, is it absurd to think that Passport is worth 10x operating income or $400 million? That would put Evolent’s stake at $280 million, or nearly half the market capitalization right now.

On top of that there is the benefit to the base services business. Platform revenue increases by $50-$75 million as a result of increased integration with Passport.

The Risks

There is, of course, a lot that could go wrong.

In the short-run, there is a reasonable chance that the second quarter is bad. The stock may still have another leg down.

Looking longer-term, the Passport experience may fail miserably and Evolent may end up losing not only its $70 million investment but the $100 million of revenue they currently get from Passport.

Maybe even worse, Evolent’s focus on Passport distracts management team and deals elsewhere fall through.

The other risk here, and it’s a legitimate one, is that the platform business slowdown is not just a one-time hit caused by MDWise and a few other customers.

The cynical view is that the acquisition of True Health New Mexico, the acquisition of New Century and now the ownership stake in Passport are really just smoke and mirrors – intended to obscure the revenue decline of the platform.

I, of course, cannot rule that out.

What I can say is that if the negative assumptions don’t play out and the platform business returns to low-double digit growth (management did a soft-guide to “teens growth” at the analyst day in May), there is really no reason the stock should be in single digits. If they execute successfully on Passport, it could be much higher.

Evolent trades at under 1x EV/Sales. Margins aren’t as high as most platform plays at around 40% (this is something I have to admit I haven’t quite wrapped my head around why) so they shouldn’t get the sky-high multiples that you see with some. But under 1x has to be too low if the business isn’t on the verge of an implosion.

So that’s the opportunity. I think it’s miss-priced. I understand why its miss-priced. I also understand that how it could be fairly reflecting what is to come. But I think the risk is worth the reward. I’ve made Evolent a pretty big position but I will double down if it tanks on earnings, but my thesis is intact. I’m willing to take some risk here.

Reviewed the results and listened to the call and came away more bullish than before. Company was much more upbeat about growth – said 2020 should see mid-teens growth and there is upside to that with both Passport and with pipeline wins. Expect to be at $40mm to $50mm EBITDA run rate by Q419. Passport remains a risk but they’ve gone a long way to implementing the efficiencies they talked about. Said they have reduced operating expense 8% already, expect another 4% by end of Q319. So if those numbers are consistent with what they talked about previously, they are essentially at the opex and admin cost reductions already. Still the risk that Kentucky pulls the rug out but when I think about this I have to ask myself, how likely is it? Kentucky throws all these citizens, seniors, into turmoil of new health plan at a time when Passport is getting its act together? I don’t know, maybe there is an element I don’t understand but it seems like an unlikely path to me.

Whats the normal multiple on EBITDA here do you think?

very interesting. maybe a stupid question – if Passport is a nonprofit how can it be allowed to make 20mm EBIT? i’m sure they bought it for a reason but just wondering how that works..

When EVH buys passport they took over 100% ownership of assets and liabilities and then issued a 30% equity stake in that sub back to the original passport owners – so i believe by that process it is no longer a nonprofit