Sonoma Pharmaceuticals

These last few weeks have resulted in only a few changes to my portfolio. All of these changes are at the margin. I added back part of the tanker position (Ardmore Shipping) and the refiner position (Marathon Petroleum and PBF Energy). I subtracted and then added back some oil stocks as I waffle in my view on whether we are headed into a recession or not. I added back some Overstock. I reduced positions in the gold miners, mainly because its been a good run. I sold my position in BRF SA as I struggle to understand whether African Swine Flu is a big deal or not. Nothing major.

I haven’t been adding many new positions. I mentioned Evolent and Moneygram in previous posts. One other that I added just last Friday was Sonoma Pharmaceuticals.

Those of you that have followed this blog for a while may remember an ill-fated post I wrote last April about Sonoma.

The idea back then was that Sonoma was a relatively cheap ($24 million market capitalization) pharmaceutical company that had a growth business (a U.S dermatological segment comprised of 6 products) that was obscured by other slow growing businesses and divestitures. I argued that the market was not correctly pricing the dermatology business.

It seemed like a reasonable thesis at the time, but it didn’t work out very well. In fact, only a month later the company reported their fiscal year end results and the story unwound completely.

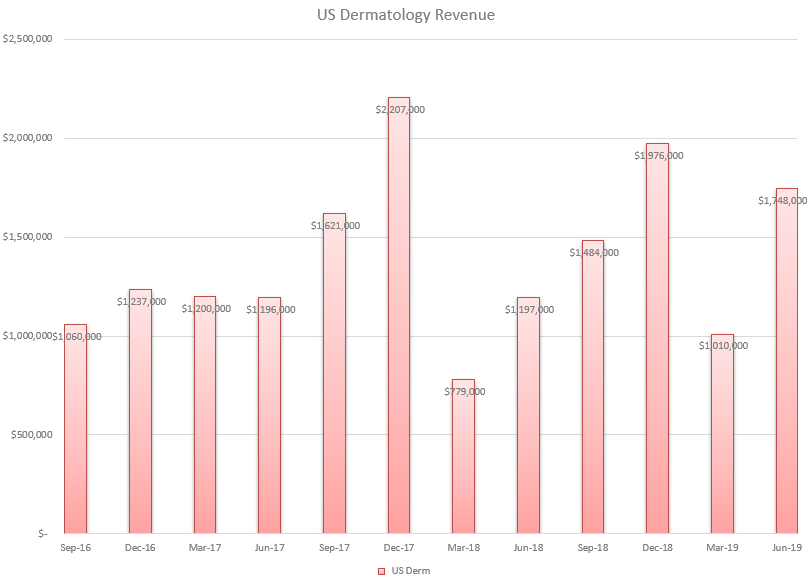

In the first quarter of 208 growth in the US dermatology segment stopped abruptly. Revenue for the March 2018 quarter was $780,000, down from $1.2 million the previous year.

Needless to say, I put my head down, took my loss (which if I remember right was substantial) and went home.

It was lucky I did. The stock continued to fall through to the end of the year. I got into the stock at a split-adjusted price of about $36. I exited in the low $20’s.

It traded down to $10 in November when the company did an equity offering (at $9 with half warrants at the same price). It fell further to the $7’s as Sonoma replaced their CEO and CFO in mid-December. It is bottoming (maybe?) now at a little over $5.

The new CEO is Bubba Sandford. Sandford’s previous gig was with Command Center (CCNI), which is a publicly traded temporary staffing company.

His track record at CCNI is mixed. The stock price treaded water for a number of years but it is worth noting that shortly after Sandford came onboard in 2013 there was a noticeable rise in the share price from $2.50 to $8+. It seems like he did the job cutting costs but was never able to follow through with growth. Things went south for a while in 2016 after a restatement of results. There are some vocally displeased shareholders on this call in particular.

Sandford describes his role with Command Center as a turnaround on Linkedin:

New CEO or not, this year the share price of Sonoma has continued to fall, albeit at a somewhat slower pace. It was trading at pretty much the low of $5.50 when I bought stock on Friday. It popped after that, but I have no idea why. It wasn’t me buying it up.

So what is the story now?

I’m almost embarrassed to say. It’s basically the same as it was. But with a better breakeven and bigger discount.

In March Sandford announced that there would be cost-cutting measures to bring the business closer to profitability. In the press release Sandford said:

“Our chief goal is to allocate our resources in a manner that maximizes shareholder value. While we are pleased with the direction of the 3rd quarterly results, we are not yet finished with the process of accessing ways to grow revenues, reduce expenses, and improve gross margins. This process takes time and can be painful, and we recognize that personnel reductions are difficult for our employees, their families and the community. We value the dedicated team at Sonoma for working hard towards this goal.”

This was followed shortly after with the sale of their animal health business in May for $2.7 million. The sale gives them a bit more cash which means a bit more runway which is something they need because they are not breakeven yet.

Their fiscal fourth quarter, which is for the quarter ended June 30th, was announced this week and it looked to me like the company made progress. Operating expense for the quarter was $4.1 million. This is the lowest operating expense I’ve seen for the company since I started watching them back in 2016. The reduction in SG&A for the quarter was $1.2 million year over year.

Equally positive was that U.S dermatology sales were up 46% year over year.

In fact, apart from that disastrous first quarter of 2018, dermatology sales in the US have been doing pretty well.

But the second quarter was a blow-out. If it continues the company may be closer to cash flow breakeven than you think. It’s a seasonal business with sales typically being highest in the fourth quarter which will be a wind at their back for the rest of the year.

But the second quarter was a blow-out. If it continues the company may be closer to cash flow breakeven than you think. It’s a seasonal business with sales typically being highest in the fourth quarter which will be a wind at their back for the rest of the year.

With better sales and improved costs, I calculate that operating cash flow before working capital changes was still a drain of $1.4 million. While this isn’t great, it is much improved over the $2.5 to $3 million burn they were doing a year ago.

While operations appear to be moving in the right direction, what really got me interested here is the price tag. At $5.50 and with a little over 1.3 million shares outstanding the market cap is only $7 million. There are another 446,000 warrants and options, but these are priced significantly higher at $10 and above, so I’m not considering them.

While I realize the cash on hand is fleeting given the cash burn, this means the enterprise is trading at under $3 million as of the end of June.

That seems pretty cheap given what is a legitimate product line that is demonstrating growing sales.

Of course, unless they have more cost-cuts up their sleeve or another big bump in revenue, they will have to raise cash one more time. An ill-priced predatory offering and all that potential value could be out the window.

On the other hand, a fair offering and another good quarter could represent a turn in the stock.

So there is unquestionably a lot of the risk here. We’ll see. Bubba Sandford seems to have them on the right track here. If the next quarter can bring another uptick in sales and/or further cost reductions, we may see the cash burn contract further. Or some other positive event may occur. Sandford is acting in what appears to be shareholder interests. Given the price and the recent trends, that is reason enough for me to take a small stake.

Always enjoy reading your blog. Lots of refreshing and under the radar ideas.

Have you read this blog post recently? I know u wrote about shippers before. I still find them interesting even with the mess that’s going on on trade.

http://adventuresincapitalism.com/2019/08/19/shipping-update/

Thanks I’ll check it out