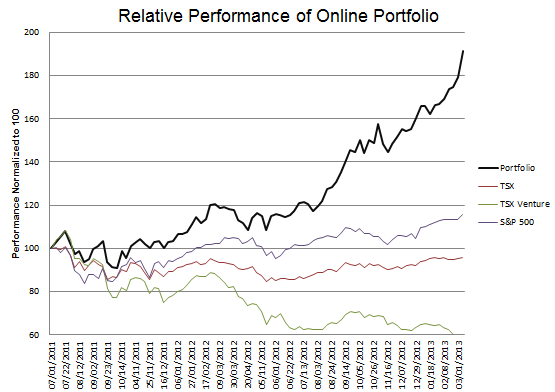

Every quarter I spend an evening or two going through the reports of the 15 or so gold stocks that I follow and updating a spreadsheet that I use to track their progress and compare them against each other.

I do not use the spreadsheet in the way a strict value investor might. I do not search out and buy the cheapest gold stock of the bunch on a cash flow metric or per ounce metric. I do look for value, but I also look for growth. The stock market tends to treat gold producers in much the same way they treat any other business: stocks with superior growth potential get bid up to higher valuations. On the other side of the coin, you can sit on what appears to be an undervalued producer for a long time if that producer has a poor pipeline of projects or has no prospects to produce near term incremental ounces.

I did exactly that recently with Aurizon Mines. I was attracted to the value, it was cheap compared to its peers, it had a lot of cash on its balance sheet and no debt, and they have a well run and profitable operation at Casa Berardi. Yet Aurizon does not have a strong growth pipelne. Its closest to completion project is an open pit prospect called Joanna which, while it could one day produce a lot of gold, has been stuck in the feasibility stage for more than a few years and has the worry of requiring a large capital outlay out front. When you add that to a number of fairly early stage exploration projects the result is a company without the near term potential to grow ounces significantly. I sat on Aurizon for almost 6 months based on its value story and the stock went nowhere.

At the other end of the spectrum is a company like Argonaut Gold. I owned Argonaut Gold for a while last fall but sold out way too soon. I sold because I saw the stock was priced dearly compared to many of its peers. However I failed to adequately account for the growth opportunities. It was a silly oversight; I had originally bought the stock because of the low capital cost heap leach projects that they could bring to market quickly. Somehow though I forgot about this, got caught up in the valuation and that led me to sell too early. The stock has since doubled to $10 before pulling back in the recent carnage that has brought all gold stocks to their knees.

When I was looking for gold producing companies a couple of weeks ago I was on the lookout for the next Argonaut Gold. Unfortunately I have not been able to find them (if you have some ideas, please drop me a note). In my opinion the closest comparison to Argonaut in terms of near term low capital cost growth potential is Atna Resources. Atna has a legitimate chance of increasing their gold production from 40,000 to over 150,000 ounces in the next couple of years. What makes Atna an imperfect comparison is that most of its projects hover around the cash cost level of $900 per oz, which is on the high side of the cash cost scale, whereas Argonaut has been able to achieve the double whammy of low cash cost low capital cost growth.

A second producer that I have bought (back) recently is OceanaGold. I have had good luck with buying OceanaGold when the market hates them and selling when the market starts to show some love. This time around I may hold on for a bit longer. OceanaGold has typically been one of the cheapest gold stocks on cash flow metrics. This is because, in part, they have struggled with costs and production at their existing mines. However, their soon to be producing mine in the Philippines (Didipio) will bring about some growth to the company, and perhaps more importantly, it will reduce the corporate cash flow numbers substantially.

One thing that got me interested in OceanaGold again was my research of Agnico-Eagle (which by the way is the third producer I own right now). While Agnico-Eagle has had some difficulties with the closure of their GOldex mine, they remain one of the best growth stories in the industry and I believe the market will come around to forgetting about Goldex and recognizing this once again. Agnico-Eagle owns 5 operating mines. Of those five, one mine, Meadowbank, produces about 1/3 of the production. At the corporate level, Agnico-Eagle has reasonably low cash costs. They were $594 per oz in the first quarter. However Meadowbank, the largest mine, has cash costs over $1000 per oz. On its own its a marginal mine that produces a large number of ounces. Together with the other low cost assets that Agnico has, it receives a much higher valuation than it would on its own.

I liken this situation to the one at OceanaGold. At OceanaGold, the corporate level cash costs should come down fairly substantially with the introduction of gold production from Didipio. Didipio will produce a lot of copper in addition to its gold, and this will make the cash costs of the project appear to be quite low. The cash costs of OceanaGold will not get down to the level of a company like Agnico-Eagle (the high cost mines at Oceana will continue to make up too much of the production) but I do not see it as unreasonable to think they will drop into the high $700 range. My bet on OceanaGold is that when production begins at Didipio, analysts will begin to revalue the company on the basis of a mid-cost producer rather than a high cost one, and that should provide for some upside in the stock.

I updated the spreadsheet below over the weekend. I did not update it during this week with stock prices for each stock tabled. The prices are as of Friday’s close. There has been so much movement in many of these gold names in the last couple days that the prices are already somewhat outdated.

My hope with gold and gold stocks is that this move is for real. What I think we need to have for this move to be real is action out of Europe that brings gold back into the system. I wrote this weekend about how, in general, the turmoil in Europe should cause weakness in paper currencies and lead to strength in gold. On Sunday Donald Coxe was interviewed on King World News and decribed a scenario whereby gold would be used along with a value added tax as colateral for euro-bonds on ther periphery. While I am a bit fuzzy on what the details of such a bond might be, I believe that conceptually this is the sort of event that has the potential to create a great rally. On the other hand my enthusiasm is tempered that if nothing is done in Europe, and if the Federal Reserve does indeed decide that QE is not working (I don’t think its nearly as clear as others do that the Fed will mindlessly embark on further quantitive easing. The Fed is, after all, a data centric institution, and if it appears that the benefits of QE are not what was anticipated, and I believe that has been the case, they may decide that a third installment is not beneficial).

Below is my spreadsheet comparison.