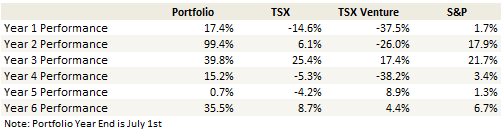

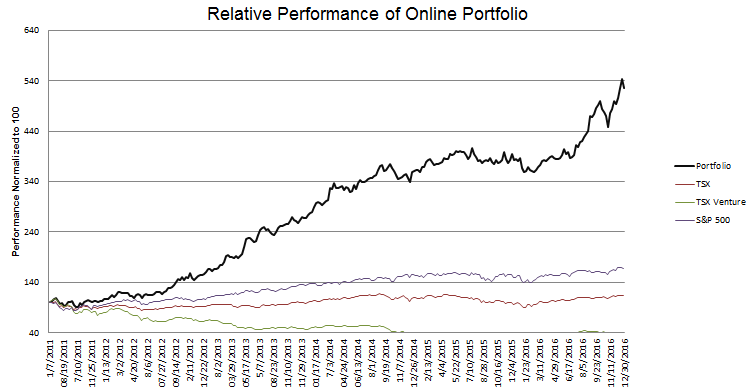

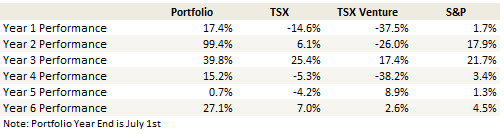

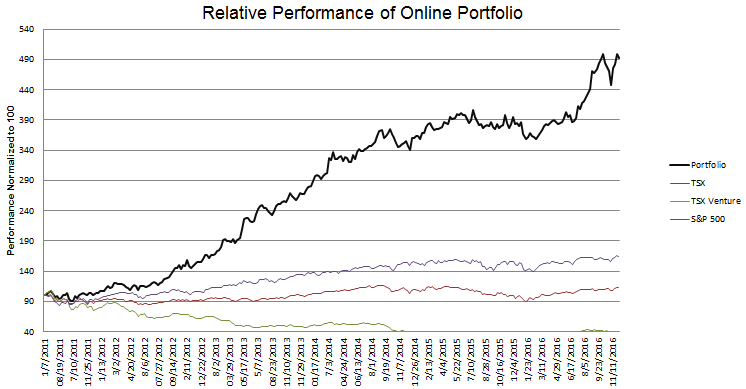

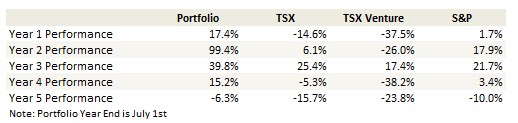

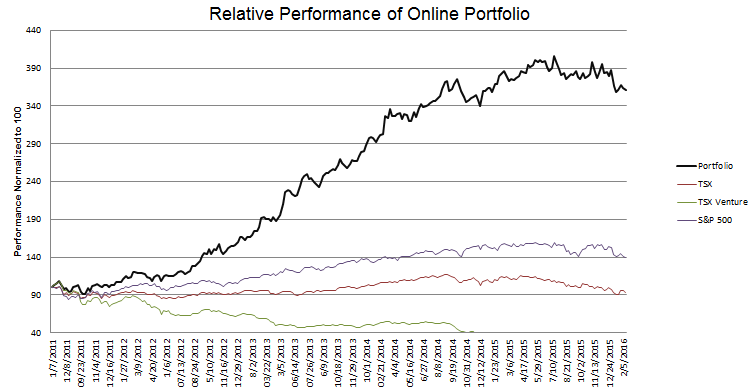

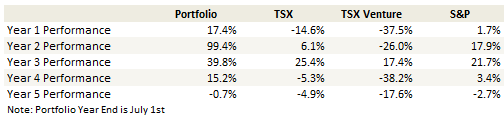

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Monthly Review and Thoughts

I was on vacation for three of the past four weeks, so my portfolio changes have beeen minimal. It was nice time away but the timing was unfortunate; the market swooned but bounced back before I got back. There were plenty of opportunities I missed out on.

As it were, the only two I was able to capitalize on were Mitel Networks and New Residential. In both cases I had old stink bids that got hit (a little over $6 for Mitel and $12.50 for New Residential). But even in these cases, the positions I ended up with were much smaller than I might have had I been actively watching the action. I’ll talk about Mitel a little later on.

I haven’t been tweeting a lot either, but I can’t attribute that entirely to being away. I find my mind hesitating on any conclusion. Its very difficult to tweet when each comment requires a couple of caveats a maybe and at least two possible scenarios. There are only 140 characters.

David Tepper was on CNBC a few weeks ago sharing his thoughts about the current state of the market (click here for one of the clips). Most of the summaries I’ve read focused on his comments about the S&P possibly going to 1,800.

What I took from the interview was uncertainty. The direction of money flows are criss-cross, whether the tide is still coming in or starting to go out is more uncertain then it has been in recent years. When quantitative easing was in full swing there was a clear easing of liquidity, now its much more muddled. And Tepper isn’t really sure where it will all settle out. It might be higher, but he seemed to suggest that he thought it was more likely to resolve itself lower.

If David Tepper isn’t sure of path of least resistance, I bet you can say the same for the market. And that to me says we are in for volatility. Which is what we are getting.

If we are going to be in market where directionality is wanting and volatility rules then the right approach is to not believe too much too fast. Sell the rallies and by the dips.

If I’ve done one thing right in the last four weeks it is that I have manifested these convictions in my trades. I sold out of a lot of positions as the market rose last week. I will be ready to buy them back if the market falls back far enough. Without QE, without China, and without sensible leadership from any of the market groups, I think we simply flounder around aimlessly, at worst with a downward bent.

A Position in Mitel

Mitel develops and installs unified telephone systems for businesses. They also provide white label back-end services and software for carriers so they can offer their own telephone products to business.

With Mitel’s legacy business, called the “premise” segment, they install a telephone platform on location, including the phones, connections and back-end. Upon sale of a telephone system Mitel generates revenue from upfront hardware and software sales, and a small amount of recurring revenue for maintenance and support.

The premise business has been shrinking as companies migrate toward a cloud solution. The cloud system Mitel provides is similar to premise in terms of functionality: the business gets a telephone platform that operates and connects its devices, provides unified voice mail, conferencing, all of the functionality you’d expect. But the system runs through the cloud, so the hardware component is mostly absent.

With the cloud product Mitel receives recurring revenue for each end-user that is hooked up. For their retail customers (those who purchase cloud services directly from Mitel) they receive around $45/month revenue per user. For their wholesale clients (carriers who resell the service as their own) they receive somewhat less, but at a much higher margin as they are only providing the software and support.

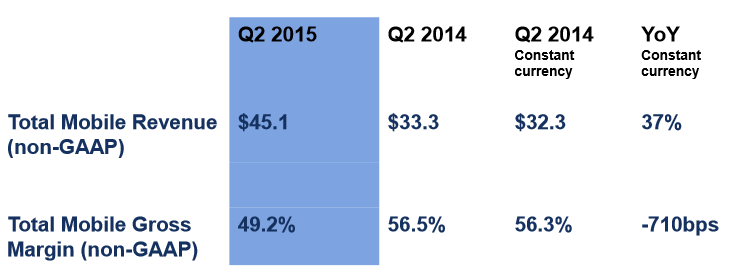

In April Mitel expanded into a third segment, mobile, with their purchase of Mavenir for $520 million. Mavenir offers a 4G LTE solution to telecom carriers. 4G LTE is the next evolution of telecom transmission.

4G LTE is slowly being adopted by carriers for its functionality and costs. With respect to functionality, 4G LTE allows for something called Rich Communication, which makes it easier to do things like video calling, group messaging or video streaming over mobile. As well 4G can deliver voice over the LTE connection rather than the legacy voice network which is expected to improve call quality.

For carriers the cost advantage is that once installed 4G LTE uses less bandwidth, which limits the requirements of additional spectrum that they have to buy.

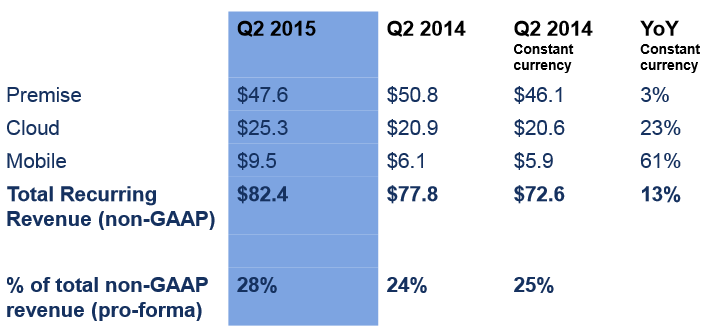

Mitel’s shift to cloud and mobile means that the overall business model is shifting towards one of recurring revenue through subscription/licenses. Below is a snapshot of recurring revenue growth for each of the segments.

The overall premise business is shrinking by about 5% to 8% per year as companies migrate to a cloud or hybrid cloud/premise solution. The cloud business has been growing at 20%. Mavenir grew at 30% in the second quarter.

Overall the company has been growing only nominally as the premise business, which makes up 75% of revenue, declines have overshadowed the smaller, growing cloud and mobile businesses. But this will change as the other two segments become larger.

The early indications are that the Mavenir acquisition is going well. Second quarter revenue for the mobile segment (which is essentially Mavenir), was $45 million.

On both the second quarter conference call and at subsequent conferences Mitel has noted an acceleration in Mavenir’s wins since they have been acquired. The concern of many carriers with respect to choosing the Mavenir solution was that it was a small company with limited resources and a small global footprint. Mitel’s acquisition has alleviated those concerns. At the time of the acquisition Mavenir had 17 footprint wins with carriers. Since April Mitel/Mavenir have won 10 more footprints including 1 major cable company in the United States.

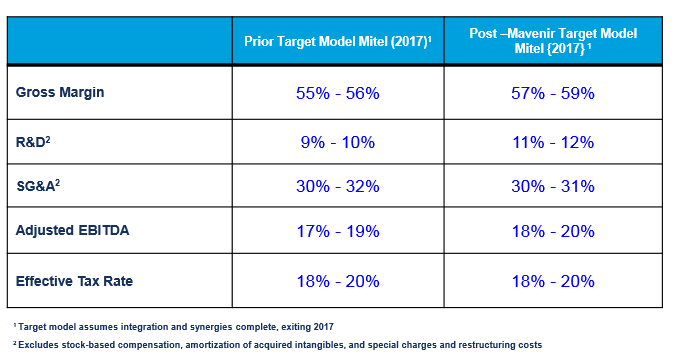

Mitel provides the following roadmap for earnings in 2017.

If I use the above roadmap and assume that Mitel can continue 20% growth in both the cloud and mobile business and that the premise business declines at 5%, I can see Mitel earning over a dollar in 2017.

I only wish I would have bought more of the stock when it was in the $6’s. The timing was unfortunate. As it is, I am contemplating adding to the position if it dips back into the $7’s.

There are a couple of decent Seeking Alpha articles on Mitel here and here.

Wading into the Biotech Controversy

I decided to jump in with the sharks and take a position in Concordia Healthcare. I also took a very small position in Valeant Pharmaceuticals.

Concordia has a similar business model to its much larger competitor Valeant. Its a roll-up strategy. In the last year they have acquired three pharmaceutical companies: Donnatal, Covis and AMCo. In the process they have increased their revenue from a little over $100 million in 2014 to over $1 billion in 2016. Below is a table of the companies acquisition pre-AMCo.

The stock has been hammered as Valeant has been singled out for pushing through price increases on many of its newly acquired drugs. The comparison is not unwarranted as Concordia has much the same strategy as Valeant, raising prices on newly acquired drugs where the market has been inelastic.

In both the cases I haven’t been able to get a solid handle on the extent of the price increases. Articles point to 20% plus increases in some drugs. Others go on to point out that these list price increases are not representative of what is actually paid, and that the actual price increases are more modest.

Valeant is also suffering from its own opacity. There is an excellent four part blog series that I would recommend reading before investing in either Concordia or Valeant. It is available here. The author illustrates numerous examples where Valeant had questionable disclosures and raises some questions about the performance of their acquisition post-integration. Most important though, it provides an overview of how to think about the valuation of both companies that I found extremely helpful.

Concordia is not quite as opaque as Valeant, though some of this is a function of its size. Until very recently the company only owned a few drugs and depended heavily on Donnatal for its revenue. So its not too hard to separate the contributing parts.

Unlike Valeant, I don’t see evidence that Concordia’s acquisitions have underperformed after being acquired. Donnatal, being Concordia’s largest acquisition prior to 2015, is illustrative. Donnatal was purchased in May of 2014. In 2013 Donnatal had revenue of about $50 million. In 2014 Donnatal had revenue of $64 million. In 2015 Donnatal is expected to bring in between $87-$92 million of revenue.

Of course some if not most of that revenue increase was due to price increases. How reasonable are future price increases on newly acquired drugs? Without a doubt the potential has diminished. But I think that as the front page headlines fade the reality will appear less dire than it does now. Keep in mind that the price increases are not comparable to the 5000% jack-up by Turing Pharmaceuticals an other aggressively managed hedge-fund like pharma providers. Meanwhile Concordia is down 50% in the last month; surely the more robust expectations have been priced out of the stock.

The bottom line is that both Valeant and Concordia have real negatives but they have also experienced really dramatic falls in valuation. Concordia was a $100 stock (Canadian) a few months ago. Valeant was over 30% higher.

I can’t take a big position in Valeant because I can’t really figure out how well its doing and I think the difficulty of performing their roll-up strategy increases with size. With Concordia performance is easier to evaluate and they are still small enough to be able to find interesting acquisitions and fly under the radar of the news. I think the question is more one of: are the negatives priced in? And I think there is a reasonable chance that is the case.

A Few Small Bets on Gold Stocks

Gold stocks have been so beaten up that it just had to turn at some point soon.

I also thought I saw was kind of a win-win situation with respect to the September rate hike decision. Either the Fed was going to hike rates, which would mean the event had finally passed and the stocks could stop pricing in its inevitability, or they wouldn’t, in which case the legitimate question would resurface as to whether we are really passed the QE-phase.

Additionally, there has been a shift quietly occurring in the gold sector. Many producers are getting their costs under control. This has been helped by improving currencies for non-US based producers, by lower energy costs and by lower construction costs. While the market seems to have a curious focus on valuing gold companies on the price of gold, which has been stagnant to down, the margin they make have been improving.

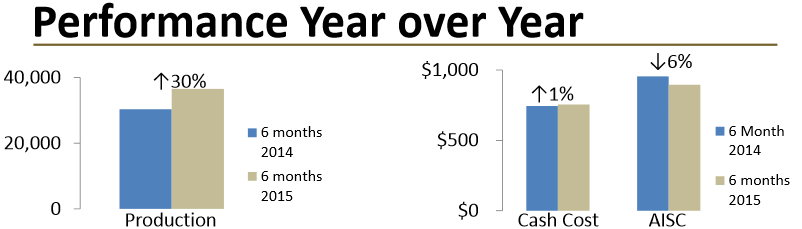

Let’s take Argonaut for example, which is one of the companies I took a position in. Argonaut has 155 million shares outstanding and trades at about $1.50, so the market capitalization is about $250 million. Debt is nil and the cash position is around $50 million. They have been improving their performance year over year.

Argonaut produced cash flow from operations before working capital changes of $28 million in the first half of 2015 (cash flow including working capital was $38 million, but because changes in inventory are such a big and fluctuating part of a gold mining operation I think they need to be ignored).

Sustaining capital expenditures and capitalized stripping at Argonaut’s operating mines (El Castillo and El Colorada) runs at about $5 million per quarter. So free cash (so before expansion and development capital) is around $35 million for the year.

Argonaut, and other gold producers like them, are not expensively priced at $1,100 gold. That means there is no expectation of higher gold prices priced into them. I think there is a reasonable chance we see higher gold prices as there is a reasonable chance that the economy continues to muddle. These stocks are multi-baggers if that happens.

Oil

I have had some strong opinions on oil over the past few months but I don’t have a strong opinion now. When oil was in the low $40’s I once again bet on a number of oil stocks including Crescent Point, Baytex and Jones Energy. I went through some consternation as Goldman Sachs came out with their $20 oil call and I listened to the twitter universe decry the inevitability of a collapse in the oil price. But in the end it all worked out, and I sold Baytex for a quick 50% gain, Crescent Point for a 40% gain, and Jones for a 20% gain.

With oil back in the $50’s I feel much more non-committal. For one, I think that at least some of this move is due to geo-political concerns, which isn’t a firm footing to base a stock purchase. For two, earnings season is upon us and there is at least some risk that the lack of drilling leads to downward revisions in production forecasts for companies like Baytex and Crescent Point. And for three, pigs really do get slaughtered, so when the market gives you a big gain in a couple of months I have found it more often than not prudent to take that gain and run.

I will be a bit sick to my stomach if Baytex runs quickly back up to $8, or Crescent Point to $25 but this doesn’t seem like the sort of market to be trying to squeeze out the last 10%.

What I sold (and one more I added)

As I already said I sold out of most of my oil stocks. I also used the run-up in tanker rates (they breached the $100K per day rate last week) to sell out of DHT Holdings in the mid-$8s and Ardmore Shipping at $13. I took some quick profits on my small position in Apigee, which ran back up from $7 to $10 on just as little news as what precipitated its move down from the same level. And I sold out of Alliance Healthcare after the rather bizarre acquisition of shares by a Chinese investment firm (another case where poorly timed holidays contributed to a larger loss than I might have otherwise taken).

I also had a bunch of stocks that I neglected to add to my on-line portfolio, mostly previously held names like Enernoc, Espial Group and Hovnanian. I took small positions in these stocks during the last dip but sold out them of quickly as they rose. My plan is to continue to do this sort of cycling, taking advantage of dips and selling the rips.

With that in mind, I did re-add one last position on the last downdraft that hasn’t recovered like I had hoped and that I think will at some point soon. Air Canada. The third quarter is mostly passed and there isn’t a lot of evidence that overcapacity from Air Canada and WestJet is going to hinder their performance. The stocks has barely budged from $11 while other airline stocks soar. I think it catches up some of this performance in the near term. (Note that I forgot to add this one to the online portfolio but will correct that when the market opens on Tuesday).

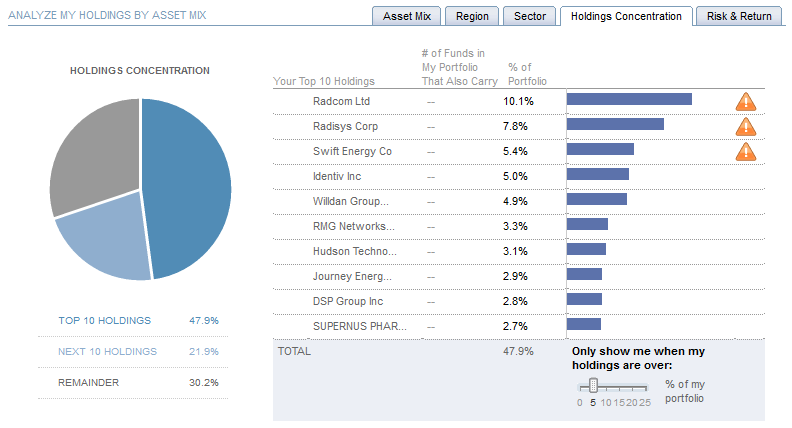

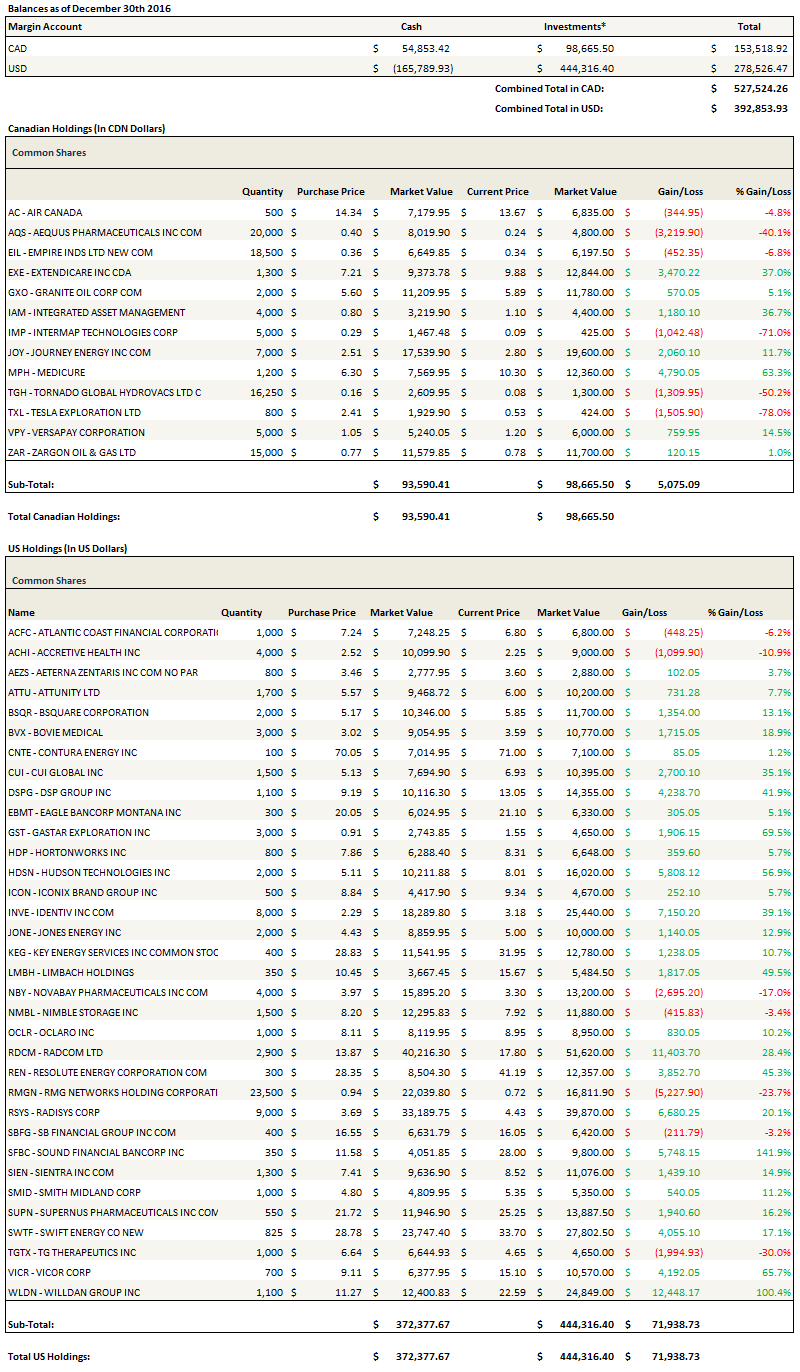

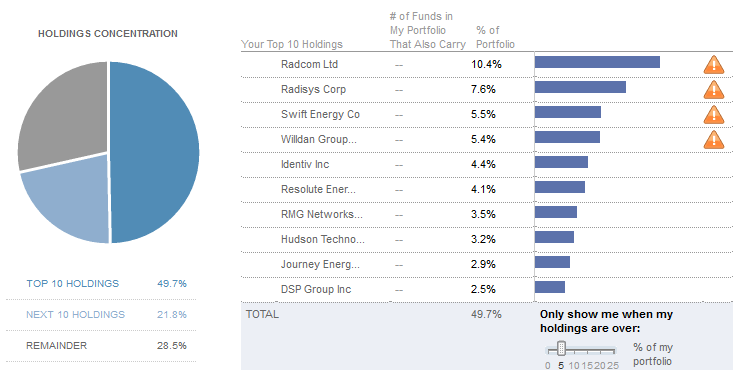

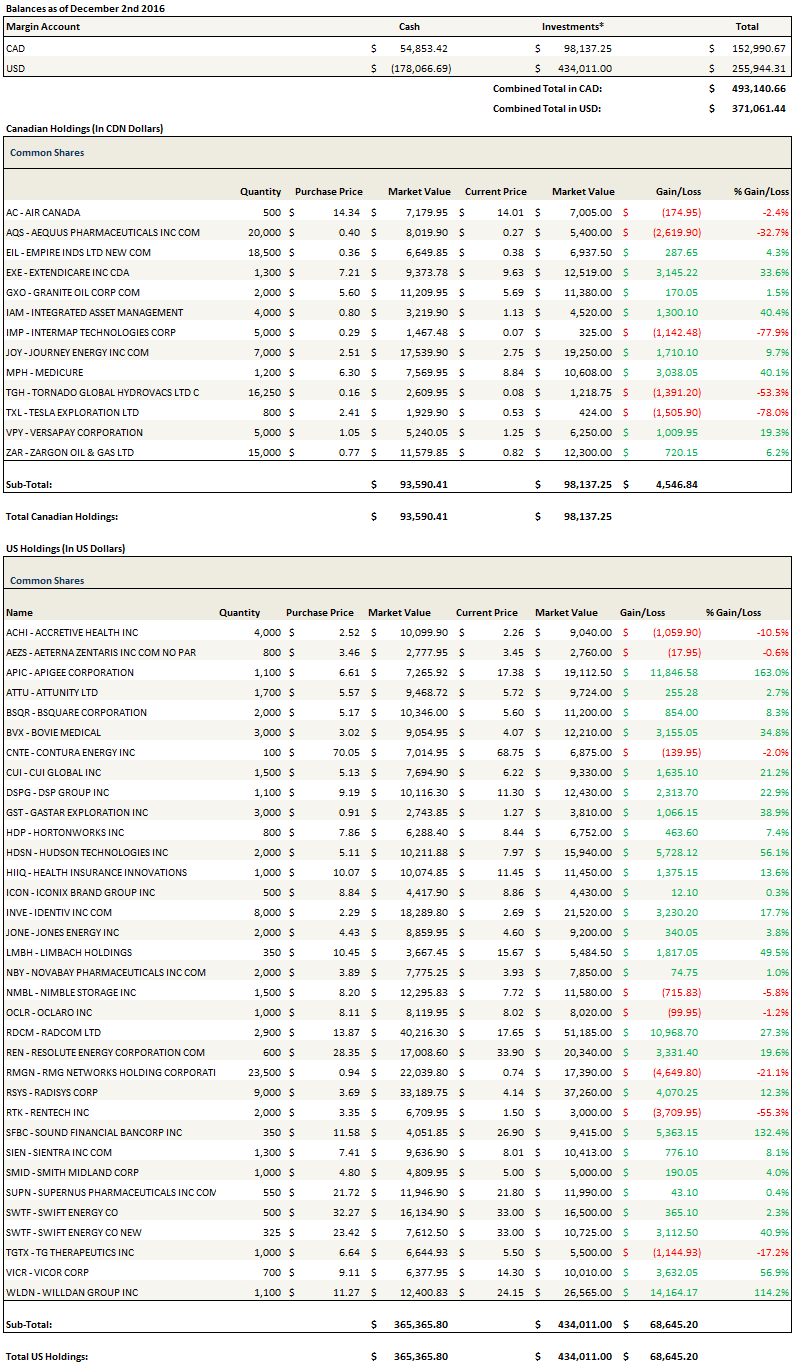

Portfolio Composition

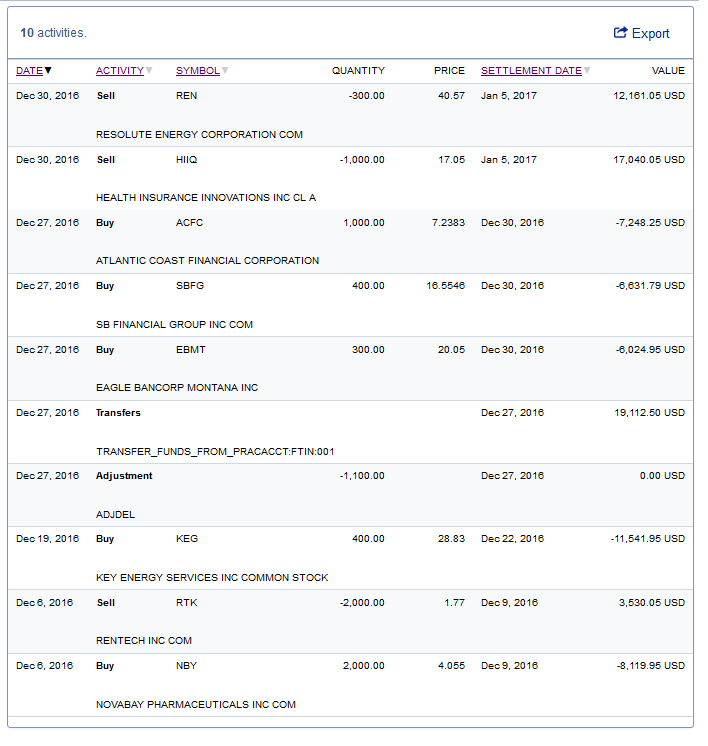

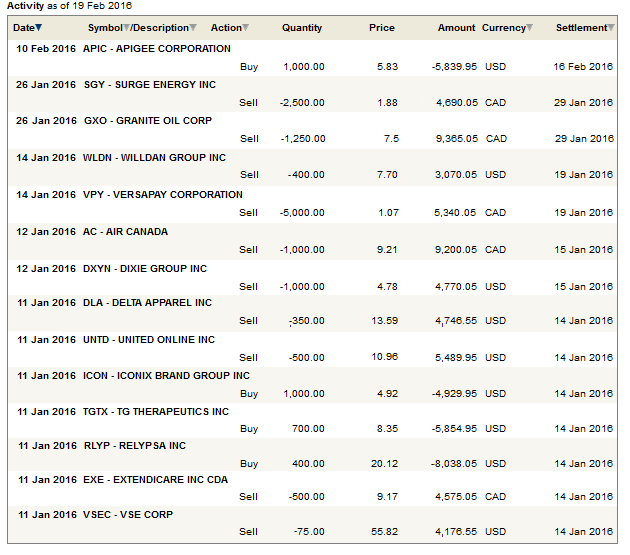

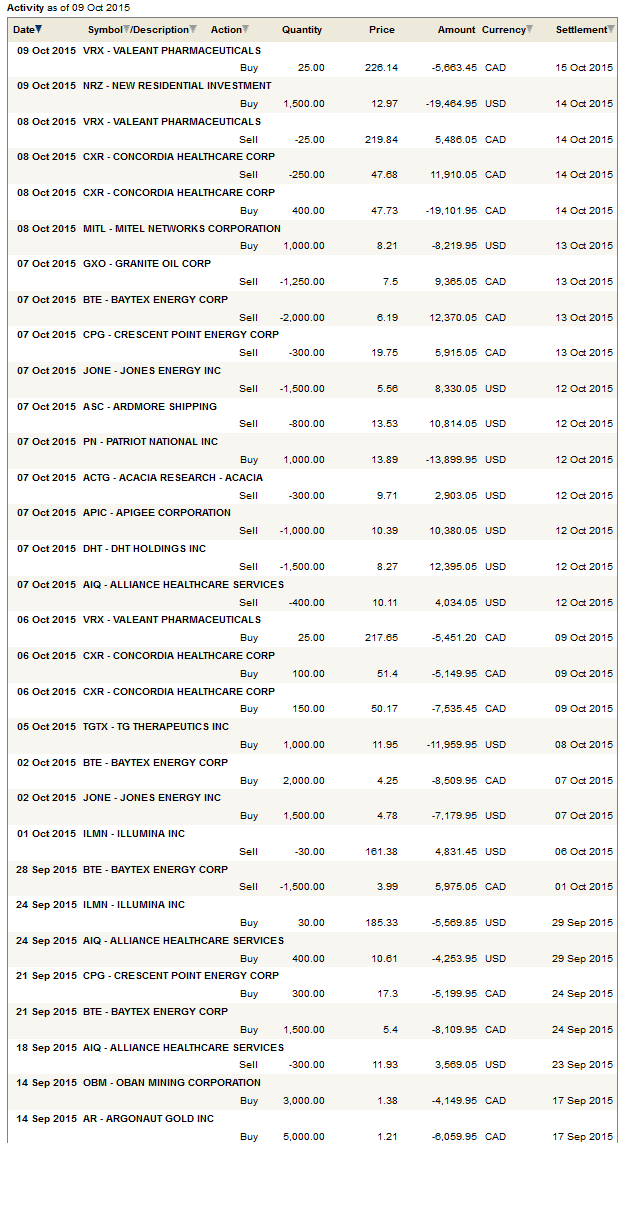

Click here for the last four weeks of trades.

{kind=link}

{kind=link}

{kind=link}

{kind=link}