I decided to make a number of changes to my portfolio today.

I wrote on the weekend that I hadn’t really changed much leading into the invasion of Ukraine, other than adding a bit more on the hedge side. I think that is because the uncertainty of the situation has taken a while to sink in for me.

So today I changed tact. I sold a lot of stocks. And I bought a few others that are tied to the commodities Russia exports.

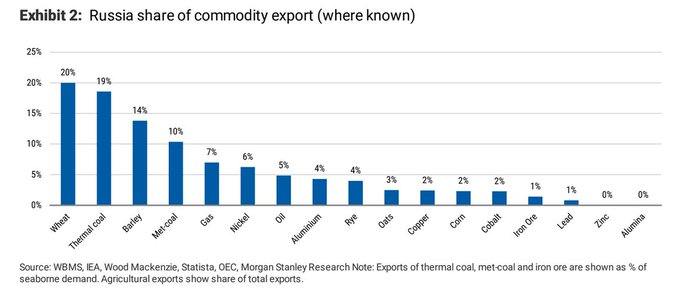

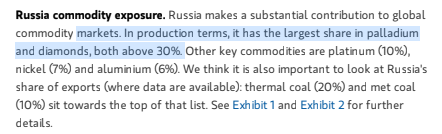

What sparked this was a search through the brokerage document database I have access to. I started searching for the word “Russia”. I quickly came across documents that showed just how large its influence on various commodities was.

I don’t think I realized just how big of a commodity exporter Russia is. And that really got me wondering how this is going to ripple through the world economy.

At the end of this post I’ve snipped a bunch of the tables and charts I found. Russia is just such a big player in the export of so many basic commodities. And then on top of that Ukraine is a large grain exporter and they actually export a fair bit of other commodities as well – steel for example.

I was already on edge about market exposure. So when the market almost got to even today, I said to myself that I would be crazy not to take this opportunity to make wholesale changes.

I sold a lot of my bank positions and a lot of my biotech positions. I now only own a little BCBP, a little BSVN, and a bit of a few biotechs trading well below cash. I added to my index short some. And then I added some small-ish commodity stock positions like Stelco, Algoma, Peabody Energy, and Diamcor Mining (Russia is 30% of the diamond industry!).

(Note: I also bought JJG, the grain ETF, and added a little to BIOX. I forgot those ones in the original post).

None of these long positions are very big. I just thought if I’m going to have some long exposure, this seems to be the place to do it.

My basic thought here is that A. I have no idea how events are going to unfold but B. It seems unlikely that something will happen in the near-term to lift the sanctions that are going to impact all these commodities that Russia exports. I guess what I am saying is that while I don’t know what the world will look like tomorrow or next week, it is hard to imagine a fast return to status quo.

That said, let me emphasize – small positions. I tweeted today that the “best advantage a tiny retail investor has is ability to just sit it out”. I did that during COVID and I made a pretty big move in that direction today.

This is all just to hard to figure out. I’d rather stand aside and wait.

I don’t really think the market rally on Thursday and Friday is based on sound footing.

The rally is being led by all the same stocks that are in the middle of a triple waterfall decline. It seems to be being driven by a combination of very over-sold conditions, having some “relief” that the invasion is now upon us and not just a foreboding specter on the horizon (a thought that makes me ill), and the expectation that this will slow the Fed tightening.

It just doesn’t ring true to me, not with this disaster that is unfolding. The only one of the 3 points above could produce a lasting rally is this: if the Fed stopped tightening (though it hasn’t started right?).

Whether or not the war in Ukraine puts the Fed on hold, I don’t see how it is not going to make inflation worse. It is going to make shipping more arduous, make food prices go up, make energy prices stay up. And if the Fed does decide not to act, won’t the bond market eventually do it for them?

So I’m staying very cautious. I’ve avoided the slaughter so far, and this does not seem like a good time to change tact.

That said, I’ve made a few changes to my portfolio since I last wrote. Not too many, but a few.

The biggest change I made was to sell my gold stocks on Thursday. Pretty much the whole lot – I still own a little Calibre Mining (this was my old Fiore position) and Superior Gold, but that’s it.

Partly, this is sentiment driven. I saw the big red candle developing after the invasion announced and I know enough about gold to realize that big red candles are rarely shrugged off. As gold stocks sold off during the day on Thursday, I sold mine too.

I might buy back but I’m not really sure how this plays out. The thing that worries me is that with the sanctions being announced, the one thing Russia can sell is gold. Gold bugs can argue all they want that this is a good thing, that it justifies gold’s place as a reserve currency, but it seems to me that selling is selling.

Other than that, on the long side I added a small position on Diana Shipping, which so far has worked out, a position in Copper Mountain, and I should have added to Rada but I’m an idiot. Oh, and believe it or not I actually added a SaaS name – Alteryx!

Don’t get me wrong, I am still more short SaaS/momentum than long. Thursday-Friday was a bit painful in that regard. But Alteryx is something foreign to the SaaS world. A company that raised growth guidance to ~30% and has a low (6x) Price/Sales ratio. I might be wrong, Alteryx may just be a bad business. I’m still trying to figure that out so I won’t say much else about it until I do.

One-Hit-Wonders

But the short-SaaS/momentum story feels like it is getting old. Yesterday’s news. I am moving away from those shorts and towards some other, more industrial, shorts instead.

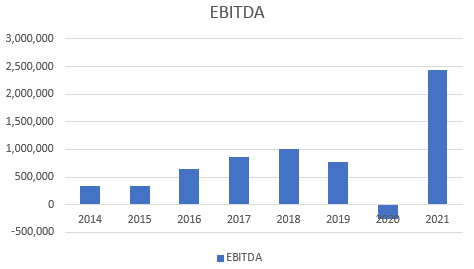

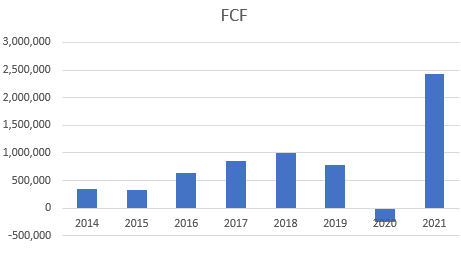

It strikes me that there are a lot of businesses, where if you go back and look at cash flow and EBITDA over a 10 year period, there has just been this massive spike in the last year and a half that is completely unprecedented. And the more I think about it, the more I think this is a bubble itself.

It is not a “valuation” bubble. These stocks tend to trade at less than 10x EBITDA, sometimes well under that. Single digit FCF in some cases. But I think that might be because the bubble is in the business instead.

Consider Olin. I owned the stock for a bit last year. But I got to thinking, in part because the price action seemed so poor, about whether this was really sustainable. Take a look at how Olin’s EBITDA and FCF compare to prior periods.

While I would love to believe that Olin is in a new paradigm, I have my doubts. And Olin is far from the worst in terms of the one-hit-wonder factor. There are far more egregious offenders. All the building material companies, the retailers – particularly the sports stores (remember BGFV?), steel, maybe even aluminum eventually. The list is very long.

While the triple-waterfall SaaS and momentum collapse gets all the headlines, these sorts of names look suspiciously similar to me.

Vidler

With the Ukraine situation so fluid and just so awful, I’m going to go in a completely different direction here and talk (again) about a stock that has a thesis untied to most of this geopolitics.

This is the routine that I have every morning since mid-November:

Get up and go downstairs

Put on the coffee in the coffee maker

Get the coffee and go to my workspace

Open Chrome

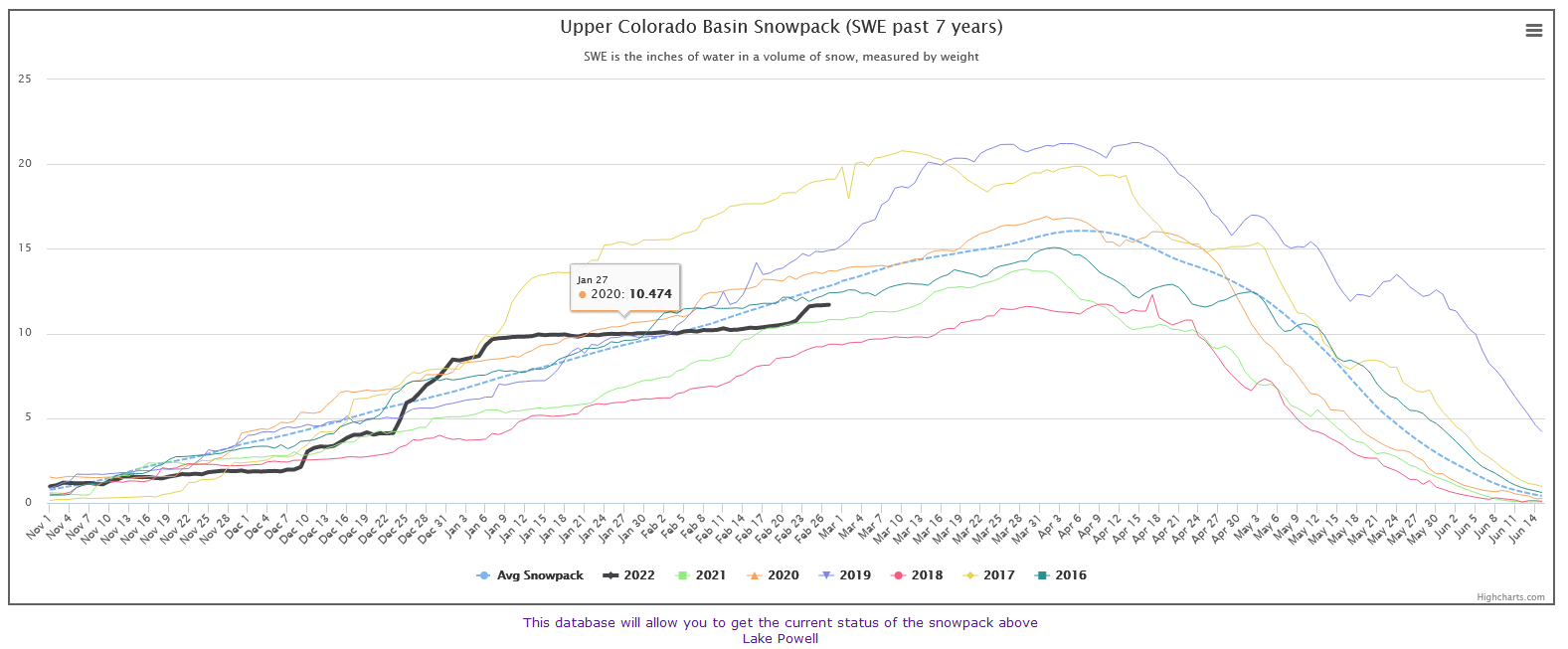

Check the snow pack of the Upper Colorado Basin.

The irony is that I don’t live anywhere near the Upper Colorado Basin. I’ve never been to the Upper Colorado Basin. But for the last 4 months it has been the most important piece of data for me.

I wrote about Vidler back in early December. It was then and is again my largest position. If you follow my portfolio though, you’ll notice that for a few weeks I sold some of the stock, and then bought it back.

That sale and repurchase relates to this chart:

Wouldn’t you know it that about a week after I wrote about Vidler, the Upper Colorado Basin had the biggest snowfall that it has had in years.

Through the Christmas break I was sweating bullets. Every day I’d watch the snowpack rise. And I’d get more nervous.

I’d get nervous because at the end of the day, Vidler’s near-term stock price is all about drought. While the long-game is water shortages accruing over decades, over the short run the stock price is about whether there is a problem right now.

Investors care about what happens next quarter or at most this year, not what is going to happen over the long-run. While Vidler’s sale of water in December is a big positive, at the beginning of January I was not convinced that Vidler’s stock would do well if we saw a record snow pack in the Upper Colorado Basin. If Lake Powell and Lake Mead began to rise significantly, and investors began to look at the story as an “eventually” and not an “emergency”, I feared the stock would be re-rated down.

So I reduced my position in Vidler by about 1/3, to a point where I slept better with that concern. And I waited to see just how much snow would fall.

I waited. And I waited. Just as the amount of snow that fell from Christmas Eve to New Years Day was nearly unprecedented, the lack of snow since then has been equally unprecedented.

We did have a blip of snow last week. But even so, the Upper Colorado Basin snow pack is now below the 5-year average. And that 5-year average is not a good baseline – it is the baseline of a drought.

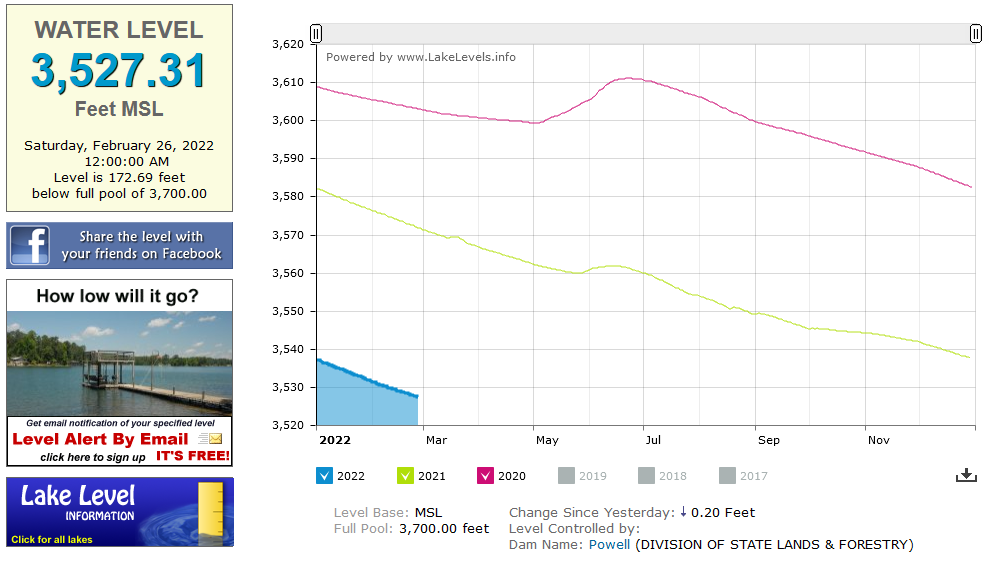

We are starting to see the articles pop up again. This article from the Colorado Sun says that projections for Lake Powell are too rosy.

In the article, they point out that “Ten or 20 feet can make a big difference at Lake Powell these days. Water managers are closely watching whether the water level will drop below 3,525 feet above sea level. If it does, it threatens the ability of Glen Canyon Dam to generate power.”

Lake Powell is 2 feet away from that level right now. And it is going down every day.

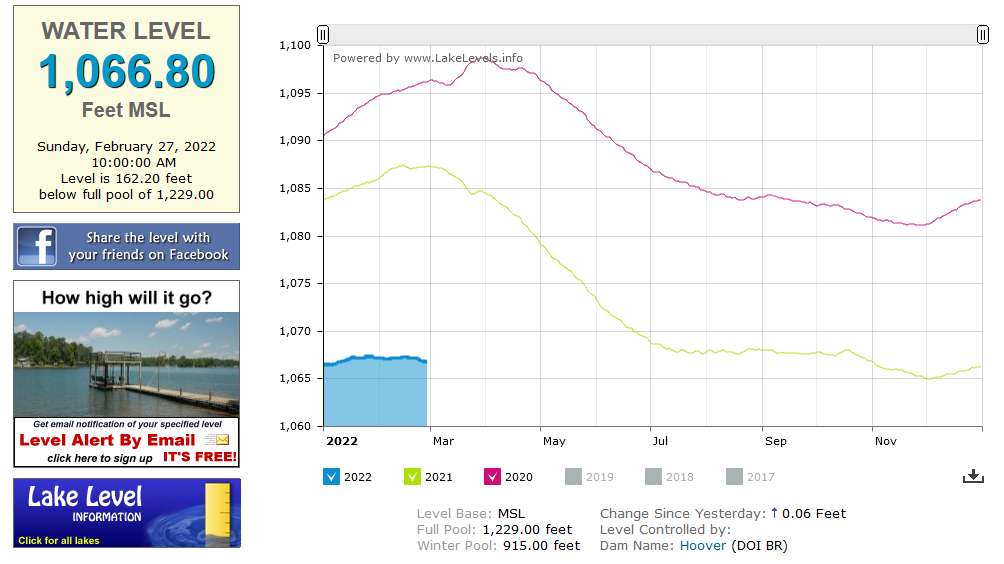

Lake Mead is no better. The usual winter bump has basically not happened this year.

The other thing about this article is that it is about the models, and how the models aren’t predicting accurately. I find that interesting. This is a case where the models are painting the picture that everyone wants to hear. So it kind of makes sense that no one (up until now) is questioning them. This isn’t the first time I’ve read that the models are too optimistic. It has come up here and there. And I really wonder if the problem here could be much bigger than anyone has admitted, because the consequences are so severe.

I wrote back in early December how “stocks felt heavy”. This felt like a bear market to me, even though the indexes were holding up extremely well. They went on to new highs in the late December Santa Claus rally.

I went on to describe how it felt eerily like the second half of 2015. And how I was worried that the first month of 2022 would be like the carnage of the first month of 2016.

That feeling certainly turned out to be right. We have seen a very similar result. And now that so many stocks have become incredibly oversold and have charts that have gone straight down, it looks like we might rally.

But I think this will be a bear market rally.

That means that I need to be careful not to keep longs too long. I’m hopeful that I can get some nice bounces in the beaten down names I’ve been adding to over the last couple weeks. But I have to be careful not to get greedy and hope for a return to prior highs.

I’m looking for a bounce. A strong one, at least I hope, but not a straight run to higher highs.

If I had any guts, what I would have done over the last couple weeks is just buy more biotechs, buy more small caps, load up. This has been a huge drawdown and so many names are trading at levels that do not value the business at very much, and in the case of Biotechs, value it negatively.

But as it is, I am betting with the money of my family, which I have done well with over the years and so my primary objective is not to blow it. Don’t lose, try to win where you can. The antithesis of the hedge fund that needs to perform to survive. So small risks only.

I did add to a couple biotechs on Monday when the fear was palpable. And there is one new biotech I added this week, on Wednesday after results. More on that in a second. But I did not go all in by any stretch. As much as I think this sector is poised to rise, I can’t take too many chances in case I am wrong.

There was also one non-biotech name that I added to this week that I wanted to talk about and think may be mis-priced here after a very deep drawdown.

Finance of America.

FOA has done nothing but go down since its SPAC merger was finalized in March.

The correct response to this chart would be – but this is a SPAC, right? Isn’t this par for the course?

The list of SPACs down 80% or more is very long. There are so many terrible businesses, or really just businesses that are way to early stage to be on the public market, that have gone public via SPAC, and now they are all getting killed.

But FOA is not really like most of these businesses. This not a LiDAR or robotics or EV company expected to begin generating revenue in 2030 and trading on the hopes and dreams of an investor presentation until then.

FOA is really kind of boring. They are simply a mortgage origination company.

That comes with its own problems. Like many mortgage companies, FOA is complicated. They originate loans, they securitize loans, their balance sheet is a mess of loans held for sale and debt held to fund them. Much of it is non-recourse and not really part of the book value of the business, per-se. There are Special Purpose Entities that hold the loans before sale and variable interest entities where FOA has no economic interest but does hold management over and so they are consolidated. It makes understanding the company very hard.

On top of that usual complexity, FOA has extra complexity because it is not a usual origination company.

Your typical mortgage originator sells the majority of its loans through Fannie and Freddie securitizations. These are called agency loans. These are loans to prime borrowers that qualify to be insured.

Fannie and Freddie originations are pretty commoditized. There are lots of mortgage origination companies that can make these loans, it doesn’t lead to much moat and margins are tight.

However last year with COVID, this market did what a lot of markets did. It went on tilt. Margins skyrocketed to (I believe) over 600 bps at one point as people refinanced their homes en masse . The usual level is more like 150-200 bps.

That was great for FOA because they made a lot of money along with every other mortgage originator.

So FOA rode this wave and came public around March. Which is about the same time that the dislocations in the mortgage market began to ease.

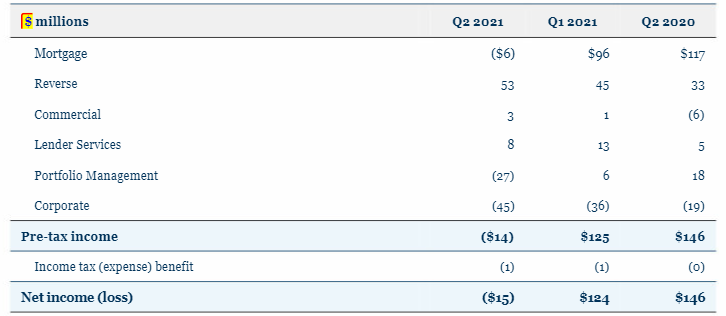

The consequence is that the blowout earnings of 2020 reversed in 2021. Their Q2 earnings look like a mess.

So what do you think a stock will do if it goes public and the first quarter out of the gate its highest income business (Mortgage) goes from $117 million of pre-tax income the year before to -$6 million this year?

It’s going to shit the bed is what its going to do.

You can try and explain all you like that this is “in-line with industry trends” (they did), that there are a bunch of “non-recurring costs” that impacted the results (there were) and that mark-to-market accounting hammered the numbers even more (they did).

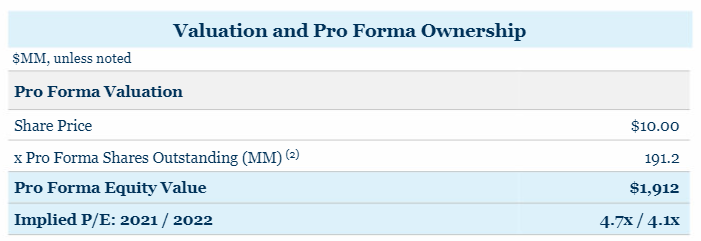

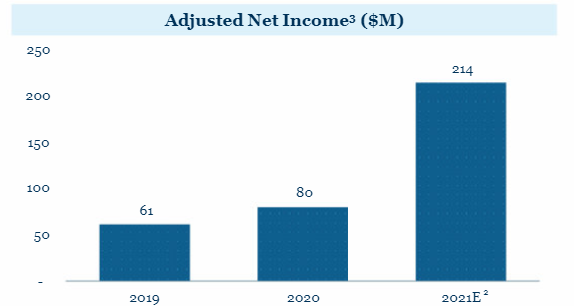

No one cares. Most of your shareholder base (the one’s that can sell the stock) only have a foggy idea what you do. They bought you because you were a SPAC that went to market at a $1.9 billion equity value on the belief they were buying something at 4x earnings (see below, from the March 2021 presentation).

And now they are saying, these guys lost money? Get me the hell out of this!

So selling begets selling. It doesn’t help that gain-on-sale margins on mortgages continue to normalize through Q3 and Q4. Take a look at the chart of Rocket Companies, LoanDepot or even Mr. Cooper. They are all going down because mortgage gain-on-sale profits are coming back to earth.

Ok, so why am I investing in this hot mess?

Because like I said at the start of this, FOA is not your usual origination company. And I don’t think the market has bothered to look at it enough to figure that out yet.

Yes, FOA has an origination business. But a large part of that origination business is non-agency mortgages. Think subprime. And of the business they have, most of it is purchase, not refinancing.

So ok, that could help. But its still originations.

The bigger part of the story is that FOA has 3 other businesses that are not originating mortgages for people buying or refinancing their house. These businesses are:

Reverse Mortgage

Commercial Lending

Home Improvement loans

Each of these are far more niche than mortgage originations. That also means, they aren’t as much a commodity business that is subject to low margins. They aren’t nearly as rate sensitive.

Together these businesses make up what FOA calls their Specialty Finance and Services segment.

Likely because they recognized that their stock was in deep doodoo, FOA scrambled on their third quarter call to try to explain to investors that they are not just a mortgage origination company. They outlined a 7-point “market mis-perception” case:

Their comparison set is mortgage companies

Yet their origination segment is only about 20% of earnings

Individual companies in their reverse, commercial and lender services businesses trade at far higher multiples than mortgage companies and then them

The mortgage platform they have is geared to purchase market

It is also geared to non-agency which they think will reduce volatility compared to agency dependent refis

They plan to double down on reverse, commercial and home improvement lending

It didn’t really work. It is tough to change perception when you are a SPAC that went to market as a mortgage company, hardly any brokerage covers you, and all the mortgage companies and SPACs are getting creamed.

So where are we now? Well, FOA gave the following guidance for Q4:

It works out to about $70 million of adjusted net income for the quarter. This is less than the $75 million of adjusted net income in Q3. So still not good right?

Well, yes and no. Even if FOA meets guidance it is down quarter over quarter, I’ll give you that. And that is largely because the mortgage business continues to normalize (meaning go down), which is really no surprise. A bank I follow closely, called SB Financial Group, has a large origination business. They reported Thursday. Their originations were down 25% year-over-year and their gain-on-sale margin was down from 503 bps to 288 bps. LoanDepot hasn’t reported, but their guide was for Q4 gain-on-sale margins of 210-260 bps versus 290 bps in Q3.

So yes, earnings are still being dragged down by mortgage. But the rest of the business – the Specialty business – is doing quite well.

At the midpoint, adjusted net income from SF&S would be at $64.8 million in Q4. In Q3 it was $59.6 million. This year it is up pretty significantly over 2019 and 2020.

The problem is the mortgage business has been down more.

But where we are now is an adjusted net income level of around $280 million annualized with the mortgage business contributing ~$20 million of that.

There are 191 million shares fully diluted. So that works out to $1.50 EPS. The stock is under $4, trades at about 2.5x PE.

While the stock traded at 4x PE at the time it went public, that was on a much higher “E” and those were on peak, unsustainable, earnings. Now it is on earnings largely from SF&S, which is growing.

I’m not the only one sniffing around this stock. Leon Cooperman was on their Q3 call asking questions. Cooperman held 900k of Replay Acquisition Group before the merger, but has increased his position to 4.4 million shares in Q2 and 4.7 million shares in Q3. He has been buying all the way down.

Cooperman focused his questions entirely on the long term:

Just a couple of high level questions. I noticed on your press release of earnings, you referred to yourself as a high growth consumer and specialty lending business. I think the stock sells is somewhere between two and three times earnings, we’re starting to see just high growth. I know you spent a lot of time this morning discussing why, do you think the market, are you relying upon the market just to wake up and change the expectations or there proactive things you could do, I notice for example that GE is breaking themselves up in the three companies. So, that would be question number one.

36:19 And related to that question is, forget about the next quarter, but on a five-year basis, when you refer to yourself as a high growth consumer specialty lending business, what kind of growth do you think the company can support on a five-year basis per annum? And secondly, on the cover sheet there are three earnings numbers, it’s the basic $0.36, there’s the fully diluted zero point two two dollars, and then there is the adjusted net income of seventy five million dollars or zero point three nine dollars, which do you think given you’re now into the business the most relevant to your business.

36:50 The kind of number that we shaped dividend policy going forward or are the kind of activities? Those are two questions, and congratulations on a good quarter.

The answers were that they aren’t going to break themselves up because the mortgage business generates customers for the specialty businesses, they can grow SF&S at 15% per year and that we should focus on the adjusted net income number.

Cooperman has always been a pretty astute mortgage investor. I followed him into Arbor Realty years ago (at about the same price as FOA is at now, coincidentally) and did quite well alongside him.

So that is FOA.

A Little Bit of Biotechs

I finally bought more Eiger this week. I waited and waited and waited to add to my position but when it cracked down to $3.55 on Monday I said enough is enough and doubled down.

I did add one other new biotech stock this week. Checkpoint Therapeutics.

I say new but I owned this for a week around New Years. I bought it then as a tax-loss selling idea and it didn’t work so I quickly sold. Now I bought it back.

But this time I buy it back with a bit more conviction.

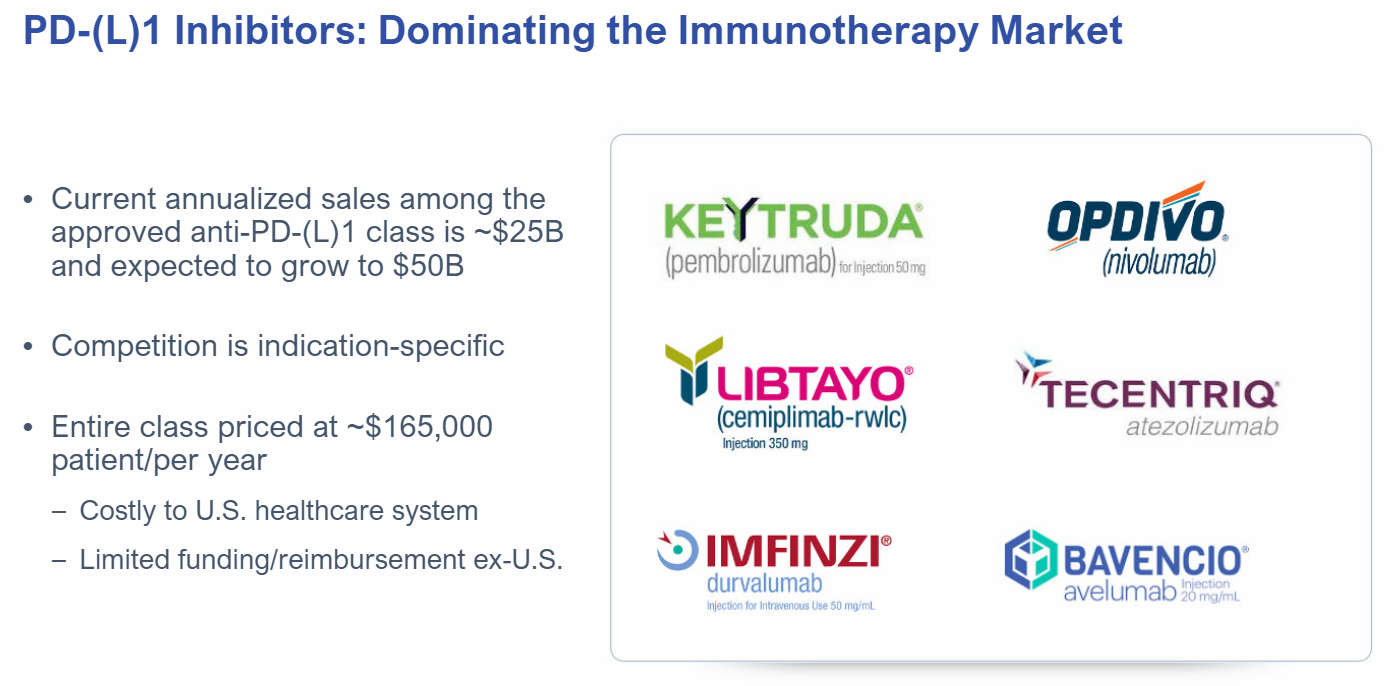

The reason I have some more conviction is Checkpoint released results on their anti-PD-L1 drug candidate.

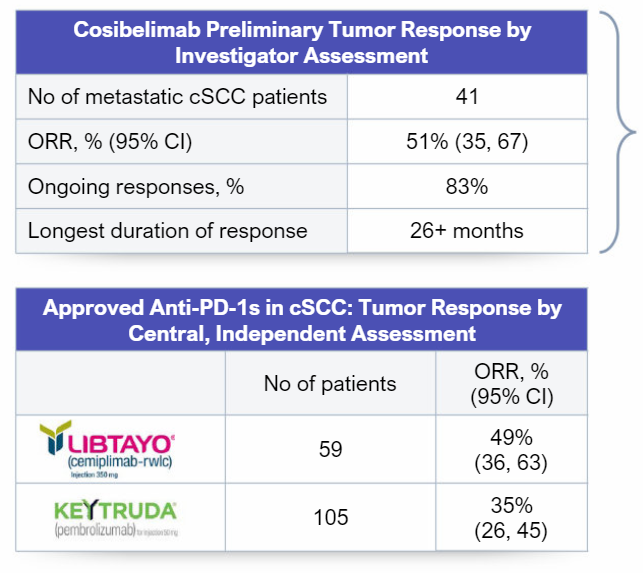

I had said that Cosibelimab had released some interim results previously. Here are those results, followed by the new results:

And here are the new results from the larger patient cohort:

They noted that “the median duration of response (“DOR”) had not yet been reached at the data cut-off point (76% of responses are ongoing)”.

Compare the final results to Keytruda (Merck) and Libtayo (from Regeneron) results. They look pretty much the same, if not better. And the safety profile looks good too. Here is what B Riley says:

we call out that the response rate is in line with or better than the two approved PD-1 inhibitors on the market in this indication, the complete response (CR) rate is trending positively, and the safety profile indicates cosibelimab could be a preferred combination partner

This is how HCW titled their note the day of the release:

Again, this is a very big market. Checkpoint’s strategy is to undercut the big players (Keytruda is owned by Merck, Opdivo by Bristol Myers) on price and take a piece of it:

So I don’t know. Either the analysts are missing something, as am I, or this is just such a bad biotech market that even if you get just the right results, the best your stock can do is stay flat.

But I could be wrong. They do have to muscle their way in against big-Pharma. And its not a better drug, other than maybe the safety profile. Maybe that is what is holding the stock back.

But it also is a very bad biotech market. I’m guessing that it has at least something to do with the latter. I think it is worth a small position, at least for a pop.

Corrections like this are very hard. No matter what you try, it is extremely difficult to make money on days when the market is down 90 points.

I can almost stay flat on my margin account because I am short enough SaaS and momentum stocks to make up for the carnage on my longs.

But in my RRSP or my wifes cash account, even though the stocks I hold there are more weighted to dividend paying, and even though I have the index hedges, it is really tough to not lose money on a day like Friday.

Think of it this way – on a day like Friday you are likely to have 3-4 stocks down 5%. The index is down 2%. So you need 2.5x the holdings in the inverse index just to make up for those 4 stocks. Pretty quickly you’re biggest risk is all the inverse ETF you hold (which can go south on you quickly). You just can’t make the numbers work. Not to mention that if you are putting that much into just beign hedged, you might as well just be holding cash.

I think that the only time I managed a correction ideally was during COVID. And that was just because it seemed so obvious at the time to just get out entirely.

But now? I have been dragging my heels on getting out entirely. Because things just don’t seem that bad. The market seems bad, but the world doesn’t seem that bad. And many stocks are very inexpensive.

So I’m hedged, but I’m not cash. And there is a difference between the two in that when the shit really hits the fan, as Friday showed, hedging does not mean you don’t lose money.

You could put my investment ideas into 4 buckets right now.

A bunch of banks/insurers

A bunch of biotechs

Gold/metals related

Small cap idiosyncratic

I’m going to go through why I own each of the first 3 buckets.

Banks

Bucket 1 is the biggest. I own a bunch of regional and community banks that all trade at very low multiples (most are close to tangible book and at or under 10x earnings).

During the first two weeks of the year, these stocks actually did really well. As I wrote about here, my portfolio was actually going up a little, and it would have been going up a lot if not for the drag of biotech.

But this week, not so much. The KRE (that is the regional bank index) gave up its gains from the past two weeks. CUBI had a bad week. Most of the banks I own gave up the previous weeks of gains.

Do I sell? Get out?

It is hard for me to agree to that.

The outlook for banks and insurers, with Omicron likely ending COVID, with rates on the rise, with an economy that should be at least okay, should not be that bad. And the stocks are some of the cheapest one’s out there.

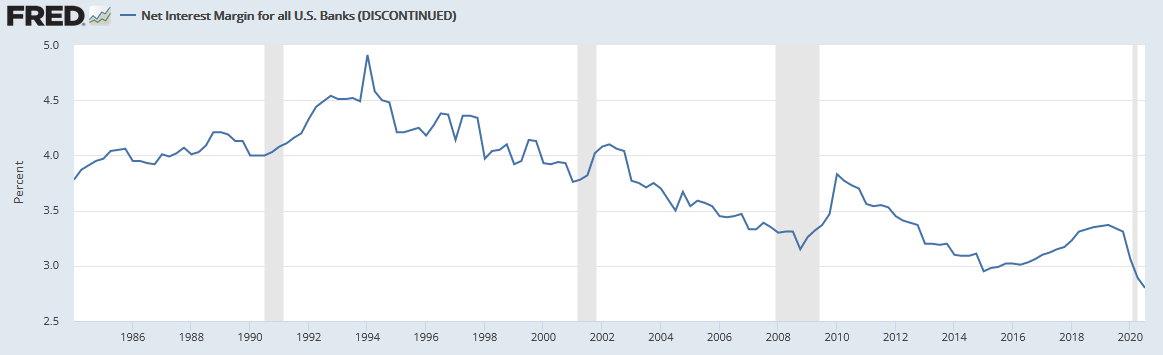

I also think there is a chance we see something that hasn’t happened in years. Expanding interest margins.

I don’t think the Fed, the Bank of Canada and others can raise short term rates too far because too many households have variable mortgages that depend on those rates. But they don’t control longer dated rates.

I wonder if we could see a world where short term rates remain low even as longer term rates slowly rise over time. I’m not talking about a wild-hyper-inflation-type rise like the crazies are shouting about. But a modest rise, so that net-interest-margins for banks maybe go up 0.5% in the next year.

Which should be beneficial because the net interest margin of banks has shrank so much over the last 10 years.

If you go through the banks I own, even though some of them have developed other businesses that don’t depend on interest, they still derive a lot of their income from interest margin. And with interest margins so low right now, for many a 0.5% increase would be akin to doubling their non-interest-income business. So its significant.

To put it another way, with commodities the old saying was to buy when the PE was high and commodity prices low and sell when the PE was low and commodity prices high.

With the banks, we are at multi-decade lows in NIMs, but the PE is low. Far lower than the market average.

So sell now? Ehhh…

On to biotechs

My one big mistake over the last 4 weeks has been thinking that buying biotechs at prices near or under cash with drugs in late stage trials would be a good idea. My premise, which has proved false, was that these stocks couldn’t possibly go below where they were during the peak COVID panic.

As it turns out – they can, and cash has only been a partial counter force against further share price losses. When the XBI goes down, they all go down, idiosyncrasies be damned. My only redemption has come from my SaaS and momentum short trades which apparently are tied to the hip with the XBI (for now) and thus makes money as these names lose money.

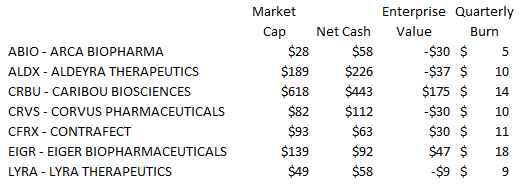

Where we are now, four of the biotechs I own have negative EV’s based on Q3 cash levels. The other 3 are getting there.

Do I sell?

Well clearly I’ve been wrong. Cash on hand has been only a bit of help. But at this point: A. apart from Caribou these stocks are all trading at only slight positive or negative enterprise values, B. apart from CRVS these stocks are at levels that are lower than they were during the worst of the COVID panic and C. they are all terribly, terribly oversold.

Nothing fundamentally has changed with these names. They are all closer to their next data read-outs then they were a month ago.

And here’s the thing I keep thinking: these names aren’t goosed by COVID numbers like a Netflix or Peloton. We are seeing an unwinding of the COVID trade, sure, makes sense, but these are just collateral damage to that. In fact, th forces at play for these biotechs are the opposite: because of COVID, drug trials didn’t get done, patients didn’t enroll, everything slowed down. Now that is ending and we can get back to normal.

I also don’t buy the argument that biotechs are rate-dependent stocks like SaaS/tech companies are. Consider this chart, which was posted by @Amarillo_Slim1 on twitter.

Biotech stocks have traded at a far higher EV/cash multiple in the past during periods where rates were much higher. So the “long-dated-assets-discount-rate-rising-present-value-compression” argument doesn’t hold water to me.

Finally, big drawdowns with biotech stocks just happen. And then they end. Consider this chart of Eiger, which is the one biotech I’ve (unfortunately) held through this entire drawdown:

This drawdown is unique in terms of the absolute price it has taken Eiger down to. I honestly never would have thought we’d see a $3-handle on this stock, what with an approved drug generating revenue and with Phase 3 results on HDV less than a year away.

But what is not unique is this steep, sudden drawdown. It has happened over and over again. And most of the time, the stock has recovered almost as fast as it has fallen. If history is any guide, it could be back to $6 in a month.

That makes me very reluctant to bail out here. Even as each of these stocks painfully slip a few cents more almost every day.

Eiger also presents an example of another point. Funds are getting involved with some of these beaten down biotechs.

The funds and clients of Columbia Management Investment Advisers now own 20% of Eiger (or more if they continued to buy this week). They have bought over 6 million shares in the last year including over 1 million in the last 3 months.

The funds mentioned in the filing that hold the bulk of the shares are Seligman Tech and Seligman Offshore funds. These don’t look like dumb investors to me. They are run by Paul Wick. His funds were profiled in November in The Institutional Investor:

A hedge fund manager best known for running long-only mutual funds is enjoying one of his best years in recent memory.

Paul Wick’s Seligman Tech Spectrum fund is up 24.37 percent for the year through October, well ahead of many other tech- and internet-focused funds, a number of which have been mired in the red for most of the year. “We’re playing in a different area that they pretty much ignore,” Wick asserted in a recent phone interview.

Wick is the lead portfolio manager for the Seligman Technology Group at Columbia Threadneedle Investments. He has been heading up Seligman’s technology investment group since 1990.

Wick is not a momo growth guy, which is probably why he has been around for so long:

“We are fundamental growth investors [who] are valuation aware,” Wick stressed in the phone interview. “Others have a tendency to forget about valuations and drive off [the] cliff periodically.”

Wick believes his group is more focused on a company’s profit margins and cash flow, as well as companies repurchasing stock or doing accretive acquisitions.

Anyway, if you read through the 13D filing, you can see that Wick’s funds and clients were large buyers in late December in the low $5s. Now we are a buck lower.

I added a bit to my biotechs on Friday. I have been cautious the last two weeks and just tried to do nothing with these positions. But Friday I broke down and added to ABIO and ALDX. Both of these stocks are WAY below cash and they have years of runway given their current burn.

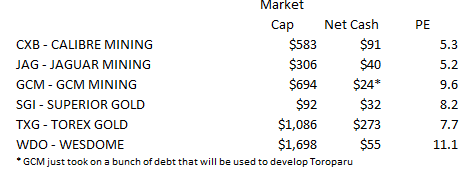

Gold

Gold is the last single theme bucket and the last bucket I will talk about.

But what can you ever say about gold stocks? Cuz who the hell knows.

If it really is a market collapse gold stocks will go down… maybe. But maybe not. During COVID they actually went up until somebody gamed the 3x ETFs and then they gave up all their gains and then some in like 3 days.

What I do know is that tech and SaaS are long duration assets. That means they are dependent on their earnings stream many years away. In the case of some of these SaaS names it had gotten so stupid that you would have to go out 30-40 years to truly realize the value on a discounted cash flow basis.

Gold stocks, on the other hand, are (like bank stocks) the opposite. They are short duration assets.

Banks give you the earnings right now, dividends right now and in some cases buybacks right now.

Gold stocks do too. In fact they are even shorter duration – basically the length of the mine, especially now when exploration is priced at a big, fat zero. Its all about today’s cash flow.

The gold stocks I own are also very reasonably priced.

Soooooo… the case can be made.

The trick right now is figuring out if these stocks can go up while other stocks go down.

It seems like the growth-cohort of SaaS/momentum/stay-at-home stocks is finally seeing their good fortune come to an end. As I tried to point out in my last post, you can make a case that there is further to fall.

And quite honestly I have a hard time believing that the descent of the growth stocks will be over until we finally see Tesla give up the ghost. It is the unquestionable kingpin and as long as it still stands the triple-waterfall collapse will not be complete.

With that as my premise, the question I can’t answer is if other stocks can go up if Tesla and all the other stocks held up by it keep falling.

If I knew the answer to that I I wouldn’t have so many hedges on my portfolio that I am essentially barricading it like I was about to be attacked by the huns.

But I do know that the stocks I own are the antithesis of growth/SaaS/momentum stocks. They are very low PE stocks. They are short duration stocks.

And I do know that during a regime change there are new winners. And even with the pummeling, I have optimism that I might be in 1 or 2 of those.