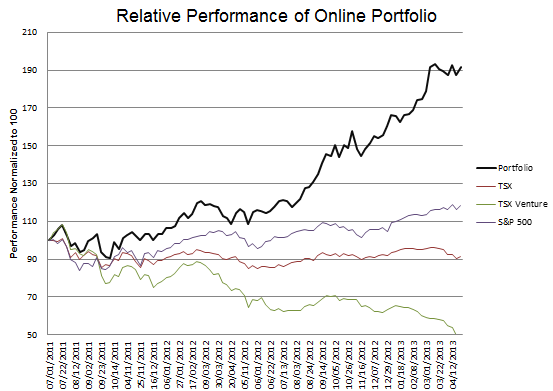

Portfolio Performance

Portfolio Composition

Week 42-43 Trades

Biweekly Portfolio Updates

Those who read this blog regularly may have noticed that I have begun to post my portfolio updates on a bi-weekly basis. Every week was just too much. First, not enough happens to my portfolio every week to devote an entire post to it. Second, its a pain to copy and paste the pictures and update the chart every week. That is time that would be better spent doing research. Third, an perhaps most importantly, I have found that with weekly updates I was becoming a little too focused on my short term performance, and I think this was conflicting with my investment style.

When I think of how I have made money in the past, it has rarely been from making quick trades in and out of stocks. I generally make my money by sitting. Somewhat paradoxically my best investments have tended to go through a significant period of pain before eventually moving in the direction that I had originally expected them to.

I have to accept, and to some extent expect, that my portfolio is going to go through significant drawdowns at times. Those drawdowns are challenging. These drawdowns cause me to reevaluate, and either to strengthen my conviction in a particular position or to realize the folly. A lot of the time I waffle back and forth on a stock, buying and selling it at the margins, before finally coming to a conclusion on whether to keep it or not.

In the course of the last year I have found that there is extra stress associated with keeping a public portfolio, where the performance is there for all to see, even though most of the people that read this blog are strangers. I don’t want to make bad decisions. I feel like showing my portfolio every week may be affecting my decision making ability, at least a bit. So I am going to try showing my portfolio every two weeks from now on, as this will make the portfolio less of a focus of the blog, and will allow me to focus on the research topics that I really enjoy writing.

With that said…

Out of Aurizon Mines

Without of a doubt my most significant move over the last two weeks was to get out of Aurizon Mines. On the downside, I got out of Aurizon before it jumped this week and became one of the TSX best performers for the week. I’m not terribly upset with that because I bought Atna Resources, Keegan Resources, and Gold Standard Ventures with the proceeds.

The reason for swapping a producer for 2 development companies and an explorer was simply valuation. The explorers and developers have been hit extremely hard. I honestly never thought Atna would get back below $1. I mentioned Keegan Resources in a previous post, pointing out that I learned of the company from this Mineweb article, where they were listed in the table below as having one of the highest cash to market capitalization ratios of any of the juniors.

Its worth noting that Canaco Resources is also on the list with a 0.65 ratio. I bought Canaco back a few weeks ago at 85 cents and it has done reasonably well since then, trading back up to 95 cents. I would say that companies like Keegan Resources and Canaco Resources represent fairly low risk opportunities to take advantage of the current gold price environment. Both companies have 4x to5x more cash than their current yearly burn rate. Both companies have large deposits and they are actively exploring so there is the possibility of these deposits getting bigger.

The downside to both is that the deposits are so-so, and they are in Africa. Those are my only hesitation with these two stocks. But I am optimistic that the takeover of Trelawney may portend to a bottom in the deposit holding juniors. I was surprised that IAMGold chose Trelawney as a target. It was my impression that the deposit had disappointed and that it was going to be tougher to open pit than was at first suspected. It goes to show there is a price for everything. The price for Keegan Resources right now is hardly the cash in its bank accounts. Canaco is only a little better. I have to think that the mining intermediates must be looking at these possibilities with interest.

A future move that I could see myself doing in the next couple weeks would be to lighten up on these two companies a touch so that I can reinitiate a position in Lydian International. I sold out of Lydian when it looked like the gold sector was about to go into tank mode. I figured Lydian would go down (it did) but I also don’t believe that has anything to do with the validity of their project. The work I did on Lydian 9 months ago remains true today. The company could easily be a $7 stock if gold deposits began to be valued at $1500 gold. It has a much better deposit than either Keegan or Canaco.

I also added to my position in Gold Standard Ventures when they announced news of a second drill hit on their Railroad property. I listened to the conference call that was held that morning. It is still too early to know what Gold Standard has hit upon. What they know is that they have two large, long intervals about 300m apart, and they know from analogy that the mineralization and formation they are drilling into is consistent with some of the large Carlin gold deposits. The stock has a market capitalization of $200M now, so its no longer a cheap speculation; there is a lot of resource built into the share price. Still, I find it hard to lighten up at this point, when the evidence right now is pointing towards one of those large 5-10Moz Carlin deposits that would make a $1B market capitalization not out of the question.

Banks doing well… for now

The regional bank stocks that I have bought continue to perform well. I am going to write a more lengthy post reviewing the earnings of the 4 stocks that reported this week (RBNF, BOCH, BTC, and SHBI) so I won’t go into that detail here.

What worries me about the regional banks is that there is some evidence that the US economy is softening. In particular, the ECRI WLI, which I have been following for years, appears to have stalled out, and it fell for the 4th consecutive week this week. This softening makes me feel much better about the gold stocks I hold, but it gives me pause on the regional bank stocks.

Spain

Also making me feel much better about gold stocks are my worries about Spain. I now follow the Spanish 10 year and 5 year bond on a daily basis. Both are getting ominously close to crisis levels. It appears that my analysis from earlier this year (What is the LTRO going to do for Europe? And how does it affect my stocks?) is turning out to be correct. In it I wrote:

Like the Fed operations in 2008, the liquidity injections led to short term spikes but no lasting impact on the market. I am willing to speculate that the LTRO response with follow suit.

The ECB needs to provide further liquidity injections as the markets in Europe are rolling over. This time they are rolling over in response to Spain, which is somewhat more disconcerting than how they rolled over for Greece last year. I have been hunting the net for some recent Kyle Bass commentary on the situation, but I have not been able to find any.

Losing dollars because of the dollar

I am taking a haircut on the strength of the Canadian dollar. If you look at the difference between the Canadian and US dollar values of the account, you will notice that the Canadian dollar value is now a full 2% lower then the US dollar value.

More importantly, more than 50% of my investments are in US dollar stocks. The regional banks and mortgage servicers that I own suffer every time the Canadian dollar goes up. A move of the Canadian dollar to 1.10, which has been predicted by some, would hit the US stock portion of my portfolio to the tune of 10%, and my overall portfolio, in its current construction, by 5%.

I’m not ready to do anything about this at the moment. With the problems in Spain creeping up, I can imagine a scenario where the Canadian dollar corrects rather severely, and my US dollar assets act as somewhat of a hedge. But it is certainly something to keep an eye on. I would hate to see myself turn out right on my US stock holdings only to see the gains wiped out by currency movements.