Week 95: Setting the table (hopefully)

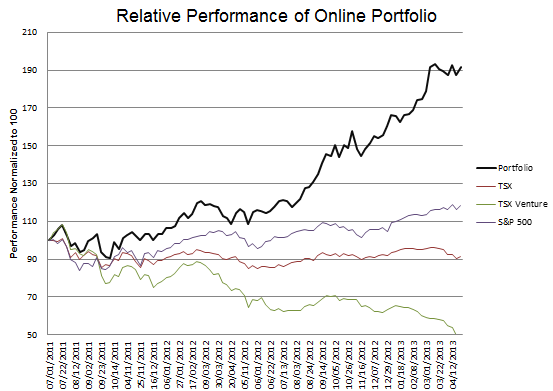

Portfolio Performance

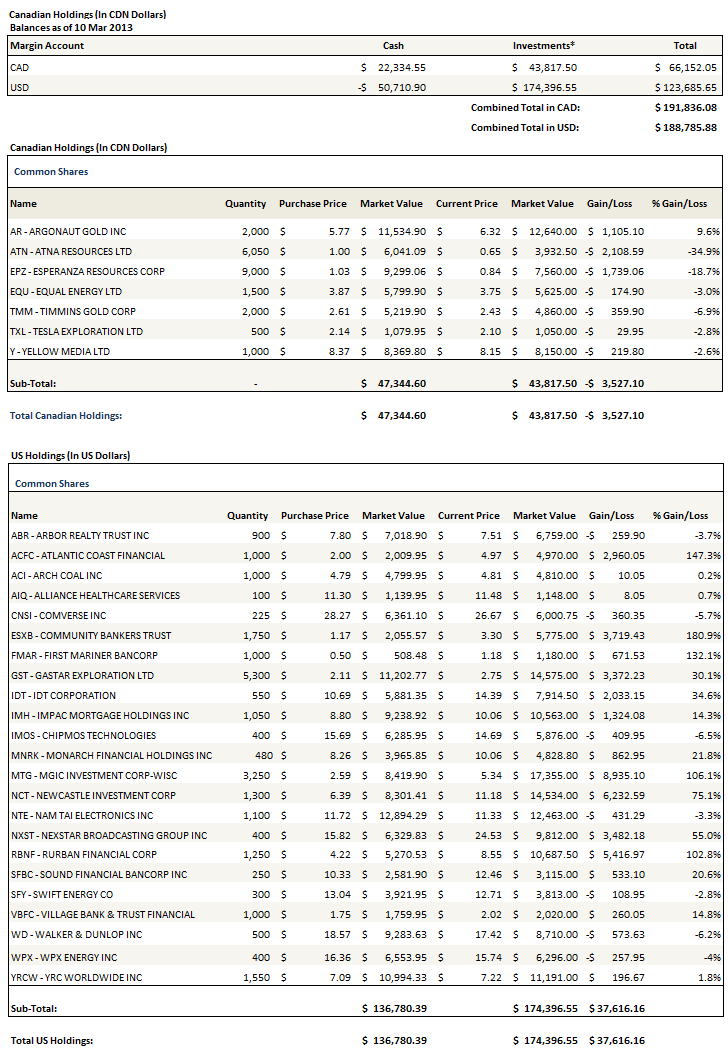

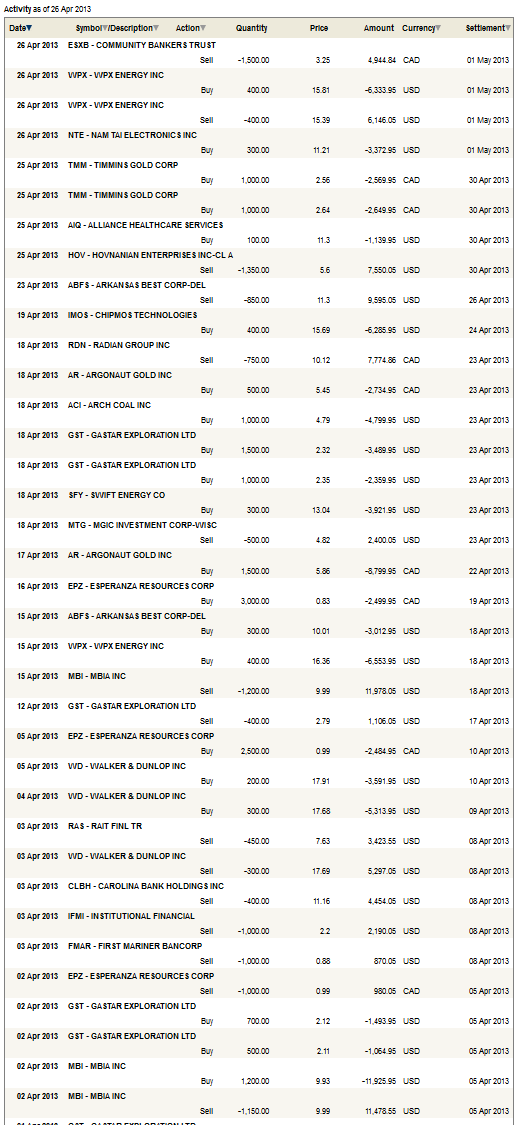

See the end of the post for a full portfolio breakdown.

Update

Since my last update I exited Radian Group, Arkansas Best and MBIA. The sales reflect a desire to redeploy cash in other opportunities as well as some lingering concerns about each company.

With Arkansas Best, its my uncertainty about the outcome of union negotiations. The negotiations were extended this week for a second time. An escalation to a strike does not seem out of the question. If a strike occurs the stock price may or may not get hit; while a positive resolution could be quite good for the stock in the long-run (see my original post about how Arkansas Best would benefit from a contract structured in a similar manner to the one that YRC Worldwide operates with) the uncertainty may drive panic selling. I’ve decided to wait this one out for a few weeks and see how it plays out.

Similar concerns about a rocky interim persuaded me to part with MBIA. To be honest, I’m a little beaten down by the name. I’m losing confidence that Bank of America and MBIA are going to settle. While it is in the best interests of both parties to settle before MBIA’s insurance subsidiary runs out of cash, I have to wonder whether the individual egos involved are going to prevent this rational conclusion from occurring. Its reasonable to ask: why now?

I wonder if this game of brinkmanship will go to the very last moment. If it does, what might happen to the stock price as the clock ticks down? If, for example, another couple of quarters pass and the cash level of MBIA Corp dwindles to the point where a seizure by the regulators looks likely, where does the stock go? I realize that the loss of MBIA Corp should not impact the solvency of the parent company, but I am less than sanguine that the market will be so reasonable. There are enough of shorts, there is enough fear, and the situation has enough complexity that I can imagine a scenario where the stock trades down on perceived uncertainty, warranted or not. I am going to be kicking myself if a settlement is announced, but I have resolved myself to accept that fate if it occurs, and if not I will wait until a resolution one way or the other is inevitable.

As for Radian, well its been a great run. I started buying in the $3’s, added significantly in the $2’s and now, with everyone else on-board, I am off to other pastures. And as with Arkansas Best, I remain heavily weighted in the sector by means of another company (YRC Worldwide and MGIC respectively), and so stand to do well from any sectorwide improvements. I plan to hold MGIC until the market develops the sort of love for the name that it has for Radian.

I removed the above mentioned positions in order to add to two new themes; gold stocks and natural gas.

On Gold and Gold Stocks

I described my gold thesis with the following tweets that I made on April 17th:

On April 18th I followed up these comments with an anecdote that struck me as relevant.

When I wrote about exiting most of my gold stock positions a few weeks back, it was always with the intent of getting back in once the wash-out was done. I just didn’t expect it so soon! While I am unsure whether the run on gold has run its course, I feel pretty comfortable picking up low-cost, high free cash flow miners like Argonaut Gold and Timmins Gold, and a well financed development junior like Esperanza Resources, at what I would deem fire sale prices. I suspect that even if the price of gold falls, we will not see the same lows in these stocks.

It was interesting to see the degree of negativity being directed at gold. I find it odd how one can be so sure that this is “the end” after seeing a few days of negative price movement. I remain skeptical, if for no other reason than that I have seen commodities and commodity stocks make wild moves in the past that, when looked back at years later, look like blips in the bigger picture. I have learned to put very little trust in the day to day swings of commodities, even if the swings are to the extreme.

But the more important point is that the good has been thrown out with the bad here. I can totally understand the carnage that we’ve seen in the low-on-cash developers and the higher cost producing gold companies (of which Atna Resources, which I am holding, is one). These companies are going to struggle at $1,400 gold and there is very little margin of safety if the price falls further. But to see equal or worse behavior from the lowest cost, highest quality names is ridiculous. Unless you believe that gold is returning to a three-digit number for good I believe that this was a tremendous opportunity to pick up quality golding mining companies on the cheap.

On the gold stock side of the trade I added the following stocks:

- Argonaut Gold (AR.to)

- Esperenza Gold (EPZ.v)

- Timmins Gold (TMM.to)

In addition I took a position in Alamos Gold (AGI.to) in one of my safest accounts, but did not in the practice account I follow here, so I won’t be speaking any further of it.

On NatGas

As for my natural gas thesis , I wrote about my expectations last Sunday. Since that time, Robry had some more bullish comments on natural gas.

The YOY deficit is now at its highest in years… estimated at 818 BCF (910 BCF Cap/gas-flow), while the YO5Y (year over 5 year average) deficit is at 121 BCF (185 BCF Cap/gas-flow). The baseline slope appears (from the last few weeks) quite shallow, aiming us at maxes up around 75-80 BCF for injections for the memorial-day timeframe at present supply/demand fundamentals.

The long-anticipated decline in NE production (the growth of which was covering for US declines elsewhere) looks just to be beginning, and adds to concern for the buy-side. As a reminder, NE production growth over the last 18 months has been a function of new wells drilled plus decline in unconnected wells. These shale-wells have very steep initial decline rates of approx 50% per year for the first couple years (IP through month 24) and with NE production approx 7.5 BCF, this years IP needs be around 3 to 3.20 (my own guestimate) to cover for the NE decline-curve. With both declining drilling and declining unconnected inventory, it gets increasingly impossible to meat the curve as time progresses, and declining production (which is not in the longer-term model’s 3332 BCF fall extrapolation) adds more layers to natgas bullishness.

Overall, natgas is more bullish than at any time since 2000/2001, and for those reading on the buy-side, you need to cover yourself quickly. Though natgas has climbed well into the 4’s, bullish fundamentals have not yet begun to be dealt with, and unless LDC’s are going to give up, they appear to be slow in dealing with this, perhaps waiting for late May / June to compete for natgas. “Large-specs” remain short natgas, a window of opportunity for the buy-side that will probably close in a few weeks (and with it opportunity for risk transfer to other energy markets by way of the markets).

I also thought this Seeking Alpha post, which explained some problems with the EIA coal forecast, was quite good and really fortified some of my thoughts on Arch Coal. I went onto the EIA website and he’s right, the production numbers appear to be overestimated.

I added the following natural gas stocks:

- Gastar Exploration (GST)

- WPX Energy (WPX)

- Swift Energy (SFY)

I also added Arch Coal (I wrote about it here), which is really a derivative play on natural gas prices staying above $4 and allowing significant coal-gas switching to bring inventories back in-line with historical levels.

Of the 4 companies, Gastar is by far the largest position, which I wrote about here. I think that WPX Energy has some upside because of its recent Niobrara Piceance discovery, while Swift has just been clobbered, appears cheap, and so I’m hoping that with gas prices perking up the bottom will be in. While I expect to hold Gastar for the long-haul, the other names are purely trades on the commodity, and I only expect to hold them as long as the bullish natural gas thesis remains viable. I also hold a call position in Exco Energy but I can’t have calls in the practice portfolio so that name is not on the list.

Hovnanian: Trading in the Common for the Preferred

Speaking of securities I can’t hold in the practice portfolio, I sold out of my position in Hovnanian and replaced it with a position in Hovnanian preferred. Unfortunately I can’t buy the preferred shares in the RBC Practice account, so I decided to just leave the position out entirely.

The preferred’s are an interesting idea. The Series A Preferred were issued in 2005, pay interest 7.625% and have a liquidation of $25. The senior secured notes carry covenants that restrict interest payments on the preferred if Hovnanian doesn’t meet requirements for fixed interest coverage. Hovnanian hasn’t met those covenants for quite some time and so the preferred’s trade at a steep discount to par (I bought mine at ~$15 and they trade at $16 now).

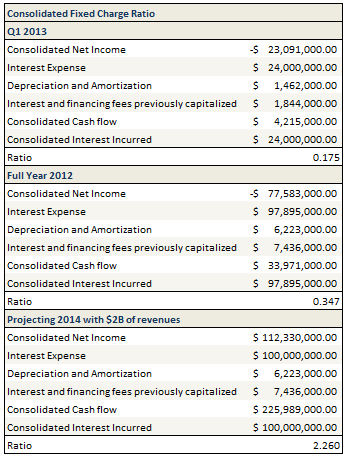

The covenant states that Hovnanian meet a minimum Consolidated Fixed Charge Ratio of 2:1 before they can pay interest on the preferred shares. The definition of the ratio is described here, and I have excerpted the most relevant passage below:

The ratio of (x) Consolidated Cash Flow Available for Fixed Charges for the prior four full fiscal quarters (the “Four Quarter Period”) for which financial results have been reported immediately preceding the determination date (the “Transaction Date”), to (y) the aggregate Consolidated Interest Incurred for the Four Quarter Period.

Where:

“Consolidated Cash Flow Available for Fixed Charges” means, for any period, Consolidated Net Income for such period plus (each to the extent deducted in calculating such Consolidated Net Income and determined in accordance with GAAP) the sum for such period, without duplication, of:

(a) income taxes

(b) Consolidated Interest Expense,

(c) depreciation and amortization expenses and other non-cash charges to earnings, and

(d) interest and financing fees and expenses which were previously capitalized and which are amortized to cost of sales, minus all other non-cash items (other than the receipt of notes receivable)

“Consolidated Interest Incurred” for any period means the Interest Incurred of Hovnanian, the Issuer and the Restricted Subsidiaries for such period, determined on a consolidated basis in accordance with GAAP.

The question of course, is at what point will Hovnanian exceed the minimum ratio necessary to resume interest payments on the preferred. I created a little table below that demonstrates where Hovnanian is right now on the ratio, and where they might be in a year or two.

The 2.26 interest coverage ratio in my projection means that they would start paying dividends at some point in 2014, at the latest in 2015, depending on the trajectory of revenues. My projection of 2014 is based on 15% growth on the top line in 2013 and 2014, and margins that fall within the range that the company has guided to in 2013. As the company makes progress towards this end, I expect the preferred will continue their trajectory towards par.

Floundering a little in the Small-cap Tech Space: Nam Tai and ChipMos

As I wrote about earlier this weekend, I took a rather regrettably ill-timed position in ChipMos (IMOS) last week. I also made my position in another small-cap tech name, Nam Tai, quite a bit larger.

Nam Tai was clobbered on Thursday and Friday after Topeka Capital Markets, which is quite possibly the only firm following the stock, decided to hack it’s estimates. The degree of the carnage was impressive; revenue was cut to $550 million in 2013 and $740 million in 2014. Earnings were reduced to 1/3 of the prior estimate.

I didn’t plan to add to Nam Tai and even after the downgrade came out and the stock dropped below $12 I sat on my hands. But on Friday afternoon as the stock threatened to breach $11 I decided that it was getting a little out of hand.

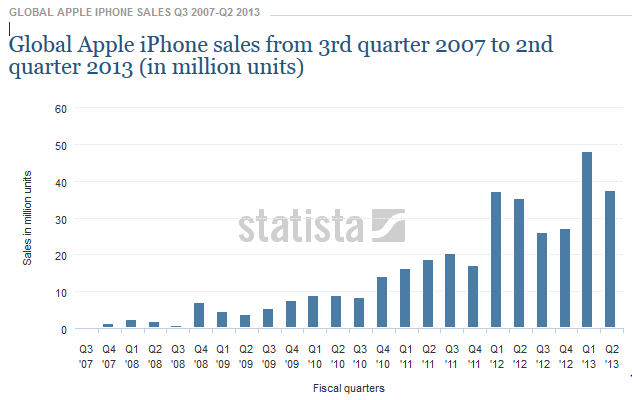

Now I don’t know if Topeka knows something. It seems that the analyst, Brian White, has recently been to China, though its not clear whether his conversations there included a visit to Nam Tai. But I’m really having difficulty reconciling the $550 and $740 million in revenue with the kind of ramp up in production that Nam Tai has been planning for, building for and discussing in past conference calls. It would be a collosal management whoopsie if they built out $3.6 billion of capacity and could only put together $740 million in revenue next year. It’s not even 20% utilization. This might make sense if we had just tipped into another great recession, but we haven’t. Things aren’t that bad. In fact iPhone sales, while weaker than hoped and below Q1 levels, are still projected to be above Q2 2012 levels.

Well Monday will be here soon enough so we will know shortly whether Topeka is truly prescient. I’m going to lose some money if they are. But I stand to make a decent stash if they aren’t. Given that the company is paying a 5% dividend, has $5 in cash, and, apart from the negativity from Topeka, there is little else to suggest that the company won’t be able to achieve significant earnings this year and next, I feel okay about this decision. A bit nervous that there is a bogeyman lurking that I haven’t figured out, but ‘youse take yours chances….’

Portfolio Composition

To see the last three weeks of trades, click here.

{kind=link}

NTE? That was brutual. Now what? Changing strategy to RE? Is it a buy now on valuation and cash per share? Sorry for the decline.

It was brutal. What can you say. Truly do take your chances and this time I lost. Topeka must have had an inkling. I’m out at about $7.50. You could make the argument the stock should be higher than $7’s given the cash and real estate but I have obviously been totally wrong about this and when I am this wrong I need to end it and move on.

On the HOV preferred, I understand that they may be allowed to pay dividends in a couple years, but what incentive do they have to do so? It is a non-cumulative issue, after all.

what did you think of MTG’s results? Thanks.

I got hosed on NTE too. I was looking at AAPL sales of iPads & iPhones. The number of units was higher than what the street thought. I bought more on Thursday PM. Huge mistake.

I just don’t get what is going on here…They get two good quarters and now they are thinking of shutting it down?

I always knew that panel manufacturing was a bad industry, but I thought NTE would be insulated because they were working with bleeding edge tech (retina displays) and were working with AAPL. That was true for 6 months. Now it is a free for all.

My guess is that the #1 & #2 producers have a size & scale advantage over NTE that will allow them to produce the panels a few percentage points lower. When your gross margin is 8% and additional 2% or 3% makes a HUGE difference. So larger players can lower price & try force NTE out.

AAPL needed NTE desperately for iPad 3 introduction & new iPhone. Now production has aligned with demand and AAPL is going to mercilessly squeeze suppliers.

NTE is still in discussion for the contracts. I think Koo will make the right choice. Why should they invest $200MM if they don’t get any assurance of volume work & pricing? If the poop hits the fan and NTE spends all their $ on new equipment, they’ve just lost the company…

The situation is not hopeless, but it does not look good.

We’ll see.

Were you going to take a look at Dex One? I though I remember you mentioning the stock at some point. Huge move today based on Kyle Bass’ comments. Thanks.

I did look at them but never in the detail I needed to talk about them on the blog and the stocks never retraced to the point I had hoped they would. Have a really tiny position in one account. My big position is in Yellow Media. Hopefully Bass comments will carry over to Yellow. Its all just phone books right? 🙂