On Friday a lot of large banks reported earnings. I have read through pretty much all of those transcripts this weekend.

None of the comments I hear from the banks are particularly concerning.

Which brings me to the question I have? Do banks usually not see what is oncoming until it is too late? Maybe they are not leading or coincident indicators?

I see a lot of comments about a impending crash. There is the longer run recession issue, but the more immediate one is that all this tightening by central banks is going to break something. Yet I don’t really hear it in these transcripts. Could the banks be so blind?

I really don’t know what the answer to that is. But they really don’t seem to see much of a problem, at least some far.

PNC:

Credit quality largely unchanged, not seen any meaningful deterioration in credit

In regard to our view of the overall economy, we expect moderate growth in the fourth quarter, resulting in 1.8% GDP growth for the full year 2022

JPM:

“Things are roughly the same” as 3 months ago

Health of US consumer: nominal spending still strong… both discretionary and non-discretionary are fine

Combined debit/credit spend up 13% yoy

Spending is growing faster than income

Banking system itself is “extremely strong” with “lots of liquidity”

“credit trends strong across the portfolio…credit quality remains strong”

“the current credit environment is benign. In fact, our net charge-off ratio in the third quarter remain near historic lows, and we are not seeing any meaningful early-stage metrics that causes concern.”

“would not be surprised to see an economic slowdown develop at some point”

C:

“There is accumulating evidence of slowing global growth, and we now expect to experience rolling country level recession starting this quarter.”

“The U.S. economy, however, remains relatively resilient.”

“while we are seeing signs of economic slowing, consumers and corporates remain healthy as our very low net credit losses demonstrate, supply chain constraints are easing, the labor market remains strong.”

WFC:

“While we’re closely monitoring trends with economic conditions expected to weaken given inflation, geopolitical instability, energy price volatility and rising interest rates, our customers continue to be resilient with overall strong credit performance and solid cash flow”

“we continue to closely monitor activity by segment for signs of potential stress and for certain cohorts of customers”

“continued high inflation has kept the Federal Reserve aggressive with rate hikes, leading the housing market to slow rapidly and the heightened uncertainty about the economic outlook and geopolitical events caused the financial markets to be volatile. However, labor demand remains robust, consumer balance sheets remain healthy, and customers have capacity to borrow. Overall, our consumer deposit customers’ health indicators, including cash flow, payroll and overdraft trends, are still not showing elevated risk concerns”Overall, our consumer deposit customers’ health indicators, including cash flow, payroll and overdraft trends, are still not showing elevated risk concerns”

Out of curiosity, I went back and looked at the comments of banks during the summer of 2008 on their Q2 conference calls. A couple of takeaways. First, they didn’t see the complete collapse of the financial system that was about to occur in ~4 months. But… second, they did see something coming. All the talk was tightening lending standards, credit weakening, a pullback in spending, of course housing.

It was a very different tone than the Q3 calls so far.

While banks were not hinting at the calamity brought about by Lehman, they were seeing conditions that were clearly quite tenuous.

This is a very different tone than we have right now.

There used to be this podcast that I listened to that was a great podcast. It was called Reply All. It was all about the internet and how silly and beautiful it is. It unfortunately blew up because one of the hosts got “canceled”. He was canceled because behind the scenes he was mean to other employees of the show, which was not all that surprising, since what made Reply All great was how he was mean to other employees on the show.

But alas, it is an unfortunate tale of loss that is for another time. The relevance here is that Reply All used to do this segment where their boomer podcast company owner (Alex Blumberg) presented the millennial hosts with tweets he didn’t understand and the hosts had to figure out those tweets and explain them. That segment was called Yes, Yes, No.

At some point the boomer podcast owner decided he would flip the table around and do a different segment where he, a sports enthusiast, would present sports tweets that he understood to the non-sports-enthusiast podcast hosts and explain them to the hosts. This segment was called Sports, Sports, Sports.

And that brings us to today. My new segment is called Banks, Banks, Banks.

This is the second installment. My first was on Home Capital. I didn’t want to blast out an email on that one because HCG is always such a powder keg. If you want to view the post just send me a note.

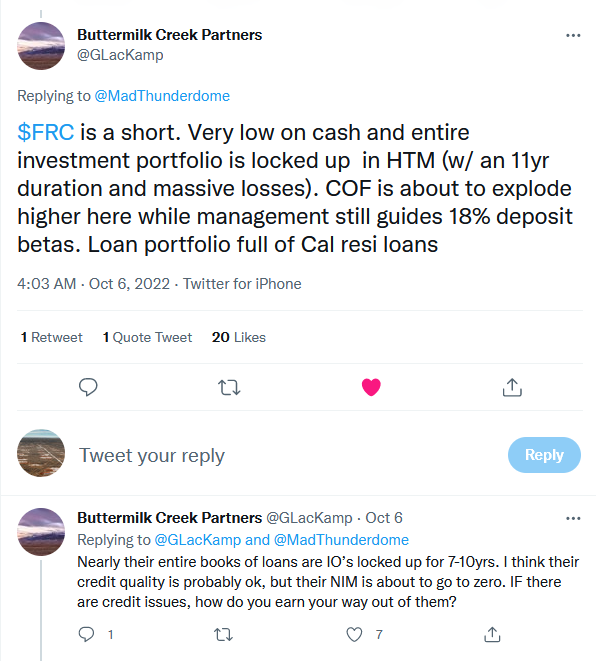

Today I will be discussing this tweet:

I found this tweet interesting because A. Buttermilk is advocating a short on a regional bank that had already been beaten up pretty darn bad and B. I didn’t know WTF he was talking about.

As it turns out, First Republic presents an interesting case. A whole pile of US banks reported on Friday (JPM, C, PNC, WFC, USB). Almost all of them had pretty good days, with most being up, which is an impressive feat considering the market as a whole was very much not up.

First Republic, however, did not do well.

Thankfully, I did not have a long position on FRC. I only sort of half-follow them. They are just one of the charts I have in my bank chart list, and I keep them there because they are a big, regional bank so I need to watch whats going on.

But then I saw the above tweet the other day, and I didn’t understand it. So I tried to figure it out.

I could spend a bunch of time going through what FRC is and does. But I won’t. Suffice to say that they are a California based bank, they pride themselves on their relationships with the households they lend to, they are known for having “pristine” credit quality, and they like to make mortgage loans. There is really not a lot going on here – its plain jane sort of stuff.

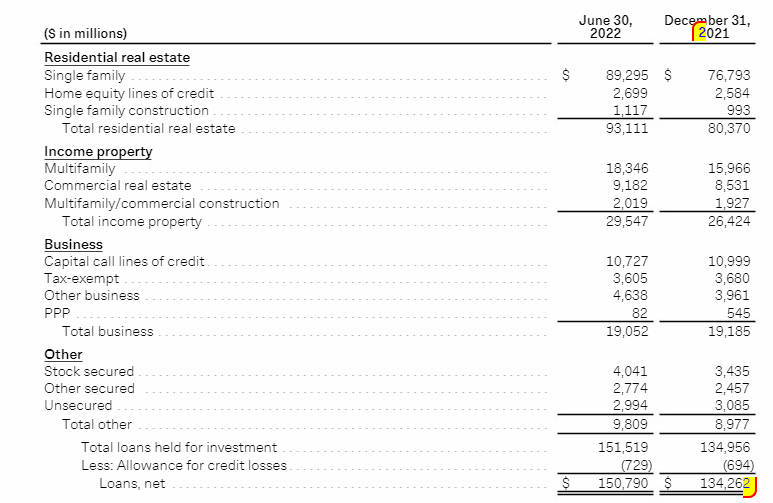

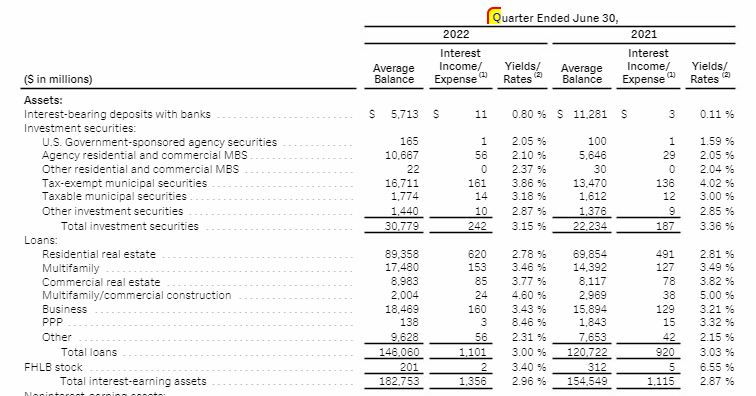

Anyway, this is First Republic’s loan book at a high level (I’m using the Q2 tables here because the 10Q wasn’t out when I looked at this but it is essentially the same for our purposes after Q3):

A couple of things about this loan book. First, its a lot of residential real estate loans. $93mm of $150mm in Q2. Second, though you can’t see it in the table, their balance sheet is pretty stuffed with loans. After Q3, they have $158b of loans and $172b of deposits. Compare that to a JP Morgan, where loans are ~50% of deposits.

Like Buttermilk says, 52% of the single family home loans are in California. Take that for what its worth. More importantly, 60% of their single family home loans are interest only loans (I/O), with a very long interest only period – they amortize to maturity after 10 years.

I honestly didn’t even know interest only loans were still a big thing in the US. Who knew?

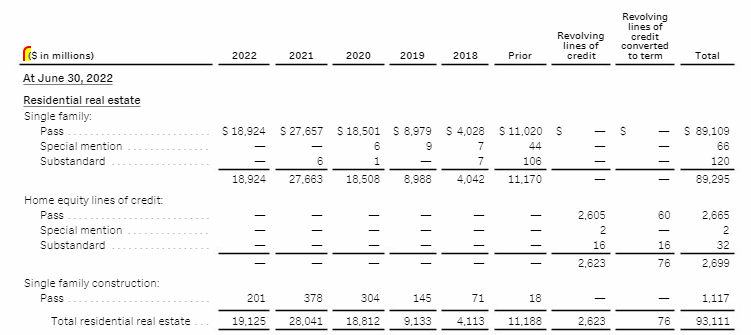

What’s more, most of these loans were made quite recently, in the last 4 years, meaning they are all still I/O and will be for a very long time:

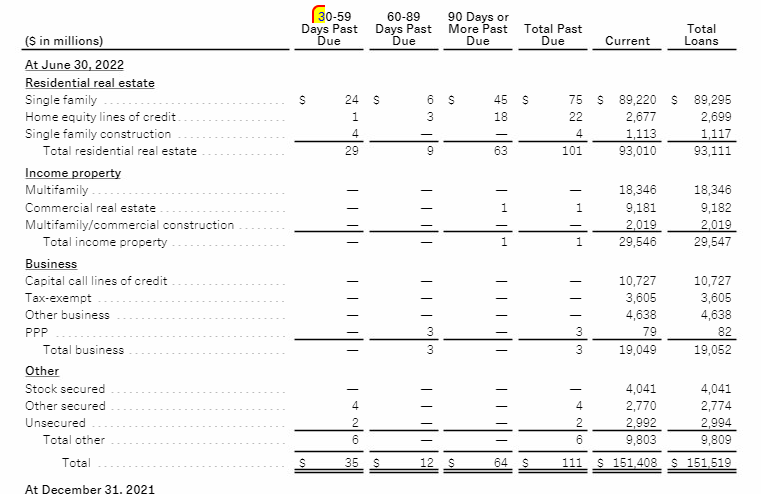

Now, to First Republic’s credit, these loans are not going bad. Very little of their SF loan book is past due.

If you compare the past due loans at the end of Q3 to the number at year end, it is actually doing better now, so its not like there is some big looming default risk here.

Instead, the risk is more on what they are going to earn from these loans.

We know that interest rates have gone up a lot. Many banks are seeing their net interest margin increase in Q3. That is why the banks that reported on Friday all did well.

When I looked at this earlier this week I was looking at First Republic’s Q2 numbers. This is what I saw:

Their residential real estate loans were actually seeing a tiny decline in yield. Now that was a bit odd because I/O loans are usually adjusted rate mortgages, or ARMs. I looked it up. But I don’t think that is the case here. They must be making fixed rate loans, or at least loans that have some sort of lag attached.

Now they do say that 23% of their loans are adjustable rate or mature in 1 year. But they don’t tell us just how much of that is adjustable and I have to assume the 23% really is skewed to the <1 year maturity because rates didn’t budge YOY on any bucket in Q2 (and only moved marginally in Q3, as you will shortly see) and if there was a sizable amount of adjustable loans those rates should be moving.

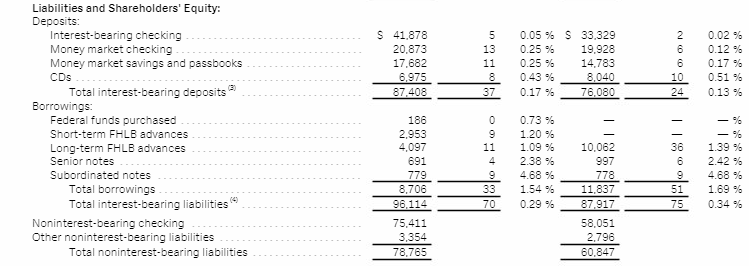

Nevertheless, in Q2 FRC was okay, because their deposit rates were quite low as well. They had hardly budged off a very low number (this is a Q2 10Q table).

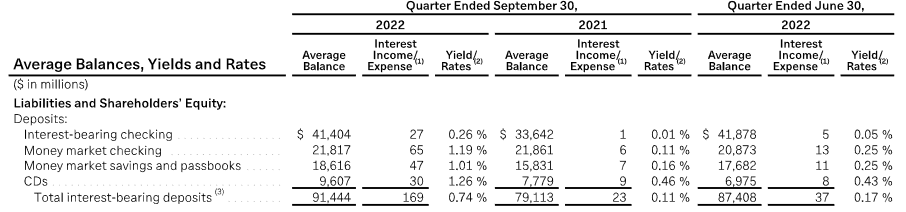

So everything was rosy. Cue the foreboding music. But, but , but… that changed in Q3. Some might call this an inflection. Here are deposit yields in Q3:

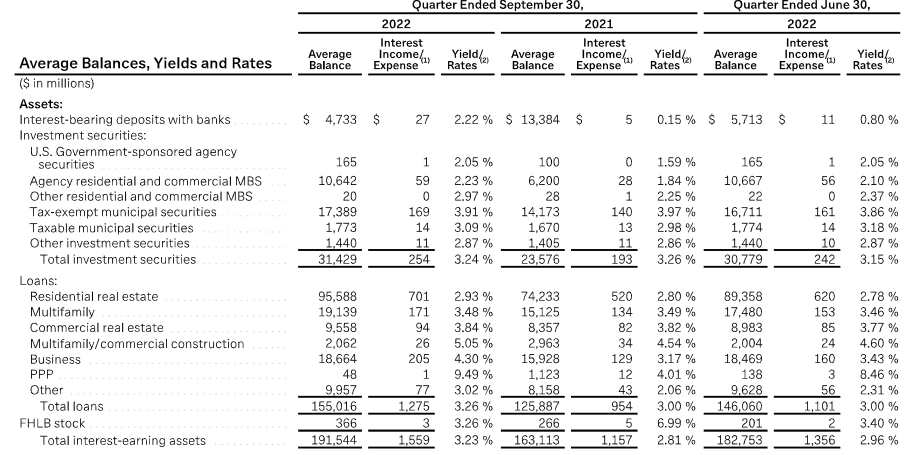

So deposits are costing more. But because their I/O loan book is not so adjustable, their loan interest did not keep up:

First Republic acknowledges they have a bit of an issue here. They guided NIM down for Q4.

In their closing remarks, they also kind of implied that things will likely get worse before it gets better:

Analysts are a little concerned. This is from another tweet, quoting the JPM analyst, who by the sounds of it has been a bull on the stock, and now appears worried about NIM:

And I think that is the story here.

Going back to the original tweet, let’s sum it up in Reply All style. We start with First Republic, a safe, plain-jane, regional bank that makes a lot of loans that people use to buy homes with. Many of these loans are long-term, interest only loans that appear to not be adjustable rate. Their loan book is also very full relative to their deposits – they have very little room to write more loans. Some investors like Buttermilk clued in that this might be a problem but until now, it wasn’t. In the third quarter it became a problem. Investors saw that First Republic needed to provide higher rates to their depositors but that they weren’t seeing a similar increase in rates from their (largely fixed rate real estate) loan book. This caused their interest margins to decline in Q3 and First Republic had to warn that these margins would likely keep going down. Everyone freaked out and sold the stock.

Last week I wrote about how my portfolio was positioned “nominally net long” but “in terms of my portfolio’s response to market moves, a little net short”. I also wrote that I thought “that a change was coming” where the bear market would end soon.

Since that time the market has gone down (it was about 3,800 then, is a little over 3,600 now) and my portfolio has not done much of anything. But my thinking has changed a little. I’m not so sure about the change, ie. not so sure that this bear market is going to end soon. But I’m not sure we have to go straight down just yet. And in the mean time, I think some stocks could go up while others go down.

This week, with a few fits and starts (I never seem to know what it is I want to do until I do a few things and realize that those are not it) I cautiously moved my positioning to being a little more net long, which I think should mean that I am actually net-net long in terms of my portfolios response to market moves. I did this even as I feel like the medium term picture is probably more bearish for the economy.

The moves I made were to take off about 20% of my index short on the S&P (the HIU), close my short on the Nasdaq, add to my position in Google, add back my position in Bank of America, add a new position in Constellation Software, add a new but so far small position in TLT, and go back to a gold names with Newmont and Barrick Gold. I also added a position in VIXY.

None of this is going to cause wild gyrations in my portfolio. If the market goes up 5%, I expect my portfolio will go up 1-2%. And (hopefully at worst) vice-versa. But I think I am more likely to participate in upside now, whereas a few weeks ago I dreaded the big up days as much (or more) than the big down days.

Ok, so why did I do what I do?

Well, I have read and listened to a lot of bearish stuff the last couple days. There are a lot of bears out there and they make a lot of good points. There is a lot to be bearish about.

If you want to hear a really bearish take, listen to this spaces, with Michael Taylor. I like listening to Michael Taylor. He is a very smart guy and well connected to the hedge fund business. As he says himself, Taylor talks primarily with 50 major hedge fund managers.

Taylor is extremely bearish, especially on the British Pound (which he says is going to blow up) but also on the stock market. Stocks aren’t seeing what bonds are seeing, he says, and if they were they would go down. I imagine most of the fund managers he talks to think the same thing.

Taylor thinks that we are going to see big redemptions from hedge funds (other hedge funds), especially around year end. He thinks the economy is going to crash (he says there is a 100% chance of this) and it is going to happen now. He thinks high yields are going to blow out, while US Treasuries are going to reverse and fly higher. It is quite dire.

Most importantly, he outlined how the carry trade is blowing up many funds. And how that has become a big headwind for the market.

As Taylor explains, it is the unwind of carry that led to the collapse of the British Pound and the eventual rescue of the UK bond market by their central bank. Taylor linked this FT article that describes the bets that went sideways for pension funds and appear to have nearly led to a collapse of these funds. This FT article, written in July, describes how pension funds have been forced to put on large carry trade bets to match their liabilities, which get larger as rates fall.

I’ve written about the carry-trade a couple of times before but not for a couple of years because when things are going well it doesn’t really matter. Knowing that it is being unwound makes me pause. Because something could blow up and this week it sounds like it almost did.

For this reason alone (and its not the only reason) I would not want to get too long of stocks right now. Taylor believes that some sort of big whooshy crash is inevitable. I’m not nearly so sure. But if there is a small probability of a whooshy crash, I want to be prepared.

For me, that is where the VIXY comes in. If something systemic is truly about to happen, the VIXY should go up a lot. Consider that it usually comes close to a double when something fairly bad happens. When something really bad happens (like COVID), it can go much higher. The trick is to buy it close to when you think a risk is there for something very bad but not so close that the bad is already priced in. When I bought it (on Monday), it wasn’t really pricing in very much risk being just a couple of points off the lows. It still isn’t.

I know any VIX ETF is a terrible instrument to hold for any length of time (see the awful chart below). But that is because it is the inverse of a carry trade, its purpose is to have sudden bursts of out-performance during times of volatility while carry-trades implode. Carry trades are essentially “short vol” trades. If they are being unwound, then the VIXY seems worth it to me as a part of my hedging routine right now. It won’t collapse overnight but it may spike overnight and if it does my hope is, in addition to my other hedges, it will put me well positioned to deal with ensuing chaos.

So that is the VIXY. What about the longs? Well Taylor’s very bearish conclusion is that the market (I’m can’t be sure if he means the GBP, the stock market or both but I think he means both) is going to go down hard. Though he had covered his entire short position after the BOE pivot, after listening to his own talk, Taylor went max short again and made big money again today (though fortunately not the GBP, which was up big today).

I am not so nimble, so I will not being going max short or long of anything at any point. Instead I will just try to eek out a few gains in both up and down markets.

This is clearly been a down market. Yet (apart from my VIXY crash protection) I’m moving my position to being more bullish. Why?

Funnily enough, it is because of what Taylor says.

Taylor is very long US Treasuries. He says on a few occasions he is long $100 million of 10-year treasuries! I am not long $100 million of 10 year treasuries. But I took a small position in TLT.

I have been scratching my head the last couple weeks about why the bond market keeps falling, ie. rates keep going up. How can this be happening when just about anyone can see that things are slowing, maybe dramatically.

Taylor explained this conundrum. Its the carry-trade! The unwind of the carry-trades in the UK has been causing funds to liquidate UK bonds. I can only presume that the same thing is happening in North America and elsewhere. Bonds that were either on the other side of the trade or being used as collateral for the other side are being sold, and it has nothing to do with rate expectations.

If this is why bonds are falling, it will end. So I followed Taylor, who has been long treasuries for at least a little while, and took my own position in the TLT, which has done very badly this year.

Taylor thinks that the market is going to tank and that government bonds are going to become the “only-one-to-own risk-free asset” again. On this point, I am kind of in agreement, but only up to a point with that point being treasuries and not tank. The market has gone down quite far, quite fast over the last month, sentiment is very bad, and it doesn’t seem to me or the transcripts I read that the US economy is doing all that badly just yet. So I’m not sure I’m onboard with the whole tank side, at least for now.

Absent a systemic catalyst that is. Which could happen. And I can’t predict it. So I’ll keep tight with the hedges and VIXY for the moment.

In my post last week I basically said I was out of the small-cap stuff and in with boring larger cap names like Verizon, Vertex, Google and Pfizer. But I wasn’t entirely sure why.

I think I know now. I think that if Taylor is right and longer term interest rates are going to peak and begin to fall, big cap names are going to outperform.

Rates will be falling because the economy is weakening. But there won’t be an expectation that the Fed will come to the rescue and save everyone. All those crappy, money losing stocks that, as Taylor says, “need the HYG” (the one’s I tend to be short) are going to have trouble. But falling rates are going will provide some positives for more established stocks, both because they mean we aren’t going into an inflationary spiral, that there will be a chance of a soft(er) landing, that bonds aren’t in competition to dividends (ala Verizon or Pfizer) and that lower discount rates translate into higher multiples.

Meanwhile a stock like Bank of America has a PE of 9.5x. Pfizer has a PE of 6.8x. Google has a PE of 17x. Constellation is more expensive, at 23x next years earnings, but it has a 5% FCF yield and grows at ~20%.

I understand that if things deteriorate enough, all of these P’s and E’s can go down more. But if rates are coming down, it will be a signal that an end of tightening is in sight (it worked!), and so just how far should the PEs of the best companies be compressed?

That same argument is why I decided to take down my S&P index short (which is weighted towards the big cap names) and not my Russell or single name shorts. Again, “short the companies that need the HYG”.

I want to keep my exposure to being short crappy stuff but get a little long the not-so-crappy stuff.

Meanwhile, there is SO MUCH negativity out there. While I am not the sort to take sentiment indicators all that seriously, sentiment certainly seems overtly bad right now. It makes me more nervous about my shorts being too large than my longs. I can imagine a scenario where something, anything, good happens, the Canadian dollar rips off of extremely oversold lows, the market rips off of its extremely oversold low, and I am left getting smacked by a big up day.

My feeling is that a big up day is the bigger risk right now than a big down day. And with a big down day I always have that VIXY backstop. Besides we’ve had a month of big down days. The Nasdaq is down ~20% from where it was mid-August. Bonds have been in a straight line down. Non-USD currencies have been in a straight-line down. After such extreme moves it is usually not prudent to press while it is usually prudent to rebalance. So that’s what I am doing.