Week 111 Portfolio Update: When Things Aren’t Working…

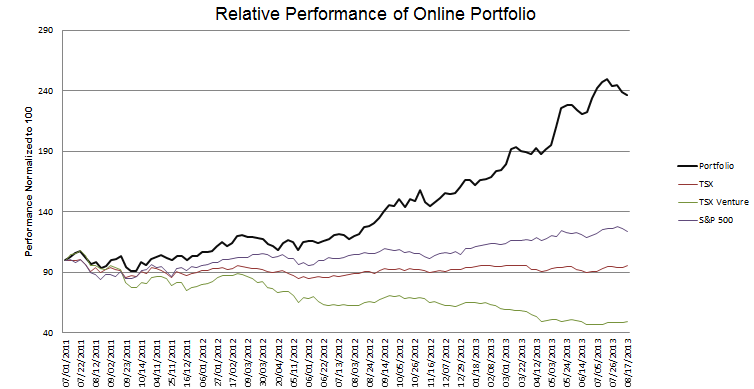

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Shake-up

In a previous post about Walker & Dunlop I described the consequence of being on vacation while the company announced poor results, which was that I was not able to take advantage of a clear selling situation. The same was the case for Dex Media.

In the past I used the term “good enough investing” to describe what I’m trying to do with my portfolio. I work a full time job, have a life and need a break now and then, and all that means I just can’t be on top of everything. I try my best but I have found it necessary to employ techniques to mitigate this. In particular, I sell stocks when things aren’t working out.

While I’ve had my share of winners over the past month and a half (AIQ, NVS, NCT, NRF, IQNT to name a few), I’ve also had my share of losers (NKO, EXE, VTNC, and the above mentioned duo) with the result being that my portfolio has done not much of anything. While I remain hopeful that both Niko Resources and Extendicare eventually pan out, the fact is that thus far they haven’t. Read more