Week 55: Skittish

Portfolio Performance

Portfolio Composition

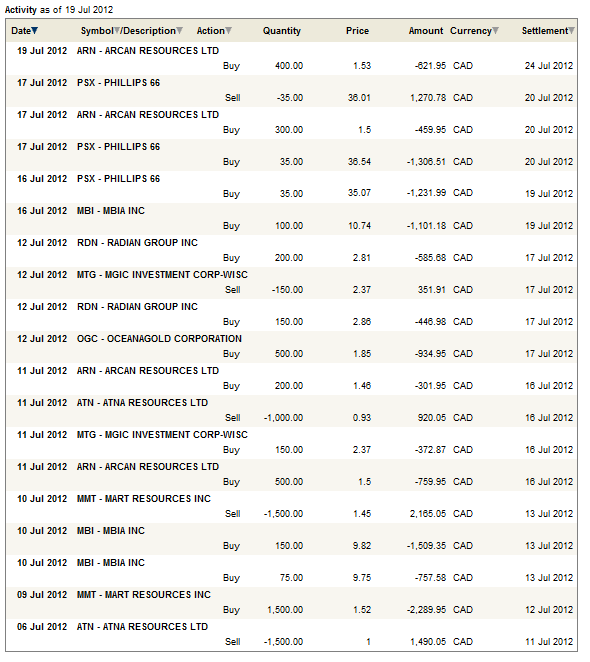

Click here for last two weeks of trades.

Portfolio Summary

I have reluctantly added some risk over the last couple of weeks My cash position is down to $27,839 from $35,893 two weeks ago, which is a drop to 23% of total assets in my tracking portfolio.

The stocks I have bought have been added because I believe they are cheap. I think that there is a reasonable chance that they will be worth significantly more over time. But I do not add them with complete conviction.

The problem remains Europe. And I remain wary of when the next shoe will drop. Until Friday, the market had forgotten about Europe for the time being, but we have seen this happen before, and always with the same ending. Europe comes back and again trumps all else. With Spanish yields rising to a new high on Friday (7.267%) I am already questioning whether I have made a mistake by purchasing rather than selling stock. I have already considered an about face.

You can see just how skittish I am by looking at how many trades I am second guessing myself on. Three times in the last two weeks I bought a position only to sell it later the same day. These weren’t planned “trades”. I don’t play the day-trade game. These were cases where I took the position and couldn’t handle the weight of it, and decided to sell instead of worrying about whether I had made a mistake by buying.

I am typically not so wishy-washy. That the market has me going through convulsions speaks volumes to the uncertainty that exists at the moment.

As for the stocks I bought, those that I kept that is, I am confident that I got them at a decent price which, in the absence of more macro-malaise, will lead to eventual profits. More on the individual position updates in the post below:

Company Updates

Radian Group (RDN), MGIC (MTG), MBIA (MBI): here

Arcan Resources (ARN): here

Phillips 66 (PSX): here

{kind=link}