Research: Big 5 Sporting Goods

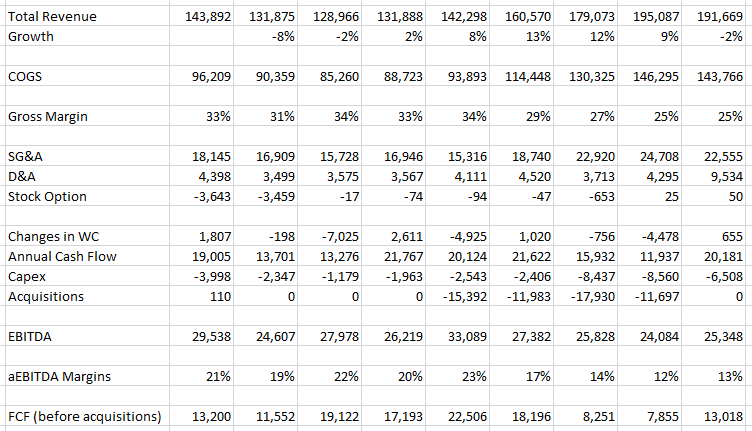

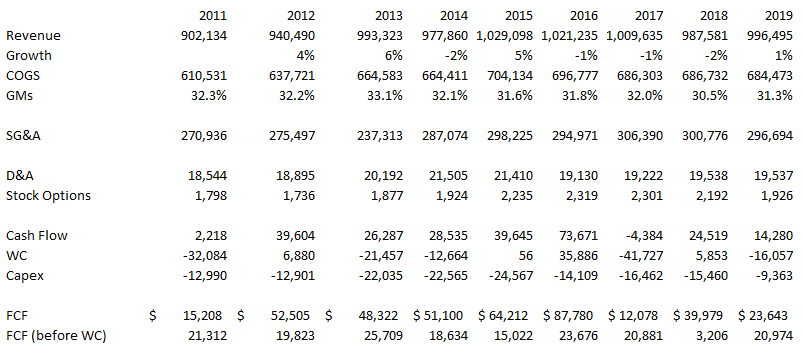

I have been surprised that Big 5 has not performed better. One reasonable bear case I can think of is that this year will be a flash in the pan. I looked back at the historical results to see how Big 5 has performed over the last 10 years.

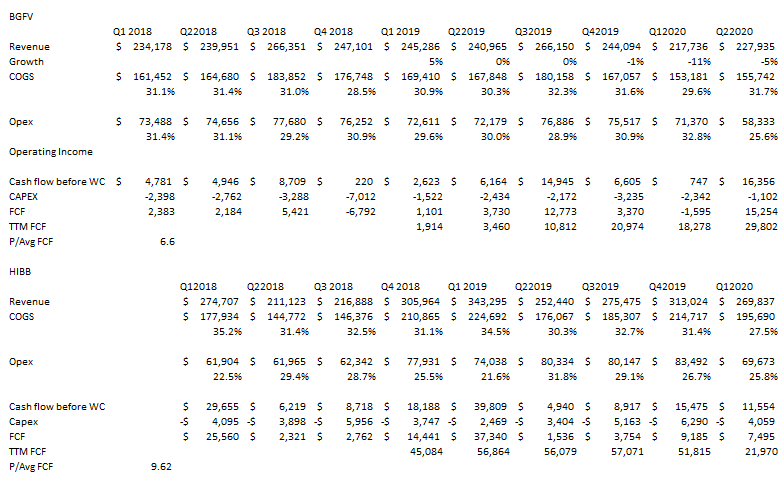

Highlights from Q2:

Highlights from Q2:

Q220 result highlights:

- SSS increased 31.9% in July

- at end of July had no debt and $38mm cash position

- in Q220 they had SSS decrease 4.2% yoy

- in second half of Q2 SSS increased 15.5%

- they had much higher GMs, up to 31.7% from 30.3% yoy – due to product mix favoring high margin categories, less promotional activity

- also they have reduced costs, and reduced warehousing

- SG&A was lower because of “lower employee labor expense reflecting reduced store operating hours and lower advertising expense during the period”

- they are guiding for 5% to 15% SSS increase through the rest of Q320 – would mean 14% to 20% SSS for Q3 as a whole

- EPS for the quarter would be $1-$1.30 per share

- still have 431 stores in operation

- they had opened all closed stores by May

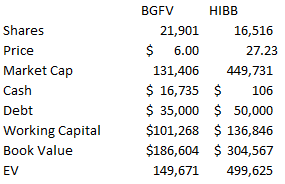

HIBB Comp: