New Position in Cherry Hill Mortgage (CHMI)

I was going to put this in my update post but its gotten a little long so I thought I’d pop it out on its own. I’ve talked a lot about New Residential and how much I like mortgage servicing rights as a play on a stronger economy and on rising rates. Well a few weeks ago a fellow who follows the blog wrote me about Cherry Hill Mortgage, a company that, like New Residential, is a REIT that holds mortgage servicing rights. It took me a few weeks to find the time to look at the company and another week afterthat for it to really sink in just how cheap it was comparatively. But once it did I felt compelled to take a position.

It was a bit of unfortunate timing; I had to sell about 25% of my (albeit unreasonably large) position in New Residential to fund the purchase. I wasn’t comfortable going on margin to fund the purchase. So I took that New Residential position down from 20% to 15%. Of course the day after I sold New Res at $6 the stock popped to $6.30. Maybe my sacrifice to the gods of trading was appreciated.

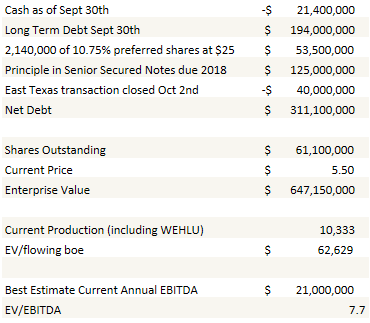

Nevertheless, in the long run I hope to be well compensated for my position in Cherry Hill. Cherry Hill is being spun out of the mortgage originator Freedom Mortgage. Soon after the IPO, the company purchased two pools of mortgage servicing rights from Freedom Mortgage. I ran some quick numbers and it looks like the company paid a reasonable price for these assets. In the table below the assets have been valued at cost: Read more