Q1 Earnings: Radisys

Radisys stock has been pretty flat since it announced its first quarter results, and while I can understand that lack of interest, I nevertheless was pleased with what I heard on the call.

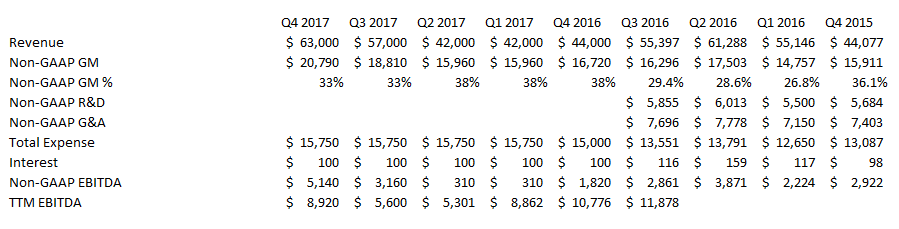

The first quarter was on the low end of guidance. Revenue came in at $37.6 million, while the company had anticipated a range of $37-$41 million. Guidance for the second quarter was $41-$47 million, which is pretty close to my expectation, though maybe the top end is a couple million higher.

The stock didn’t move on any of this and it shouldn’t have. There is nothing surprising. The Radisys story continues to be a wait and see one. We wait for announcements of new DCEngine, FlowEngine, and MediaEngine orders and we’ll see if they materialize.

There was lots of qualitative progress on this front but not much quantitative in the way of meaningful orders yet.

Here are the highlights:

Verizon announced their Exponent platform in February. The platform allows carriers to deploy off-the-shelf(ish) next-gen solutions using technology Verizon has developed. Brian Bronson (CEO) said that DCEngine and FlowEngine are designed into the Exponent solutions and that they have seen incremental customer relations develop. While this is very new and the relationships are mostly still in the early stages, Bronson did say that “a couple of engagements are fairly close”.

A second partnership was announced with Nokia. This one revolves around MediaEngine and to me seems very significant. Nokia will be marketing MediaEngine as their single MRF solution. The Alcatel-Lucent MRF will be mothballed in favor of the Radisys product. The partnership is expected to open access to new CSP customers. They expect that given Nokia’s customer base, MediaEngine will be the MRF in 3 of the 4 CSPs in North America, and that there are opportunities in Asia/India as well (beyond Reliance). In the past there were a number of MediaEngine deals where MediaEngine saw a half share win (with the Alcatel-Lucent MRF picking up the other half) but will now have the full deal go to MediaEngine.

They are close to closing 3 new carrier wins with DCEngine. First, they are pretty close to signing a master agreement with a US Tier 1 CSP. They said this wasn’t Verizon (already the primary DCEngine customer) so I think it has to be AT&T (??). They were confident enough to say that they expect purchase orders this quarter from this operator.

Second, Reliance Jio is trialing DCEngine for a single use case and they expect orders with respect to this use case in the second half. Third, a South East Asian CSP has received proof of concept DCEngine units to in the first quarter for a use case that has a revenue potential of around $20 million.

They formally announced the new FlowEngine, called TDE-2000, in the first quarter. Management provided color around a strong response and the initiation of trials and proof of concepts but nothing specific. They did say that Verizon is using the older version of FlowEngine for a new packet-inspection use case (they have used it in the past as a edge-router) and that they expect “incremental deployments in the second half” for this use case. Bronson also said that by year end he expects that at least one of the DCEngine wins will incorporate FlowEngine.

With MediaEngine, the big news is the Nokia partnership that I already mentioned, but there also appears to be some progress around transcoding. They are still looking “to disrupt transcoding”. I talked about how MediaEngine provides an alternative to session border controllers (SBC) to perform transcoding operations in this post (there is also a good youtube video on how MediaEngine can save money on transcoding) The punchline is that Radisys can offer a solution that is 3x to 5x cheaper. On the call they disclosed that MediaEngine is already deployed to a small extent performing the transcoding function with a couple of operators, which is new information. They also have a new “in” with operators, as they can leverage the Nokia-ALU relationship. Nokia-ALU is the number two SBC provider in the world. Bronson said there are a couple of operators that have “strong interest” and that they are looking to a 7-figure deal.

So is it good or bad?

You can look at this one of two ways, You can optimistically count up all the engagements, trials, proof of concepts and agreements on the verge of being signed and think that the second half of 2017 and 2018 are going to be a great ramp. Or you can pessimistically point out that nothing has been signed yet, there is still very little incremental revenue beyond Verizon, Reliance Jio and some piecemeal one-offs and that the clock continues to tick.

Both of these perspectives seem perfectly valid. I prefer to take the first, mainly because I believe the upside in the stock is significant if it turns out to be right.