Week 82: Lots of Flux

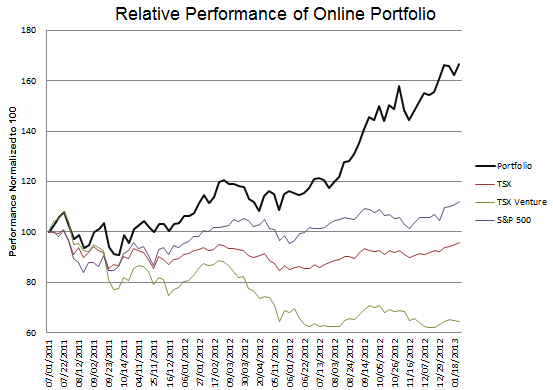

Portfolio Performance

Short Lived Niko Experience

I wrote about a new position in Niko in a short summary 3 weeks ago. A couple weeks later I sold the stock. What can I say – its part of my process. A lot of times I only get clarity about a stock once I own it. I buy a position, sit on it for a few days or a week, and do some more background and some more thinking on the name. With that my opinion becomes more clear.

The discomfort I developed with Niko was partially the result of another batch of less than stellar drilling results, but mostly the result of my conclusion that this isn’t the right time yet. The driver of the share price will be the settlement of a new gas price contract in India. I don’t think this is likely to occur until the existing contract expires, which is not until next year. In the mean time Niko will continue to experience production declines in India, and they are open to negative news flow on drilling.

Of course you could argue they are also open to positive news flow, and that’s totally true. But the point is, its a gamble. If they report a hit then I will miss out (though I suspect that such news might get me to jump back in). Absent that, I’m going to keep watching Niko until we get closer to year-end and to where the market can begin to price in a new contract.

Into Tricon Capital

I’m working on a full post of my thoughts on Tricon Capital (TCN.to) so I will only make some limited comments here. I learned about the stock from a friend over a month ago and watched it run up from $6 to $6.75 before finally taking a piece. Its a tricky stock to evaluate, having both an asset management business in addition to the on-balance sheet residential housing that drew my interest. It isn’t so much an intrinsic value story as it is an event-driven one – if the company can continue to purchase blocks of homes cheaply and build their portfolio, so should the stock move higher. Management has shown its ability to do that with the recent purchase of properties in Charlotte North Carolina for what appears to be quite a cheap price. I’ll write more about the name shortly.

Into American Axle & Manufacturing

I got the idea for American Axle & Manufacturing (AXL) from another friend about a month ago. He presented the stock as a housing play. Axle is an auto-parts supplier, mainly drive train systems and related parts, with about 60% of the product they make going to GM. Almost all of their work is done for light trucks so the idea here is that as housing picks up, so will the demand for trucks and that is going to help American Axle.

American Axle has had some struggles over the last couple of quarters with the launch of some of their backlog, but it appears to me that the problems they have encountered are nothing they can’t fix, and that there is a clear ramp of new launches over the next couple quarters that should lead to pretty decent free cash flow by the end of this year.

I’m trying to move away from some of the early stage housing plays, like the mortgage originators and servicers, and into names that will benefit from a cycle of new home building. While the obvious candidates there are the lumber and home building companies, I think that some peripheral names, like American Axle, could do quite well.

Trading Alon Energy Partners for Northern Tier at just the wrong time

Was this ever a case of bad timing. I traded out my position in Alon Energy Partners (ALDW) for Northern Tier Energy (NTI) last Tuesday. That proved to be just about the low point for Alon, while Northern Tier moved only marginally from where I bought it. Taking a look at spreads, it looks like I timed the retracement of the Midlands-WTI spread rather poorly.

Over the medium term I think I did the right thing. Based on the reading I’ve done there is a significant amount of pipeline capacity being added over the next year, both between Cushing and Seaway and between Midlands and Cushing. Texas is a pretty open place for investment, which minimizes the chances of hold-ups.

Northern Tier Energy, whose primary asset is a refinery in St. Paul, derives its spread primarily from the Bakken and Canadian crude. They can take about 20% Western Canada Select which is trading at a massive $30 spread. Given the regulatory environment here in Canada I think there is a better chance that Northern Tier receives wide spreads for longer than Alon Energy Partners does. But we shall see. I am more than aware that this is probably a short-term phenomenon that won’t last forever. Therefore I am keeping my position in Northern Tier reasonably small so that I can get out quickly when the cycle turns.

Taking some off PHH

I already wrote a piece about my thoughts on gain on sale margins and taking a little PHH off the table. I decided today (Monday) to get rid of the rest. I wrote the following to a friend today who asked me about my decision:

I just have too much gain-on-sale exposure. I have Impac Mortgage, which is an origination play, and a number of the banks I own have gain on sale risk to varying degrees (RBNF, FMAR, MNRK, and PVFC). PHH is sensitive to the risk of shrinking margins because its on the streets radar.

I think at the end of the day we settle to a higher than historic level on gain on sale, and that purchase mortgages take up some of the refinancing slack. But getting from here to there worries me. I don’t want to take that risk right now when I have done well on the stock and recognize there are headwinds.

Keep in mind though I got spooked out of NSM at the wrong time so my record on when to sell these mortgage names is not stellar. I think I am more compelled to take profits on some of these stocks because they have moved so much for me since my price point and I am seeing them from that angle rather than from remaining upside.

Selling AIG, Nexen, Phillips 66, Nationstar Mortgage, Mart Resources

To some degree the reason behind the sale of each of these stocks was that I am getting too many names in my portfolio and its time to trim them down. But these are also stocks of which I have low conviction.

In the case of Nationstar and Phillips 66 I have made good money on both, 40% return on Phillips 66 and almost a triple on Nationstar (though in full disclosure I sold most of my position in Nationstar at $25, for about a double), and it feels like the time to take gains.

Nexen has played itself out and I made a bucks on the stock. AIG is a stock i need to do the work on, and I haven’t done that work yet, and I simply have a lot of names I’m looking at right now and I’d rather not be stuck in the position of owning something that I really don’t understand that well.

Mart was sold strictly on concerns about the problems in Mali, which have recently spread to Algeria. I realize Algeria is in the opposite direction as Nigeria, but I don’t like the rising conflict. Nigeria is not that far away from Mali, and I simply don’t have to take the risk. There are many other opportunities right now.

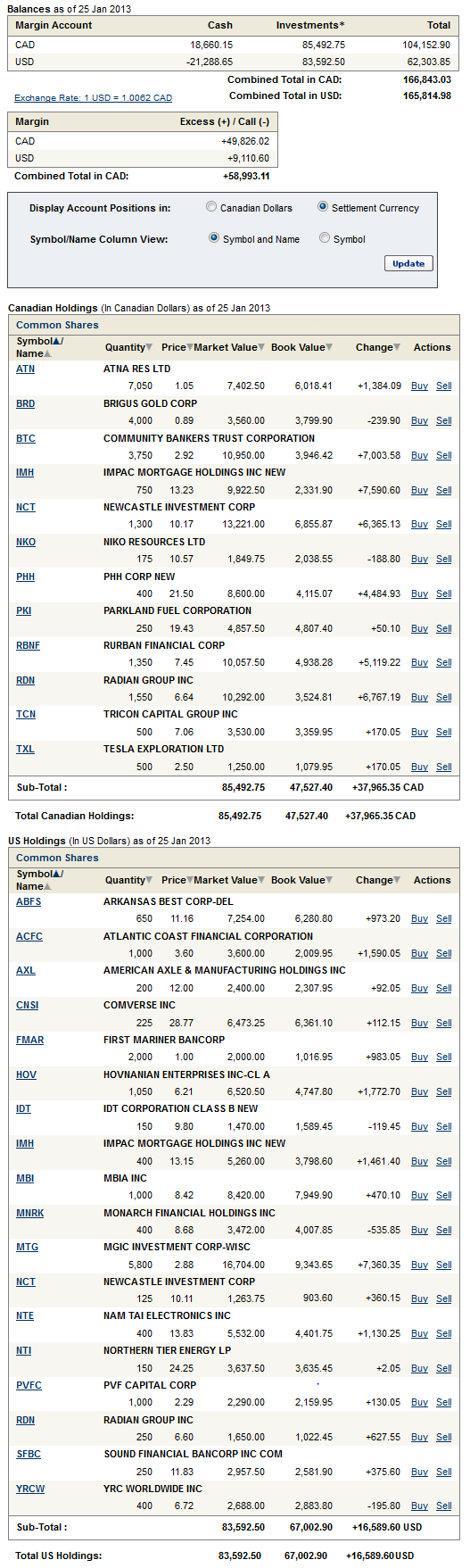

Portfolio Composition

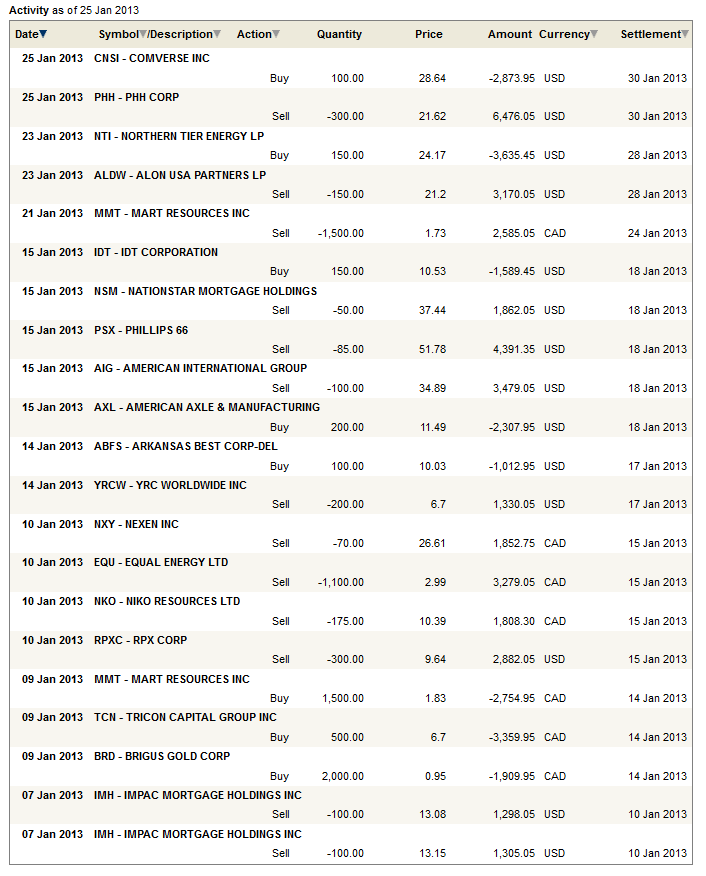

Click here for the past three weeks of trades.

{kind=link}

I noted your comment on your intention to lighten up on early housing plays such as mortgage servicers. However, NCT in my opinion may have a ways to run up yet, along with Nationstar, as the big banks will take another 18 months to 2 years to completely unload their servicing portfolios. Fortress Investments has developed some synergies between these two companies that will continue to benefit shareholders in the near term (12 – 18 months). Bank of America, for example, still has a significant amount of servicing rights to unload, and this will likely continue to benefit both NCT (or spinoff) and NSM with increased earnings and higher share prices. Your thoughts? Nelson