Week 107: Back to Commodities

It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that – Warren Buffett

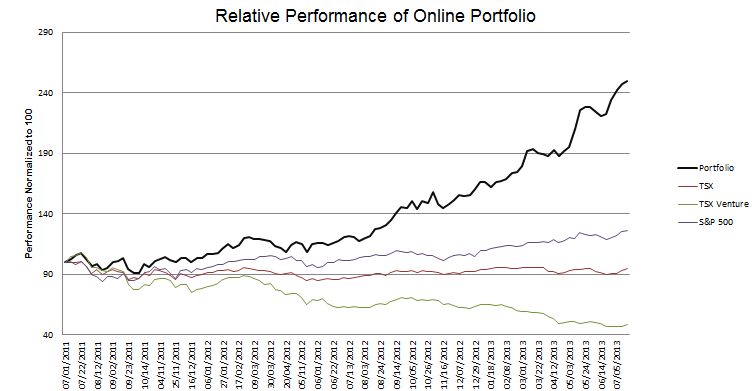

I’m adding a simple year by year and quarterly performance table to the start of every portfolio update. I’ve had the on-line portfolio going for over 2 years now, and I find that the chart is less informative the longer the time horizon gets. The quote, which I have mentioned before, is more of a goal than a statement. Buffett says it’s possible, let’s try to prove him right.

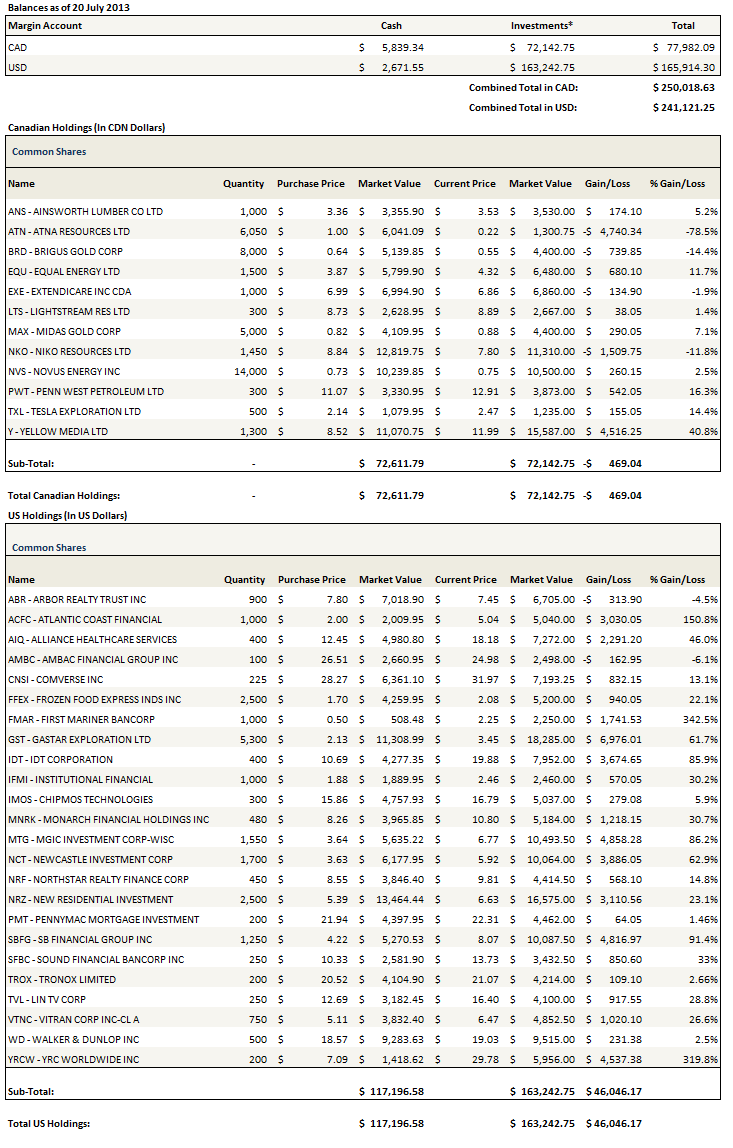

I’ve already written about most of the new stocks that I added in the last month (Ainsworth Lumber, Tronox, Novus Energy,smaller positions in Lightstream Resources and Penn West, and lastly Niko Resources. In this post I will focus on some of the stocks I sold (including most of my large position in YRC Worldwide), and add some thoughts on oil and Canadian oil juniors.

I’m getting this update out a day late so all of the numbers are are of Friday July 19th.

Portfolio Performance

Portfolio Composition

The last four weeks of trades are available here.

The last four weeks of trades are available here.

I love being back in Oils

I’m really happy to be getting back invested in some Canadian oil companies. This is the sector I work in, I find it interesting to study and I like to think I have a bit more insight here than I do in other sectors.

I already took a post to write about my position in Niko Resources, and another to describe how I came to invest in Novus Energy, while taking smaller positions in Penn West and Lightstream along the way. I won’t belabor the points made again here.

I watched a good BNN interview with Eric Nuttall last Thursday where he described what he thought has happened with Canadian oil and gas companies. He should know, he’s gotten pretty shellacked over the last year and a half. Anyways Nuttall pointed to the boom/bust cycle that began in 2010 and continued into 2011 until things got out of hand to the upside when investors got overly excited about the application of horizontal multifrac technology (without perhaps realizing that this is still oil and oil is not terribly easy to get out of the ground period) and bid up junior and intermediate light oil and condensate producers to levels that were, in retrospect, far too high. Since then we have seen those positions unwind as the companies have fallen victim to high debt levels (because these wells are very expensive to drill and capital was too readily available), in many cases production that has lagged expectations and lower than anticipated oil prices in Canada because of transportation bottlenecks.

Nuttall makes the following points arguing that this trend has run its course:

- The differential between WTI and Edmonton Light Sweet (the proxy for what most Canadian producers are getting) has narrowed to a couple bucks and with the fall of the Canadian dollar, producers are actually reaping a price that is on par with their American counterparts

- Much of the outflows from the sector had more to do with “fast money” leaving and less to do with the actual productivity of the companies. The depression in price isn’t justified by the fundamentals.

- There is evidence that American investors, who were the primary cause of the outflows, are beginning to make their way back into the sector.

I am well aware that this is a sector full of pitfalls, that managements are often not after shareholder interests, that the companies can get even cheaper (anyone who remembers the early 2000’s would attest to that) and that the long-term projections and net asset value estimates should be taken with a grain of salt (because realistically no oil company is going to run out its assets in the manner that these calculations suggest, so what reality are they modeling?). Still, I think that the sell-off is overdone given the fundamentals, and the assets that at least some of the junior and intermediate producers have are worth more than the market is valuing them at. I am actively looking for other Canadian oil based juniors.

Has to be oil though, my thoughts on Canadian natural gas are far less constructive. I also think there is an element here that is much like the REIT sell-off that I took advantage of a few weeks ago; that oil is being lumped in with “commodities” in a sell-off that has not discriminated. If a discerning investor can recognize that some commodities are equally tied to US (and Japanese?) growth and not dependent on either money printing (ie. gold) or a Chinese resurgence (ie. Base Metals), there could be money to be made. So those are the reasons behind the bets so far, and maybe a few more in the near future.

Out of Nexstar and Inteliquent

Both of these stocks have been winners for me, and while the companies are quite different, both exemplify how the strategy of buying companies trading at low EBITDA multiples that translate to free cash is generally a profitable endeavor.

Unfortunately, both stocks also exemplify the trouble with selling anything in a bull market. While I have done well, and both had come close to the target of what I had hoped to get from them eventually at the time I sold, within the next week each was trading higher, in Inteliquent’s case significantly so. I am reminded of the phrase of old Partridge in Reminiscences of a Stock Operator, “it’s a bull market!”. Justification to hold onto as much stock of good companies as you can while the good times last. Eventually they will turn for the worse, but there is no sense in anticipating that, at least not when you are an individual investor that can unload positions in a day.

Significant Reduction to YRC Worldwide

While I haven’t sold out of my position in YRC Worldwide entirely, I have reduced my position considerably. Its actually down even more in my actual portfolios than in the practice one, to about 1.5% position.

The reason? I’m not certain what earnings are going to look like over the next few quarters, and at $30+ per share the downside is considerably more than it was in single digits.

YRC Worldwide has been a great stock. A 5-bagger in less than 6 months. Its been a huge contributor to my performance and the biggest single reason that I am up 100% in the last year. But it reminds me of a comment I heard on twitter a few weeks ago: Don’t get caught up in thesis creep.

The idea behind YRC Worldwide all along was that the company wasn’t going bankrupt, and if it wasn’t going bankrupt the shares were going to trade at a price that reflected it wasn’t going bankrupt. It was a good thesis, but its done. The shares are a long ways away from having nothing but ‘imminent Chapter 11″ priced in.

To hold on to YRC Worldwide at these prices you have to have a view on earnings. I don’t have a strong view, at least not one that justifies the $30 price tag. I have found that at inflections, like what YRCW is at, its really difficult to predict quarterly changes in earnings; there always turns out to be a surprise, sometimes positive, sometimes negative. It could go either way and I don’t know which way it will go. I had a strong opinion that the company wasn’t going bankrupt. I have far less of an opinion on whether the company can earn $2, $3, or $4 per share when its all said and done. At $30, you have to have a view on this to be in the stock. So I’m out. Mostly.

One more REIT play

I wrote about my earlier REIT purchases in my post Taking Advantage of the REIT Sell-off. In the days subsequent to the post I added back a position in one more REIT, a company I had owned just a month prior, Newcastle Investment. I sold Newcastle after the spin-off because my interest in the company has always been the MSR business, and that business was transferred into New Residential. However, after listening to the conference call, reading through the slides, and noting that the stock was down 12% from where I took my position off, I changed my mind.

What enticed me to get back into Newcastle was, of course, the sell-off, but also the simplicity of the business plan. The company has legacy CDO’s that, over the next few years, will unwind or that Newcastle can collapse. This will result in about $750-$800 million net to the company. As long as the economy doesn’t tank there is an excellent chance they will realize this cash one way or another. The cash does nothing to the company’s book value, but it does give them an uninvested stash to put to good use.

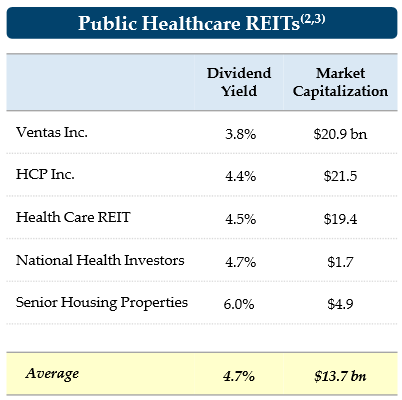

They plan to put that cash to use by buying senior housing. The returns that they are expecting on their senior housing investments are similar, if not a bit better, to those that they are getting on their CDO’s. They expect unlevered returns of 9.4% and levered returns of 17.6%. But the real benefit will be incurred by the markets perception of the sustainability of that dividend. Newcastle provided the following table of dividend yields for publicly traded healthcare REITs.

The average yield on healthcare REITs is half the yield paid by Newcastle right now. And there appear to be plenty of opportunities in the sector. The company has identified $300 million in a near term pipeline.

So its pretty simple right? Collapse existing assets, take the cash and invest them in assets that the market values more highly. Maybe that’s a little simplistic, but at $5 it certainly seemed worth a plunge. Here at a little less than $6 I’m less sure, but I’m willing to stick it out and see how this plays out over the next few quarters.

Housekeeping

I was on vacation when I wrote my June update and when I was compiling my portfolio statistics into my spreadsheet I missed 3 trades that happened on May 28th. Because I was on vacation I didn’t make my usual comparison between the spreadsheet and the RBC practice portfolio and so I didn’t catch these errors until I was making that comparison this time around. The three trades were for 100 shares of Alliance Healthcare Services, 400 shares of new Residential, and 3,000 shares of Brigus Gold. With these changes everything is back to being the same as the RBC practice portfolio.

If you look at my trades over the last month you will notice that PennyMac was added on July 17th at a price of $22. This is at odds with my post from the beginning of July where I had talked about buying PennyMac back in June. This is because, while I added the stock to all the actual portfolios I manage, I forgot to add it to the practice portfolio I track here. This happens from time to time; the lack of actual money at risk tends to make me more forgetful at times. It’s in there now, at a somewhat higher cost basis.

{kind=link}

Mr. Sigurd,

It seems to me that Newcastle is operating much like a hedge fund play, where NCT is buying distressed assets at a discount, then spinning them off to realize value (see the spinoff of NRZ). This is now occurring with the publishing assets (New Media spinoff). Yes NCT still has the senior housing play, but seems willing to seize an opportunity in any distressed asset that offers a great ROI. I plan to keep this investment over the near term both for the latest spinoff of the publishing assets (to realize the true value after a nice dividend return has been established), and to get a piece of the Fortress Investment Group action, when they find another distressed asset(s) to purchase and potentially spin off. As NCT sells or collapses the CDO’s, this process will also provide some funding for opportunistic acquisitions.

The 70 cent annual dividend from NRZ shows me that the executives of NCT (Ken Riis, and Randy Nardone, also partners in Fortress) typically under promise (the base case investment return) and over deliver with dividends in excess of those depicted in the base case.

Your thoughts?

Sorry for the slow reply. I agree with everything you said. My position in NCT has always been based on them finding interesting investments that I can’t always predict ahead of time. I really like this newspaper business idea, and will be very interested when the spin-out is complete.