Week 127: A couple of new stocks and getting rid of a few others (JONE, MHR, PXL.CA, DGIT, TROX)

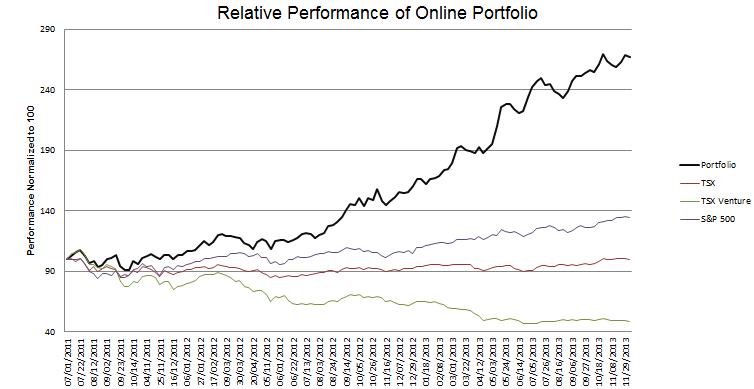

Portfolio Performance

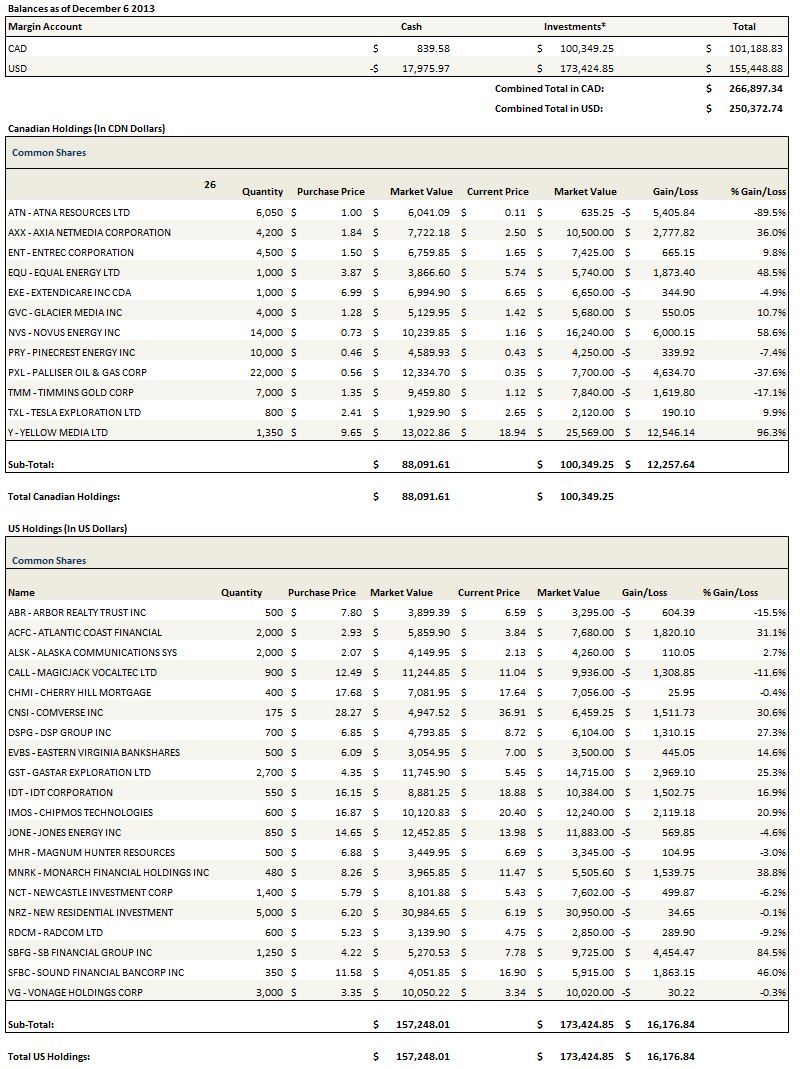

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I don’t have a lot to say about the macro picture or generalized musings about my portfolio this month. The macro continues to be a party-on atmosphere so I guess we’ll keep dancing. My portfolio is still not performing as well as I would like but I don’t have any insights into why that is or what I should do different. I had a very good first seven months of the year, and now I am having a lull. These things ebb and flow. Onto the stocks.

Adding Jones Energy (JONE)

I really like this stock. It’s a recent IPO (it went public at the beginning of August), I don’t think it’s well covered or known by many, but it looks to me like they have been drilling extremely profitable gas-condensate wells in the mid-continent, and they have plenty of undeveloped acreage to drill more. I took a big position in it right off the bat at 6%.

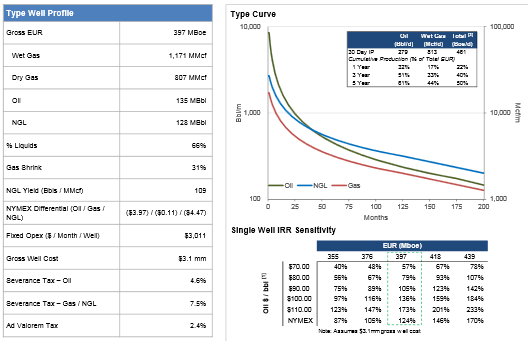

The company operates in two formations, the Cleveland and the Woodford. Of the two, the Cleveland is more interesting to me. Cleveland wells produce about 400 mboe, with about 65% liquid content split fairly evenly between oil and NGLs. What makes the formation so interesting is how cheap these wells are to drill. Jones is drilling wells in the Cleveland for $3.1 million. The combination of the high EUR’s and the low costs means that the IRR on the wells exceeds 100% at $90 oil. And this isn’t a Gastar type play, where a couple of dozen wells are being extrapolated over a vast area and it remains to be seen if the analogy holds. Jones has 293 gross wells in the Cleveland. There are another 521 locations on tap. I may write this one up in more detail in the coming weeks but to be honest, its such a stupid simple idea I don’t know if there is that much more to say. Drill more wells, make more money. Below is the company’s snapshot of their Cleveland wells, taken from the latest presentation. Nuff said.

Adding Magnum Hunter (MHR)

I took a small position in Magnum Hunter, which has been an often cited pick of @Dedwardsays on Twitter, and of whom I heard of it from. There are many things I really like about this company, and one thing that I don’t love. The thing I don’t love is the valuation. The company has an enterprise value of around $2.3 billion. Even after subtracting the value of the pipeline assets, the company trades at around $100,000 per flowing boe based on Q3 numbers. This number isn’t really excessive given the assets, but its not in the “cheap” category that I like. Of course the cheap category also has gotten me into some dogs (see my comments on PXL below) so maybe its for the best.

Also worth considering is that a valuation made on the Q4 numbers should be higher. Magnum expects average production to increase to between 23,000-25,000 boepd in Q4, up from 15,000boepd in Q3, which is quite an impressive jump. The reason that they can increase production so substantially is that the wells they are drilling in the Marcellus and Utica are monsters.

I’m particularly impressed with what the Utica is delivering around Magnum Hunter’s acreage. The company discussed some of the neighboring results on their third quarter conference call, which is really worth listening to if you are interested in the stock. They pointed to three recently drilled Utica wells in nearby acreage producing at initial rates of between 4,000 to 5,000 boepd. Those are huge numbers at $4 gas.

The other asset that is intriguing is Eureka Hunter, the 60% owned pipeline running through the heart of their Marcellus and Utica acreage. The value of the pipeline is expected to increase substantially as the Utica is drilled out and more gas comes on-line that is in need of being piped. Again on the third quarter call, Magnum Hunter suggested that they had received bids valuing the pipeline at $1 billion (with their ownership percentage net $600 million to them) but that they expected that valuation to increase even further as incremental volumes are brought on-line.

The stock makes me a bit nervous because its not cheap, and with the level of debt that they have ($1.3 billion) there is not a ton of room for error. But still, the production growth is very good and the potential even better. So as it dipped back into the $6’s this week I took a position.

Adding Cherry Hill Mortgage

I decided to move my thoughts on Cherry Hill into a separate write-up, which I have posted here.

Frustrated but not selling Palliser

I got into Canadian oil plays in the summer with somewhat of a basket approach, buying 4 stocks. Of those 4 I have had two big winners (Novus and Rock Energy), one do nothing (Pinecrest) and one big loser (Palliser). I am down an ugly 35% on Palliser. At this point the stock is down significantly on the year and in the throws of tax loss selling.

In retrospect my mistake with Palliser was getting in before a clear production trend was established (the same may be said in a few months with Pinecrest, though that is still wait and see). I assumed that the Q2 volumes reflected a turning point, which the Q3 volumes showed was clearly not the case.

Since then I’ve taken a much closer look at Palliser and given a lot of thought to whether I should sell or hold. I’ve decided to hold on. The third quarter was weak (2,300boe/d vs 2,700boe/d in Q2) and October was weaker (2,200 boe/d) but I believe that this weakness was temporary. Indeed I read a Paradigm Capital report that estimated current production as of mid-November at 2,500boe/d.

The company is trading at a fairly significant discount to proved reserves. The PV10 of their proved reserves, which are 64% developed producing, is $75.6 million as of year end 2012. The company’s current EV is $64 million. To trade in-line with their 2012 proved reserves the company would be at 51 cents. Probable reserves, which given the nature of their heavy oil land I would say are quite reliable, add another $37 million would add another 42 cents per share. And these are all 2012 numbers, I would expect them to increase at least some when the 2013 reserve report is released in April.

Meanwhile Palliser is shipping a lot of oil by rail and if I am calculating it correctly they are getting a significantly higher price by doing so. Palliser, is ramping up to ship 75% of their crude by rail. I noticed that with the ramp in Q3, where they shipped about 50% of their heavy crude by rail, the differential between their realized price and WCS shrank by $5-$7 from its historical level. Doing the math on that, I suspect they are realizing around $10/bbl higher prices on the crude they are shipping by rail. This, combined with the fact that they have been excellent hedgers of production which is complemented by the reduced royalty they pay on sold barrels, means that their price in Q4 will not be as dramatically lower as you might think.

Selling Tronox (TROX)

I would look at my exit of Tronox as a temporary one. I listened to the third quarter conference call and to the company’s comments about market conditions and I just didn’t get the feeling that we are that close to the real turn in the market. It sounds more like we won’t see price increases until Q2-Q3 next year. That’s still a long ways off in stock price time.

I’m also not sure how much the market is going to anticipate the move up in TiO2; I think there is skepticism about just how strong that recovery is going to be. There is also the question, which I have not had adequately answered, of whether the customers can reduce their TiO2 consumption further.

And then there’s question of Zircon prices. I had some really interesting discussions with a fellow poster about Zircon and how much Tronox is dependent on it. Tronox is not entirely a TiO2 play. Two of their mines make a significant portion of their revenues from Zircon sales. Zircon prices are well above their historic norms. So to paint a really bullish case on Tronox you have to be able to paint one for Zircon.

My thought is that Zircon may stay higher for longer, but I have to admit I’m basing that on the analogy to other materials that China/India/Developing nation demand has buoyed and where prices have never fallen back to their historical levels. This thesis was given some backbone by a recent RBC report that I read, where it suggested that there was any immediate supply catalyst for Zircon on the horizon. So if demand stays reasonably strong and the economy picks up things should get tighter, not looser. But still its another risk.

The upside risk of my exiting the position is that Tronox makes an acquisition that is accretive, and the stock jumps on it. Tronox is long feedstock right now(~245Kt, though some of that, I believe it was 110kt, is under contract till year end) and they took out a loan from the banks with the intent of putting it to work with an acquisition.

But when you put it all together I start to waffle. It’s feeling more like a 2014 story, something to re-look at in February. So for now I’m out.

Selling Digital Generation (DGIT)

This was simply an act of selling a stock of which I don’t have particularly high conviction. And I don’t have a high conviction because I don’t really get the business. I mean I’ve read the 10-K, I understand what they do, but I have no sense as to whether they do it well, whether they are better then their competitors, or whether they are the chumps on the block. Yet clearly the answer to that question is going to be extremely important to their future growth. Since its the question that matters, since I lack confidence in the answer to it, and since I have other stocks I want to own more, I sold.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

JONE – “its such a stupid simple idea I don’t know if there is that much more to say. Drill more wells, make more money”

What do you think of their valuation? EV/EBITDA = 10 (rather than the 6 you tweeted). $90,000 per flowing (condensate) barrel. Attempt at valuation: roughly $800m for the current reserves (PV10), a potential future $1.8bn NPV10 for 400 undeveloped Cleveland locations, and I’m not sure how to value their Woodford acreage. EV is $2bn. Is JONE so much more attractive than say CLR (similar growth profile over the next 5 years, EV/EBITDA=9, $150,000 per flowing (oil) barrel)?

Thanks for the comment. I dont understand how you can come up with 10x EV?EBITDA. You are going to have to run me through that calculation.

In particular I need to see how you come up with that $2bn EV number.

Your reply prompted me to re-examine, and it turns out I made a mistake. I used the $1.38bn market cap quoted by Google Finance, which is bullshit. So yes, I follow you. Thanks for the post. I love the blog!