Week 432: Where My (tenuous) Conviction Lies

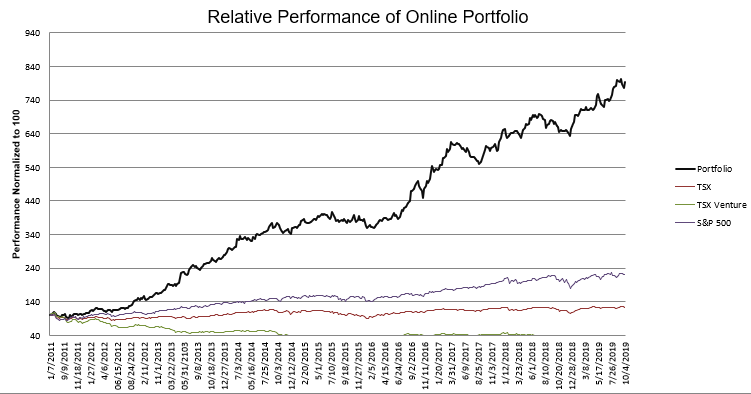

Portfolio Performance

Thoughts and Review

Writing about the broad market makes me uneasy. I fully admit I do not have any edge to it.

Yet I necessarily have to take a position on the broad market, and this blog is about why I make the decisions I do. So regardless of whether my point of view is naïve or uneducated, I still need to describe it. If only for my own posterity.

With that disclaimer, I want to briefly explain why I continue to be cautious on the market even as we approach new highs.

First, caution is different than being bearish. I am not bearish right now. I’m still long many stocks. My longs are roughly double the value of my index shorts.

I am probably not enough of an expert about the macro-drivers of the market to be truly bearish on it at this time. Its too ambiguous to me.

Instead I stick to my knitting – I go long individual companies that I can definitively say I am bullish of. At times, depending on my level of trepidation in the market, I hedge the overall exposure to varying degrees. The bigger the hedge, the more cautious.

Right now, I’m more hedged than usual.

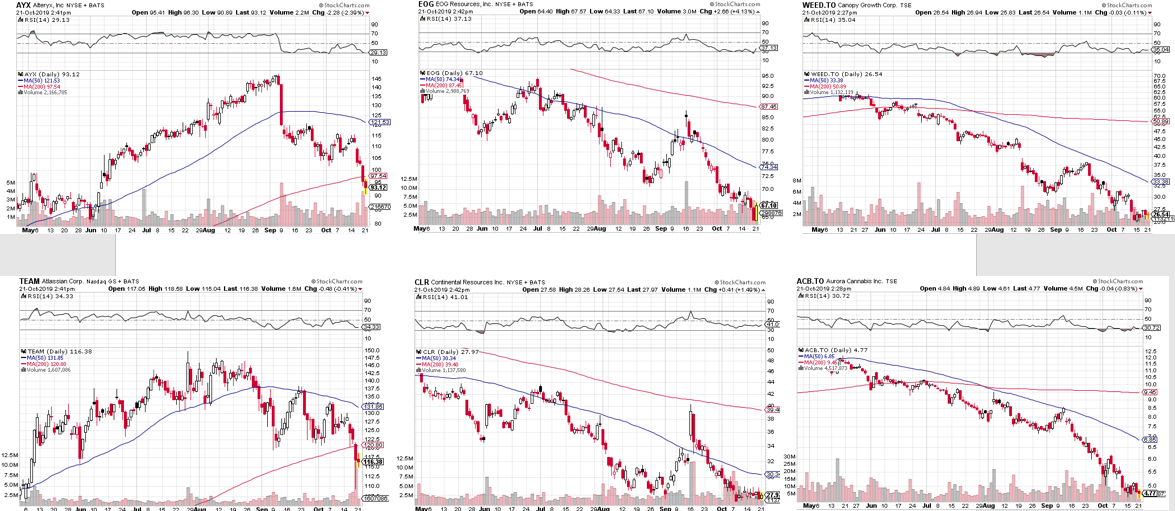

Consider the charts of the following stocks:

When I look at the three sectors that underlie these six charts (SaaS, pot stocks, oils), I don’t see much in common.

Debt issuance is a priority for oil companies. Stock issuance for pot stocks. Most of the SaaS names are self-sufficient. None of the sectors these companies operate in have much in the way of overlapping fundamentals.

The only thing I see in common is A. the chart pattern. The charts are all miserable, and B. these are the sort of stocks that are driven more by speculation than most.

Of course, I am cherry picking sectors that are under-performing. I could take the charts of Texas Instruments, Taiwan Semiconductor or even Apple and paint an entirely different picture about the market as a whole.

But that is kind of the point. It is my suspicion that these poorly performing, uncorrelated sectors are signs that liquidity is a little more scarce than it typically is, but not necessarily scarce enough to a worry the whole market just yet. We are left with rolling bear markets in some sectors, while the overall market holds up.

I have been railing on about tightening liquidity and worrisome economic signs for some time now.

Maybe I shouldn’t. I certainly don’t understand all the machinations. But there are a few general principles I have learned, and that I will continue to stick by so long as they work more often than they don’t.

My first five years of investing were from 2004 to 2008. During that time my Dad was a BMO client and as such I was a faithful listener and reader of their head strategist – Donald Coxe.

Coxe put out a monthly publication called Basic Points and did weekly calls each Friday.

Donald Coxe was quite a good strategist. He wasn’t perfect of course, and some of his views have turned out to be wrong, but many were right and he caught a number of very good investing trends.

One of Coxe’s favorite metrics to gauge the state of the financial system was the TED spread. This was the difference between interest rates on three-month futures contracts for U.S. Treasuries and Eurodollars with identical expiration months.

Coxe followed this spread with interest, and when it rose unusually high, he said it was a time to exercise caution in the market.

He did not pretend to understand all the dynamics that may be moving the spread. In fact, he often admitted it was an opaque market.

What he did know was this – that the spread was correlated to liquidity, and when liquidity was less abundant bad things were more likely to happen than if liquidity was loose.

What bad things? Who knows! It was and is (I think) kind of futile to try to predict what might be the lynch pin. You just look silly most often.

The lesson here is more about the concept and less the particular indicator. The TED spread doesn’t seem to work like it once did and I am not entirely sure if there is a single indicator that has taken its place.

Nevertheless, there are some signs the last few months that suggest liquidity is less abundant that it was 6 or 9 months ago.

One of the signs are these rolling bear markets that are hitting sectors that you might consider speculative. In my experience rolling bear markets in such sectors can preclude downturns in the index as a whole.

We saw something of the sort in 2015. In August of 2015 I wrote:

When I raise the question of whether we are in a bear market, its simply because even though the US averages hover a couple of percent below recent highs, the movement of individual stocks seems to more closely resemble what I remember from the early stages of 2008 and the summer of 2011.

The move down in the index didn’t occur until late 2015 – early 2016.

In all honesty, it doesn’t feel quite as bad now as it did in mid-2015. So we are likely further away from a move of the averages, if it happens at all. Nevertheless, the chance that something like this may occur again has been my caution since the late spring.

There are reasons to believe my caution will turn out to be wrong. Some have talked about signs that the economies of Europe and China are bottoming. There is maybe some sort of trade deal in the works between China and the United States. The Fed is loosening in one way or another. So is the ECB. The weekly leading indicators in the United States have been trending up of late.

Nevertheless, I still think I am more comfortable taking a cautious bent. When I look at the performance from the funds letters I have read, I see some numbers that, while very good so far this year, showed -15%, -20% or even -25% in the fourth quarter last year. I would not handle such losses well, so I prefer to take the cautious road.

If I am wrong it will hurt my performance a bit. But if I am right in my stock picking, that should more than compensate for the mistake. Thus far, it hasn’t really helped my performance, but it hasn’t hurt it either.

It is the individual positions that will make or break my portfolio which is how I want to position things. So, let’s talk about a few of those ideas.

Tankers – I waffled back and forth a bit, but I finally sold the last of my tanker trade this morning. I unloaded most of my position a few weeks ago, but as seems to be the case with ideas I’ve tied myself to for a while, its never a clean split. It may still not be, but I want to see an entry that is not so elevated and over-bought to interest me.

Schmitt Industries – My most recent purchase. I wrote about it here. This stock has been slowly working higher, but my best guess is that it does nothing until the next step in their restructuring is announced, which could be months away or could be tomorrow. I do not know if or when more assets will be sold but given the activist nature of the new CEO, I suspect they will be at some point. With cash still making up most of the capitalization I will patiently wait.

Evolent Health – I wrote about here. We will likely get some resolution on Passport Health Plan in the next few weeks. Interestingly, Piper wrote their thoughts on Passport a couple weeks ago. They were quite positive.

Nuvectra – I wrote about here. My entry in this one was poor, but I added to it after it fell into the $1.30’s and I am now in the black on the stock. I am hoping (this one indeed has a bit of hope involved) that we hear a positive outcome of the strategic review in the next few weeks.

Vertex Energy – I most recently wrote briefly about Vertex here. There is always at least one position in my portfolio that confounds my expectation. Vertex is it for now. In short order they should be a beneficiary of falling HSFO prices (the futures curve, where prices were as high as $50-something per barrel as recently as September, is setting up just as I had hoped) and that should mean blow-out margins. However, one might expect the market to anticipate this and it is not. So I am puzzled.

Gran Colombia Gold, Roxgold, Wesdome – My primary gold stock holdings. They have all corrected over the last month. Roxgold in particular has seen a rather dramatic plunge. They all have their own nuances, but they will all move up or down along with gold and the state of the financial system which I guess is a hedge in itself.

To balance my long portfolio, I am keeping a higher than usual level of hedging by way of inverse index ETFs. As well I remain short a few individual names. My shorts are the same as they were at last mention – a few SaaS names, a couple biotech’s with questionable histories, a couple of cannabis names that are levered to a Canadian extraction market that appears to me to be very oversupplied, a couple of US shales that are seeing their access to debt dry up and that I believe will struggle as a result, and a couple of Canadian banks that I will continue to be wrong about.

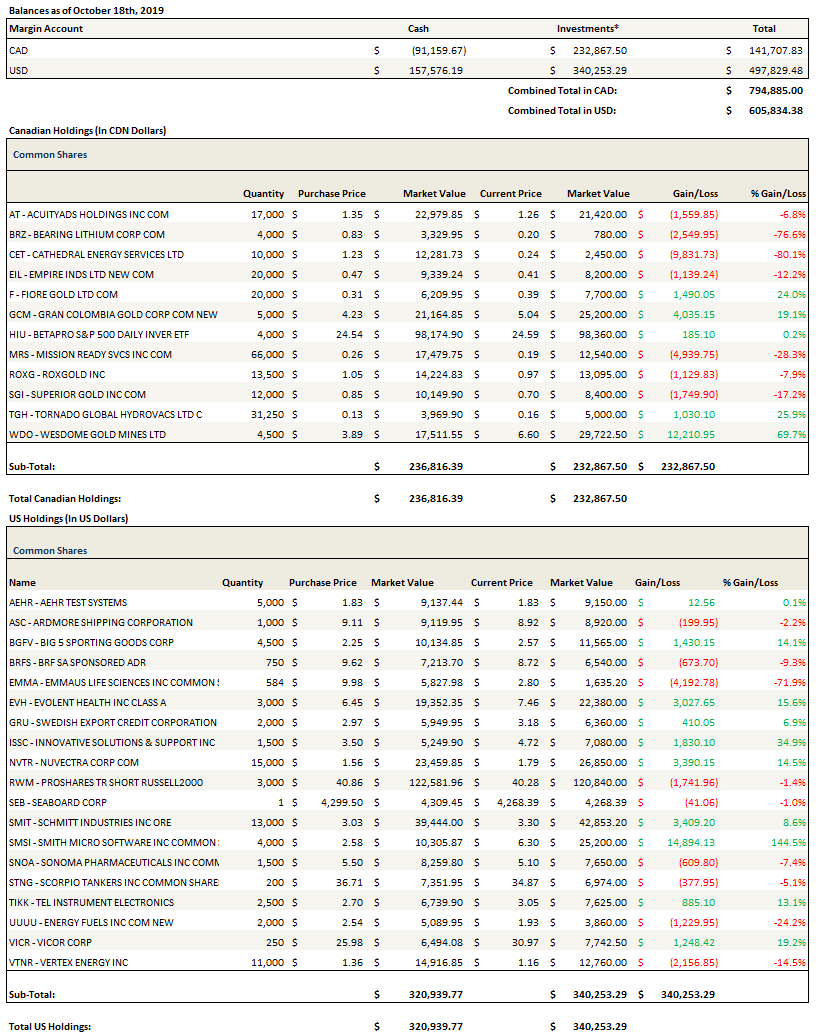

Portfolio Composition

Click here for the last five weeks of trades.

{kind=link}

It sound like you did not trade in the late 1990’s/early 2000’s market, but there certainly is a case to be made that markets now are similar to that time period (although not as extreme).

Back then you had the dot com bubble, S&P 500 massive overvaluation as a safety play and many traditional value stocks left for dead.

In the current environment, you’ve got the social media/tech unicorns/marijuana bubble, utility and other safety type stocks at record valuations and many value stocks, including energy left for dead. I think it is pretty easy to make the case that many of these stocks, like an UBER or a WEED.TO could be like CSCO of the late 1990’s and not reaching their peaks again for over 20 years.

Back in 2000, the bubble was more peaky than this time, and it kept going up until it didn’t, which we seem to be seeing now in a lot of the previous high fliers. But after the bubble burst, the economy really didn’t take much of a hit, even though it was officially defined as a recession, and the undervalued cheap stocks took off and value outperformed growth for years. Personally, it was my best period of market outperformance ever, over 80% outperformance over 3 years.

For a better description of this, take a look at the latest GMO report – https://www.gmo.com/americas/research-library/3q-2019-gmo-quarterly-letter/

or

https://www.bloomberg.com/news/articles/2019-07-23/value-stocks-haven-t-traded-this-low-in-nearly-half-a-century

You never know what is going to happen and especially when, but it sure makes a lot of sense to me that a lot of money is going to be flowing out of things like utilities, the UBERs, SHOPs, even the FANG stocks and it would not take much of this to push up a lot of these cheap, beaten down stocks.

I’m finding plenty of stocks to like in the current environment. One theme I like is that American housing still hasn’t fully rebounded from the great recession (see https://www.calculatedriskblog.com/), so there is a lot of pent up demand and no consumer recession on the horizon. So I own stocks like HDI.TO, a consolidator of building products at a 9 p/e and 7 fwd p/e for a stock that has shown good growth and typically traded at p/e’s 50% higher. Or FUSB, an Alabam bank, trading at 70% of book value, but mainly because their ROE is under 5, so as they work this back to a more industry like 10, ROE, the book value should move well over 1. I guess I could play the home builders directly, but I find these less discovered approaches can often be more successful.

On the industrial side, stocks like HMM-A.TO trade at a sub 5 p/e. They’ve increased the dividend, completed a major expansion and are in the process of reducing debt. Hard to see how this does not get much higher unless we have a major recession. Or lumber distributer Goodfellow (GDL.TO) which is majority owned by Steven Jarislowski and some other smart investors. The stock has traded way down on a botched Systems Implementation, which caused them to understate pricing and take losses. The CEO was fired and they are in the process of getting this 100 year old company back on track and subsequently the stock up.

There are other industries which are exceptionally cheap like energy and life insurance, neither of which is going away anytime soon.

If you are willing to buy overseas stocks, stocks like Hunter Douglas (HDG.AS), the blinds and other home furnishings company, trades at sub 8 p/e or bathroom supply company, Norcros (NXR.L), is a sub 7 p/e on adjusted earnings.

Just some thoughts and ideas. This all may not happen any time soon, but I am fully confident in the long run, cycles always reverse and bad stocks become good and visa versa (like how MSFT went from a growth darling in the 1990’s to a stodgy value stock in the mid 200’s to now a high-valued cloud computing company).

Thanks for the comment Brent. You are right, I did not participate in that period so the perspective is appreciated. I guess I am implicitly onside what you are saying as I am long many small caps? I will take a look at the suggestions you mention, you are always finding interesting ideas!

Smart investor David Barr from Pender also saying small caps as cheap as 2009:

“Picking stocks is the easy part right now. There are so many bargains out there….It’s like going to buy a house and the seller and says “What do you want to pay and I’ve got more for sale if you want them”

https://www.bnnbloomberg.ca/video/opportunities-to-buy-into-canadian-small-caps~1801225

With respect to Vertex, is there a possibility that they may have some sort of hedging arrangement in place that prevents them from benefitting from that spread widening? It seems unlikely to me, and I can’t find reference to anything arrangement that would be structured in a way to remove most of the upside, but I don’t know what the reporting guidelines around that sort of thing are.

Well, I talked with management back in the summer and I didn’t get any information to suggest they were hedging. In the 10-Q they show hedges for the very short-term but nothing that would impact the longer term spread. But I no idea why the stock is so weak when IMO is upon us, larger refiners are catching a bid because of it. Could it be something to do with the Tensile transaction? Maybe the Pilot for Phase 2 isn’t going well? But even then, the stock was way higher before any of that even happened. TBH I have bought more here but I may just be wrong somehow.

Lsigurd, Thank you for continuing to write and sharing with all of us. Not sure if I have posted before (maybe a long time ago, long time reader and appreciate your work and investment returns!). Any updated thoughts on Gran Columbia (GCM) or any gold miners? I’m kind of a novice when it comes to how to value miners as I really bought because of the recap and how absurdely cheap it looked (found it thanks to your blog). With gold breaking out in 2019, I’ve continued to own as it still looks very cheap.

On the other hand, they’ve diluted now at least 2 times maybe 3 (instead of being patient and taking in FCF) since the recap. I understand why they might raise cash as mgmt sounds like if they can change the mine plan at Marmato and lower cash and AISC cost. Perhaps that is why, but thought I would confirm with you and any other followers here. I know that GCM in their earnings call said that institutional investors did not like the idea of putting debt back on the balance sheet for Marmato, so perhaps that cash is also just to start the funding for the spin there. Just trying to make heads and tails of the situation there too with a controlling but reduced stake. Another analyst (although unsure what gold price he/she is using) said they calculated 70MM in FCF after debt paydowns in 2020.

Assuming Sandstorm also has a good PEA next year, it sounds like they would also need to help raise money for that. Could continued dilution result in prices staying undervalued for a long time.

Going back to being a novice on valuing miners, how should I think about all of the drilling being done? Should I think of that like oil & gas where analysts try to understand how much of oil & gas drilling is maintenance capex (to keep production flat) vs growth capex. Ie maintenance for drilling for miners to keep same reserve life / replace reserves vs increase reserve life and/or increase production.

My other thought process around drilling is that they will always drill so you will never see any money, you have to be smart enough to trade them vs GCM paying a dividend eventually. Ie All the miners are always focused on growing and becoming bigger and better (Venezula investment seems odd to me even though it is tiny) vs growing production per share. I know from oil & gas it is ‘drill baby, drill’ and anecdotally miners seem that way too.

Perhaps spinning Marmato will now lead to a dividend since Marmato will not need to be funded by Segovia? That is the impression I got from the latest conference call, but also got the impression they have significant funding for Sandspring assuming PEA goes well.

In your previous posts, you felt that mgmt was looking to extend reserve life and then would sell the company to the highest bidder. Has your feelings changed?

Hi – so I still really like GCM. They remain the cheapest gold producer out there that I can see, and while some are suspicious of the deal with Sprott and spinout of Marmato I don’t really think it matters that these are somewhat shareholder unfriendly in the grand scheme of things.

I would prefer that GCM spends money on exploration and development than a dividend. Drilling is a necessity and in GCMs case it is maybe even moreso than most.

I think that one of the problems that GCM has is that Segovia, even though its been producing for a very long time, has a very short reserve life. While this is the nature of underground operations to some extent, I do think if GCM could show a few more years of reserves or even resource it would be favorable to the stock price.

The other consideration is that the grades at Segovia have been very high the last few years, and the grades in the reserves are somewhat less, so finding more high grade veins is important as well.

This is just mining – always looking for extension and hopefully expansion of tonnage that can be mined.