New Position in Evolus

Two biotechs in a row. I’m out of my comfort zone.

But in a way ,picking biotechs right now is in its own sort of comfort zone. I remain suspicious about the economy (though the market keeps going up, so what do I know!) and companies with newly commercialized drugs are less economically sensitive then your run-of-the-mill S&P stock.

Of course in this case I picked a plastic surgery toxin, which probably isn’t the best place to be if there is a recession. So there’s that.

Anyway.

Evolus just received approval for a new neurotoxin called Jeuveau on Friday. I didn’t hear about it until Monday night. I took a position Tuesday morning, first at $20 and then at $25.

Its been a big move over the last two days but I am hoping we are just getting stated.

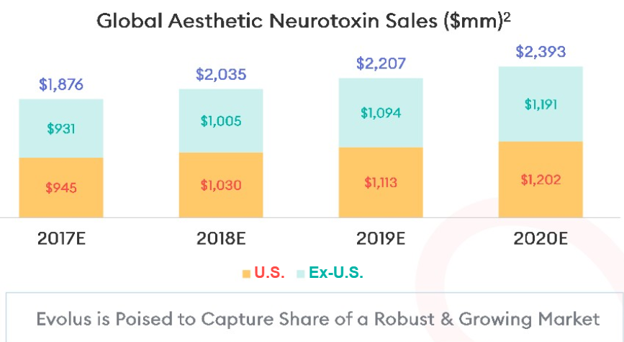

Jeuveau will compete with Botox in the cosmetic neurotoxin market. Botox has an 70% market share right now.

The cosmetics neurotoxin market is about a $2 billion market worldwide. Half of that is in the United States.

The market is growing at almost 10% a year.

Apart from Botox, the other competitors to Jeuveau are Dysport (with around 20% market share) and Xeomin (with about 9% market share).

Dysport and Xeomin were the first wave of competition for Botox. They largely failed in their attempt. Why?

A few reasons: The drugs didn’t show a real benefit to Botox. They had different dosing language (called conversion ratios) than botox. Physicians trained to administer Botox didn’t find it simple to switch over. In the case of Dysport the conversion ratio changed after the drug was used. Finally, they didn’t come out of the gate with a marketing push that differentiated them to patients and physicians. They never developed the momentum to unseat the champ.

Evolus is addressing these issues, both with its trials and launch.

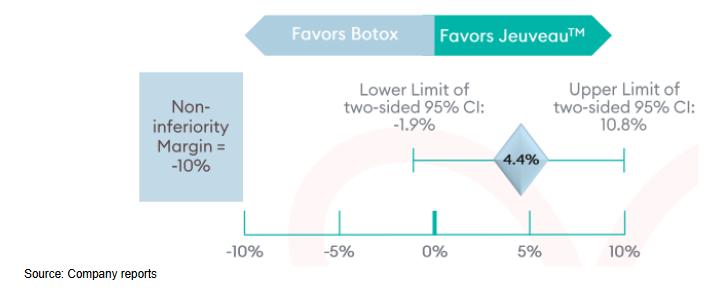

Evolus did head-to-head trials with Botox in Canada and Europe. Patients in those trials preferred Jeuveau to Botox. No one has done a head-to-head with Botox before.

Evolus plans to use that head-to-head data in their marketing of Jeuveau.

In the marketing push Evolus will focus on brand and on new patients. They are targeting millennials. There appears to be more acceptance among millennials for enhancement products like neurotoxins (they say its a consequence of the selfie culture).

Evolus decided to make Jeuveau a cosmetic indication only. If you look at Botox, more than half the revenue comes from therapeutic indications. Jeuveau won’t be competing in that market, at least for now. Limiting the drug to cosmetic means that Evolus has more leeway around pricing and that they don’t have the same constraints on their marketing.

Botox is by far the market share leader but it’s not loved by physicians. Allergen has jacked up prices on a number of occasions. The price per unit has increased 50% in the last 15 years. There is an expectation that physicians will switch if given a better option.

Evolus is owned in part by a group of physicians and plastic surgeons. The parent company, Alphaeon, which still owns over 75% of the stock, has over 200 dermatologists and plastic surgeons as investors. I read one place that these investors make up more than 2% of procedures on their own. The top management of Evolus mostly have come from Allergen: CEO, CFO, CMO, Chief Medical Officer.

Evolus said in the conference call Monday that their goal is to be #2 in the cosmetic neurotoxin market. That implies that they are anticipating at least 20% of the US market. So $200 million. That’s only the United States.

Even after this run the stock is trading at $750 million market cap. My bet is that it can roughly double that if they look like this goal is within reach and get approval for Jeuveau in Europe.

Here’s the risks I see:

- Allergan, who owns Botox is “seeking to block U.S. imports of a new rival to the wrinkle-treatment Botox” because they allege that Daewoong Pharmaceuticals stole trade secrets around Botox which led to the development of Jeuveau. These accusations have been going on for a while but are back in the headlines now that Jeuveau is approved.

- Botox is a pretty entrenched leader. Evolus has talked about how their focus are the millennials, which is not in small part because they realize second-generation clients that have had a Botox treatment are less likely to switch over

- Botox and the other two brands will push back, they will reduce the price of their drugs and step up marketing efforts

- The stock is basically controlled by the executive team and other owners of Alphaeon. Hopefully all interests are aligned but you never know for sure.

{kind=link}

{kind=link}