I wrote about my position in Zargon in my September update. I bought the stock because, after a large asset sale of their Saskatchewan properties at a favorable price, the company seemed poised to recover with an uptick in the price of oil.

As an aside, what a long post that update was! I really was cramming a lot of information into the monthly updates I used to focus on. Hopefully having the updates dispersed into smaller chunks will make for easier reading.

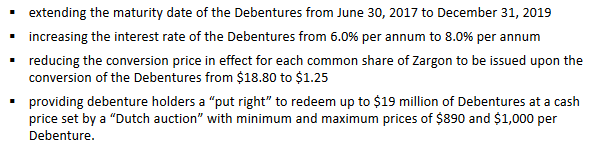

On Friday Zargon announced that their 6.00% convertible unsecured subordinated debentures due June 30, 2017 would be amended, pending approval of holders. The amendments are as follows:

When I looked at Zargon in the fall I did so with the assumption that they would have to dilute to raise capital to pay back the debentures. I was optimistically thinking that would happen at around a 80c share price.

With this deal Zargon is using the cash it has available to pay what of the debenture it can, and then, rather than issuing equity at the current level, its saying give us 3 years and we will issue equity at a 50% premium.

So its much less dilutive than I had been anticipating.

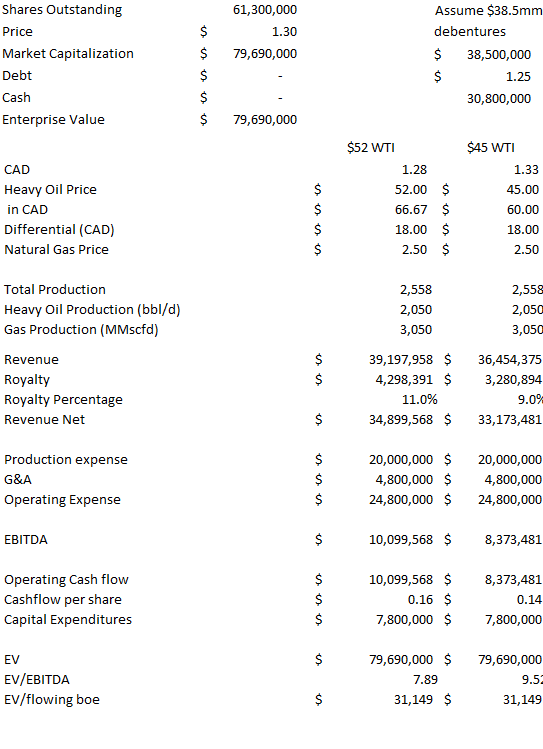

I took a look at what Zargon would look like if the debentures are converted. This happens at a stock price of $1.25, so I took a look at the company at $1.30. That implies over 50% appreciation from the current level. What I’m doing here is asking the question “is this is a reasonable valuation for this company?” – if it is, then there is a lot of upside in the stock.

If I assume that Zargon uses the $19 million to purchase the debentures at par (as opposed to 89% of par), which would be the worst case outcome of the put option, they end up diluting 31 million shares with the rest of the debentures (at $1.30 the debentures would be in the money). The capitalization and metrics look something like this:

(Note that my $52 scenario assumes a 1.28 CAD/USD exchange whereas my $45 scenario assumes 1.33 exchange. I am trying to be conservative by using an $18 differential between WTI and what Zargon realized. This differential was $10/bbl in the third quarter)

Total market capitalization is still only $80 million. There is no debt. And you have a company with a best in class decline rate of ~10%, producing 2,500boepd that is 75% oil.

On traditional metrics it looks reasonable. Even after the large price appreciation the company would still be trading at $31,000 per flowing boe and at a little under 8x EV/EBITDA, which is in-line with peers once you account for the fact that the resulting company has no debt. At $52 oil ($66 Canadian), they can keep production steady with capital expenditures of $6.3 million (in the recent corporate presentation they breakdown the $7.8 million of capital expenditures they expect to incur in 2017 and $1.5 million of it is for land retention). This leaves around $4 million of discretionary cash flow for growth.

I think Zargon could turn out to be a good idea in a rising oil price environment. It wasn’t, and isn’t a great company at $40 oil. Its barely treading water. At $50 it gets its head above. In the high $50’s there is real value there. I thought we were moving into a rising price environment in September and I am more convinced of that now. So I think there is more chance Zargon moves higher than lower.

This is the first of some short write-ups on the community bank stocks that I have invested in over the last month. I mentioned in my portfolio update that I had thought the community banks taken a basket approach, buying 5 names (some of which I had already owned a small amount of in some accounts for a long time). I’m not sure if I’ll write-up all of them, but I’ll try to do a couple.

My thoughts behind the trade are that pretty much all the community banks are going to benefit from a few tailwinds over the next year. These are:

Higher interest rates leading to higher net interest margin

Lower taxes (most community banks pay over 30% in tax)

Reduced regulations (reduced compliance costs)

Better economic growth and a better environment for loans

I want to preface this write-up, by saying I don’t really know if any of the banks I have invested in are the best way to play a rise in community/regional bank stocks. There are so many bank stocks out there. I can’t possibly go through them all. I have a list of about 40 that I looked at and I picked 5. 20 were small and 20 were larger names that I was looking at for baseline. The stocks I bought were those that compared the most favorably. They also seem reasonably priced to me. But there may be (likely are) better ones out there that I just haven’t heard of.

I’m starting with SB Financial (SBFG), which is the new name of a long time holding of mine Rurban Financial. I actually wrote about the stock first here, almost 5 years ago! Its probably the name I like the best out of all the stocks I bought.

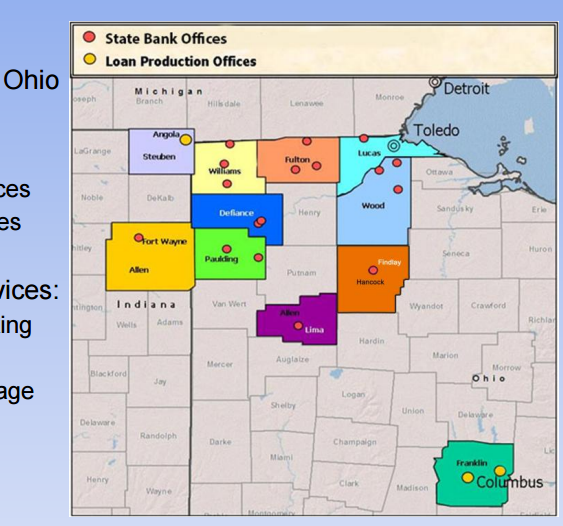

SB Financial operates primarily in Ohio with 18 branches, though it does have a branch and loan office in Indiana and another loan office in Michigan.

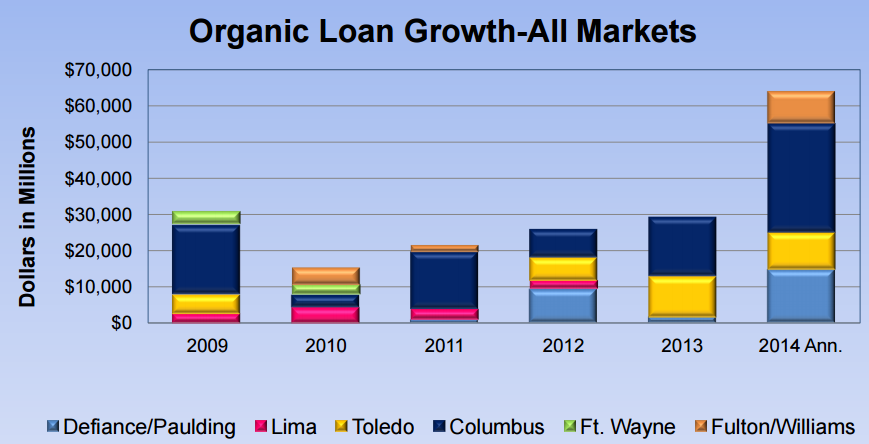

Overall loan growth in the last few quarters has been in the mid-teens year over year:

In a 2015 presentation they describe their growth markets as Defiance, Columbus and Toledo:

I haven’t found any newer data describing loan growth by market.

SB Financial is not as heavily into residential loans as some banks. Only about 22% of loans are residential. Most of their loans are either commercial, commercial real estate or construction loans. I know that construction loans are typically riskier, and the company does not break-out construction loans from commercial real estate from what I can see, so this might be seen by some as a flag.

Nonperforming assets are only 0.6% of total assets. So at least their history is one of prudent lending.

SB Financial generates a fair bit of non-interest income. Apart from the usual fee income, they have a mortgage origination segment that has been growing originations over the last year (up from $86 million to $117 million year over year in the third quarter). While rising rates will have an impact on this business, on the third quarter call the company said that 88% of originations were new money, so refi’s are only a small part of the business. The company also holds a position in mortgage servicing rights that will perform well as rates rise, offsetting the impact of reduced refinancing.

Other non-interest income is generated by the asset management business. Assets under management (AUM) grew to $376 million in the third quarter, which is up 11% year over year. Fee income was $700,000 for the quarter, so their fees are around 0.7-0.8% of AUM annualized.

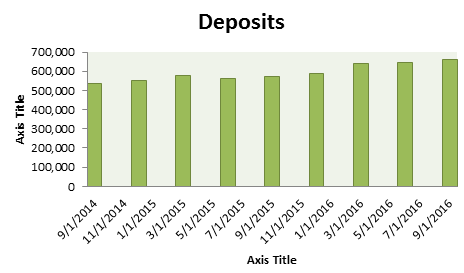

To fund their loan growth the company growing its deposits by adding branches. At the beginning of 2016 they expanded full service banking into Columbus. On the second quarter conference call, they have pointed to a strong start for deposit growth in Columbus, up $5.8 million in first 6 months, 43% since the beginning of the year. The company is planning a similar full service entrance into Bowling Green in the fourth quarter of 2016.

In the past few quarters deposits have been growing at a similar rate to loans, 15% year over year.

SB Financial trades at 146% of tangible book value. They have some goodwill on the balance sheet, which makes their price to book a little lower, 130%. The P/TB is the highest of any of the banks I bought. However they have been the best of the bunch at allocating capital. Return on assets in the third quarter of 2016 was 1.28% and was 1.1% for the first 9 months of the year. Return on equity was 11.9% and 10.3% respectively. I have read that if ROA is above 1% and ROE is above 10%, the bank is doing a pretty good job.

The addition of new branches has likely been a drag to earnings. The company’s efficiency ratio (this is the ratio of their operating expenses to revenue) was 68% in the first 9 months, which is average at best. However as they build the branches I would expect this to come down.

The company reported $1.01 EPS in the first 9 months and 40c in the third quarter. They trade at a little under 12x earnings on an annualized basis of the 9 month numbers. That doesn’t seem unreasonable to me given the 15%ish growth that they are producing.

I’ve owned this stock for 5 years and its given me no surprises. I don’t expect one going forward. Its like watching paint dry, and that’s OK.

I expect the company to keep on generating returns on assets similar to the past, continue to build out its deposit base into new markets (first Columbus, then Bowling Green) and grow fee income through asset management and mortgage originations. Simple story. Hopefully with an additional boost from a federal government policy revamp the stock can trade up to 2x tangible book.

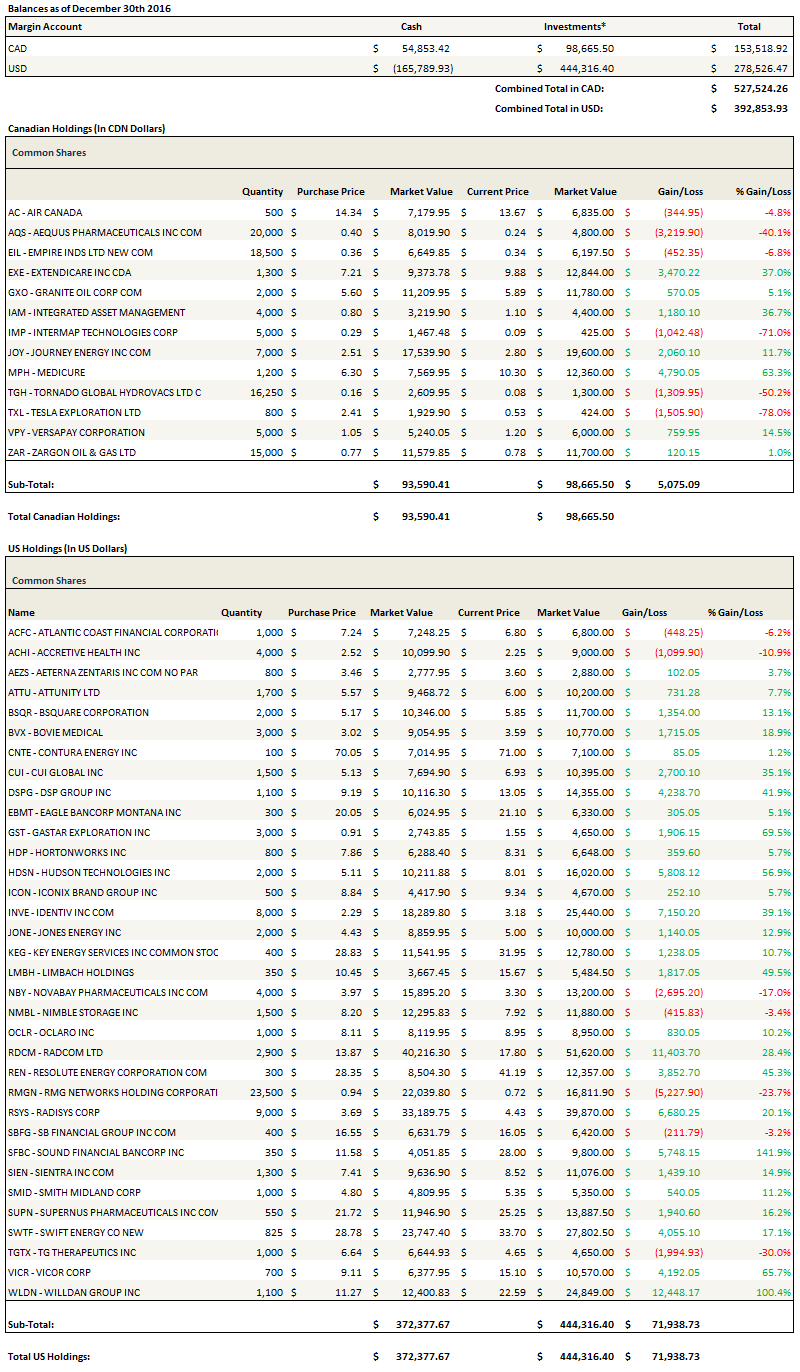

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

The other day I was considering posting an article on SeekingAlpha. I couldn’t muster the energy. I wasn’t sure why, but I felt a strong resistance against it.

So I put it aside and in a couple of days it came to me why.

Take a look at my SeekingAlpha history. I’ve written a few articles for it. The list of names is, at best, uninspiring. Hercules Offshore went bankrupt not long after I wrote about them.

The fact is, I’m wrong a lot. At least a third of the time I pick a stock it doesn’t even go in the right direction. In a bad market that number is likely well north of 50%. And even when I’m right, I often miss by degree. The last couple of months, while my portfolio has done pretty well, it would have done much better if I was not weighted most heavily in two positions that have done absolutely nothing (Radcom and Radisys). My biggest winners are often afterthoughts where credit should only be taken with qualification.

If there is one redeeming feature about my strategy it is that I am fully aware of my own limitations. I am never certain. In my blog write-ups I try to phrase every position in terms of what might happen, both the positive and negative, with the expectation that I may have the thesis totally ass-backwards. If anything, the limitations of the medium (writing) convey more conviction than I generally have.

This doesn’t play well when writing an article that is trying to convince others about what a great idea you’ve just found. It might be, it might not. Who knows. What I can say is that as long as I cut my losses quickly, it presents a pretty good risk/reward. But I have no particular insight into whether its going to pan out or not.

It doesn’t make a compelling narrative.

Nevertheless after another pretty successful year, despite a whole lot of mind-changing and almost constant self-doubt, I can say that it worked pretty well once again. To summarize:

I freaked out in January when my portfolio lost over 10% in a couple of weeks.

I only tentatively added back as the market bottomed.

I sold out of the years big winner, Clayton Williams, about $100 too soon.

I mostly missed anticipating the Trump rally apart from a position in Health Insurance Innovations and a couple of construction plays I bought in the days immediately following the election.

(As I will describe below) it only donned on me that community banks should be firing on all cylinders in the last few days.

Yet I’m up about 35% since July (my portfolio year end) and about 40% in 2016 (though with the asterisk that it is with far less than $50 million in capital 😉 ).

Most occupations don’t tolerate excessive uncertainty. I am fortunate to be involved in one of the few that reward it.

The last Month

Last month most stocks in my portfolio stagnated. The gains I had were fueled by a few oil names (Gastar Oil and Gas, Jones Energy, Resolute Energy) as well as Health Insurance Innovations, Identiv, DSP Group, and a last day move back up by Radisys.

Health Insurance Innovations has been a big winner for me. If only I had bought more! The stock has more than doubled since Trump took office. I sold some of my position in the last days of the year (I mistakenly sold all of it in the practice portfolio so that is why it doesn’t appear in the list below).

The second big winner has been Identiv. Unlike Health Insurance Innovations, I have not taken anything off the table. Identiv remains quite cheap, with only a $35 million market capitalization. There is a rumor that after a presentation given at the Imperial Conference the company suggested some recent business with Amazon, which, if done in mass, could be quite a big contract for the company. I have no idea if its true though. The stock has pulled back in the last few days, but I’m not too worried. As long as business continues along its current trajectory, the stock should do well in the coming year.

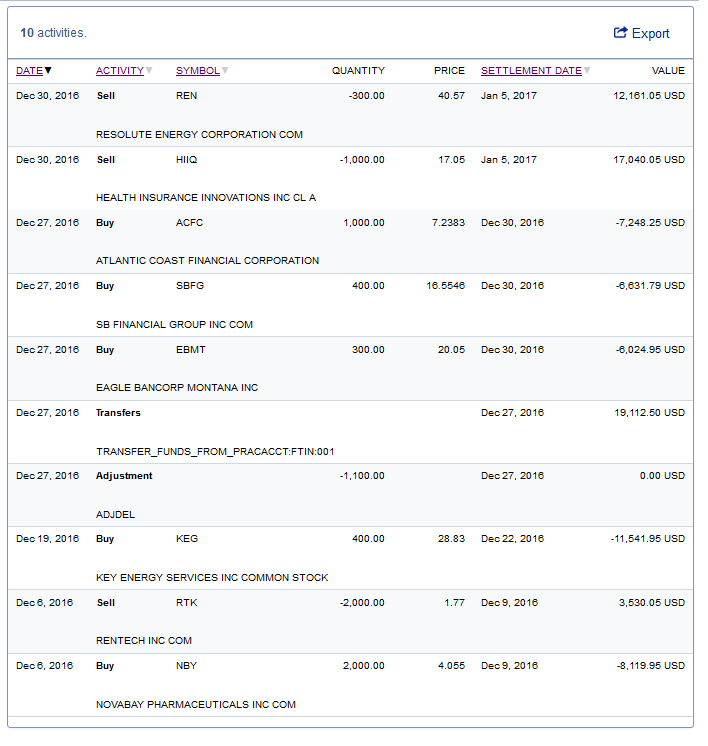

Key Energy Services

In mid-December I took a position in an oil services firm, Key Energy Services (KEY). I was given the idea by someone in the comments section of the blog. Key Energy operates a number of well services rigs, as well as having businesses in water management, coil tubing, and wireline services. This is a tough business, and has been a disaster over the last two years. At least 3 competitors in the space have been through bankruptcy.

At the time I bought the stock it was still trading in bankruptcy. Similar to Swift, existing shareholders received a piece of the new company and warrants.

Since exiting bankruptcy in late December the stock has traded up quite a bit but I think there is still some value there as oil services demand rises. What I remember from past cycles is how leveraged these companies are to improving fundamentals. They gain on both pricing and volume. With both natural gas and oil moving up, this may be the first time since 2012 where Key Energy has had pricing of both commodities as a tailwind.

The company has reduced its G&A, reduced interest expense via the bankruptcy process, and is the first of its brethren to make it through the restructuring process.

On the negative side, its a low margin business, I don’t get the sense that management was particularly astute heading into the slowdown, and in the current pricing environment even after restructuring they are still EBIDA negative.

Nevertheless I am willing to see if I can ride the cycle here. Its probably no multi-bagger, but I am looking for a move into the $40’s where I would sell.

Community Banks

The last thing worth mentioning is that after a month and a half of rallying, and the astute comment of Brent Barber asking me why I wasn’t looking at them, I finally spent some time on the community banks. Its soooo obvious, its painful to think that if I had spent a few hours on November 9th I would have quickly realized the same conclusion and ended up a number of dollars richer as a result.

Nevertheless, a good idea is a good idea. Though the names I bought are up between 10-20% in the last month and a half, I still think they have much further to run. I added positions in SB Financial (SBFG – former Rurban Financial, which I’ve talked about in the past and owned a small piece of of for some time), Sound Financial (SFBL – another bank I’ve owned for years), Atlantic Coast Financial (ACFC – which I have owned and written about in the past), Home Federal Bancorp of Louisiana (HFBL), Parke Bancorp (PKBK), and Eagle Bancorp of Montana (EBMT). I took a basket approach because all of these namess are illiquid and difficult to accumulate in too much size. I will write these up in more detail shortly.

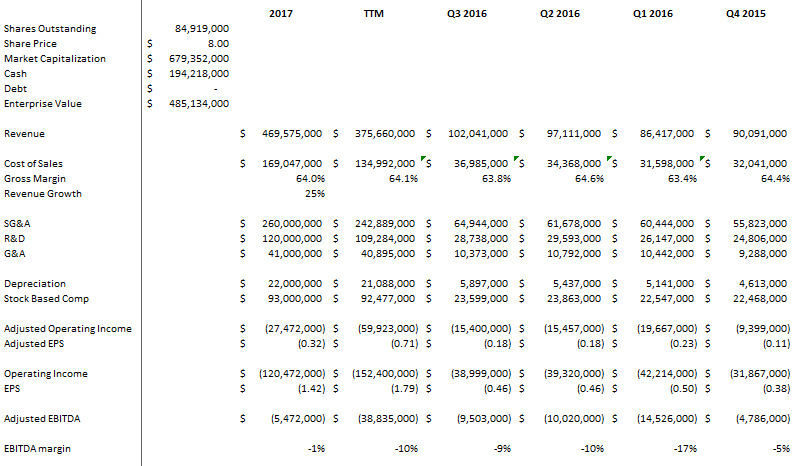

I’ve been dragging my heels on a Nimble write-up. I knew I would have trouble with it. I have a thesis, but I’m not entirely convinced of it, and I don’t feel like I have a really firm grasp of the industry they operate in. So I’m not in a position to write anything very definitive.

What would accurately summarize my thoughts is to say that I think that Nimble may go a lot higher if things pan out. I think the downside is fairly low (maybe 20%) and the upside is high (maybe a double). And while I really don’t have a ton of conviction that events will transpire positively, the risk/reward makes it worthwhile to me.

Nimble sells flash memory. Flash memory has replaced hard disk drives (HDDs) as the preferred technology for persistent (meaning that the data persists when devices are powered down) storage. Flash has much faster read and write capabilities than HDD storage. Its primary disadvantage has always been cost, and that has narrowed as the technology has been refined.

Nimble has historically sold a version of flash memory called hybrid flash. Hybrid flash means they are not just selling flash, they are selling a combination of HDD storage and flash storage. For a number of years hybrid flash bridged the gap by providing some of the speed improvement of a flash array but without all the cost.

At the most basic level, hybrid storage works on the read side by keeping the most commonly accessed data in the flash and the less accessed data in the HDD. On the write side, the flash is used as a buffer that gives the appearance of speed as long as write loads are not too heavy.

This Youtube video, which is ostensibly about Nimble’s operating system, provides a good explanation of how hybrid flash works. It also explains some of the tweaks that Nimble’s hybrid flash incorporates to speed up performance even further. Nimble’s hybrid flash is considered top of the line.

Slowly, technology improvements and cost reductions have been made to flash arrays that have improved the cost/benefit equation enough to justify complete replacement of HDD storage in some of the heavy use applications (referred to as primary workloads). When a storage system uses nothing but flash memory it is called all-flash. The acronym AFA, which is the commonly used terminology in investment reports, stands for all-flash array.

Adoption of AFA’s has happened much faster than had been originally predicted by analysts. Below is a slide from a Solidfire/Netapp presentation that was given at NetApp’s analyst day. The red line represents analysts average estimate of how quickly AFA storage would be adopted. The blue data points are the actual product adoption for NetApp.

BMO indicated in a research piece they did on Nimble (I can’t link to it but I can get it for anyone who sends me a note about it) that the AFA market grew at 88% in 2015 and was 11% of the flash market at year end. BMO expects compound growth of 22% from 2015-2020 at which point AFA will be 70% of the market.

There are only a few major players that provide All Flash arrays. The main one’s are Dell/EMC, Pure Storage, NetApp and HP, as well as a few private start-ups.

Nimble was late to the all-flash party. They have only had an offering since the second quarter of this year. The stock took a tumble in the third quarter of 2015 after investors realized that the growth trajectory of a hybrid flash business model was broken and that it would take time (and have risk) for Nimble to shift its resources to All-Flash.

Since that time Nimble stock has struggled as the company has repositioned itself as an all-flash player. There were poor results as they developed their all-flash offering, and growth from the new all-flash product hasn’t met expectations. There is also the turnover of a disgruntled shareholder base, which may be a bigger factor than any operating concern.

But the company is making progress. While the stock tanked after they released third quarter results, they did show growth. Revenue increased by 26% year over year. All-flash grew at about 30% quarter over quarter.

The negative perception around the results is in part because competitors have been growing as fast or faster off of a larger base. NetApp reported 185% year-over-year growth in the third quarter, while HP reported 100% year-over-year growth. Pure Storage, which reported results in December, showed 93% year-over-year growth.

The other part of the negativity is concern around when the current growth rate will lead to profitability. If you model out Nimble’s earnings assuming a continuation of 25%-ish growth, it’s 2018 before the company becomes profitable on an adjusted basis. It’s even longer if you factor in the very large stock compensation expense.

I bought Nimble because I think there is a reasonable chance that growth accelerates in the coming quarters. Nimble has a few things working in its favor. First, by all accounts their All-Flash product is as good or better than the competition. In fact I came across Nimble after hearing industry contacts raving about the new all-flash product.

Second, they have their legacy, complimentary, hybrid flash product that they can sell along with the all-flash. While high end workloads are moving to all-flash, secondary workloads are still better served by a cheaper hybrid storage. Nimble is a leader in hybrid and can offer both options. Other competitors, like Pure Storage, cannot.

Third, the company has a large existing customer base that they can tap. They had almost 9,500 existing customers at the end of the third quarter.

Fourth, Nimble is just starting to go after bigger accounts. In their third quarter release they said that “bookings from large enterprises (Global 5000) grew 53% and bookings from Cloud Service Providers grew 65%”. I suspect that some of the early disappointment in all-flash growth is attributable to the process of gaining traction in these larger accounts. If the company’s product is as good as it seems to be, this will correct itself over time.

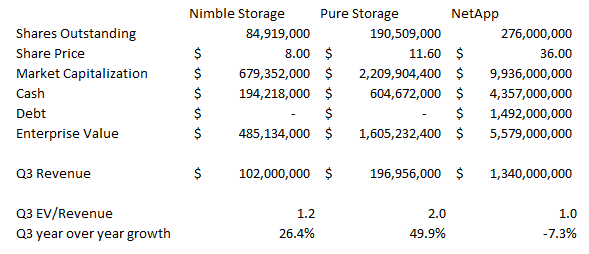

At a $8 share price, Nimble has a market capitalization of $680 million and an enterprise value of $480 million. Given the growth rate of the overall business, I think this compares favorably to peers:

The idea here with Nimble is a bit reminiscent of Oclaro. When I looked at Oclaro in the spring the stock was trading at $4.50, it had kind of a crappy history, a depressed shareholder base, but was beginning to see some secular tailwinds at its back from the 100G ramp. It was well positioned with 100G products to take advantage of that tailwind. It appeared to have decent growth on the horizon, yet if you modeled out that growth based on analyst assumptions it still was a long ways from profitability.

Yet what happened with Oclaro is that growth took off. The stock doubled.

That is what could happen to Nimble. The product is there, the tailwind is there, certainly the crappy past and depressed shareholder base is there. There’s no guarantee it happens, maybe growth sags into the teens and profitability remains distant on the horizon. But if it does happen I think the stock does much the same thing Oclaro did. So it’s worth a position. And an add or two along the way as the thesis plays out.

(Note that my $52 scenario assumes a 1.28 CAD/USD exchange whereas my $45 scenario assumes 1.33 exchange. I am trying to be conservative by using an $18 differential between WTI and what Zargon realized. This differential was $10/bbl in the third quarter)

(Note that my $52 scenario assumes a 1.28 CAD/USD exchange whereas my $45 scenario assumes 1.33 exchange. I am trying to be conservative by using an $18 differential between WTI and what Zargon realized. This differential was $10/bbl in the third quarter)

{kind=link}