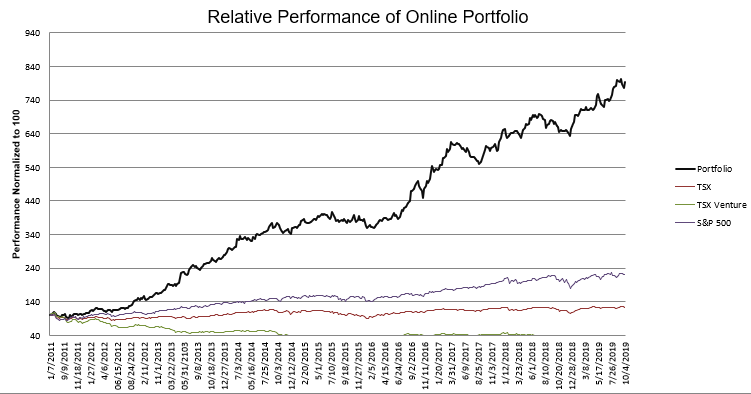

Identiv

In the fourth quarter of 2016 I was fortunate enough to catch the inflection in Identiv. At the time the stock was an unloved perimeter security play that had recovering from the aftermath of a minor RFID mania.

A few years prior Identiv had been named supplier to Disney for RFID transceivers that went into their Infinity toy line. Unfortunately for Identiv, the stock crashed and burned as Infinity turned into a bust and Disney discontinued the product.

The Disney carnage took the stock from $12 to $2. The latter is about where I bought the stock. Like many of my stock picks, I had an admittedly fuzzy idea of how Identiv might play out to the upside.

My long thesis could be summarized in two points:

- Their former CEO, Stephen Humphreys, had returned in September 2015 and seemed to be righting the ship, reducing costs and stabilizing the business to the point where at least they wouldn’t go bankrupt

- At a market capitalization of less than $20 million it was trading at under 0.5x sales and it wasn’t that far from profitability.

As it was, in part because of the turnaround and in part because of a mania in stocks brought on by the election of Republicans across the board, Identiv ran up to $7 before all was said and done.

Since that run up, the stock hasn’t done much of anything. It quickly backed off an admittedly high valuation and since that time has mostly bounced around the $4 to $5 mark.

Identiv reports earnings today after the market closes and I have taken a position going into that report. Not because of the report mind you, I don’t know if the third quarter will have anything special and, having taken a position, I fully expect a 20-30% sell-off on earnings before I have a chance of being proven right on the name.

Two questions here that I want to answer: 1. Why has Identive done nothing for two years and 2. Why am I buying the stock now?

Answer #1: Identiv hasn’t done much for the last couple of years because the company’s business has kind of stagnated.

While Identiv has made a few cheap acquisitions that have helped increase revenue (and in all honesty these acquisitions look pretty decent to me), organic revenue growth has been absent.

The company’s Premises business, ex-acquisition, hasn’t been doing all that well.

The Premises business sells on-premise security solutions to government and private business. This means cameras, keypads or card readers, credentials, locks, and then the hardware and software to control and monitor the premises.

If I understand it right, up until this year the business consisted of two product lines.

- A very robust, federal government certified (the certification is called FICAM – Federal Identity, Credential, and Access Management) security system powered by their Hirsch Velocity software.

- A commercial grade, Cisco partnered system called Identiv Connected Physical Access Manager (ICPAM)

In addition to these full solutions, they sell card readers, credentials, and other physical hardware piecemeal.

My sense is that the Cisco partnership, where Identiv provides the edge hardware and software platform while Cisco provides the network infrastructure and video surveillance piece, has been less than ideal.

Partnerships between a behemoth like Cisco and a minnow like Identiv, have a tendency of not working out all that well for the minnow. I don’t have any specific evidence but based on the lack of mentions of ICPAM since the first half of 2016 I am led to believe ICPAM sales have disappointed.

The other hint is that the acquisitions Identiv has put together are puzzle pieces that Cisco was delivering.

There have been 3 acquisitions that Identive has made.

The biggest of these was 3VR. 3VR is a video surveillance company. Identiv bought them in February 2018. Identiv picked them up on the cheap – paying a little over $6 million for a company expected to generate $10 million in revenue in 2018 and that had over $60 million of venture capital ploughed into it over the past 10+ years.

A second acquisition, in December of 2018, was Viscount, which added two products. Viscount’s Freedom platform is a software-defined physical security perimeter solution, while the Liberty platform is a lower-end, entry-level security perimeter solution. The important piece of both of these solutions is that neither is tied to Cisco servers and video surveillance solutions.

Freedom and Liberty are similar monitoring and analytics platforms to what Identiv has in their own platform Hirsch Velocity (for government, but they address different parts of the market.

I suspect the most important thing about these platforms is that they aren’t tied to Cisco’s gateway, server or video solutions. Hirsch Velocity is a high end solution, used by government, its great for winning government deals but its too expensive to compete commercially. Freedom and Libery provide options for commercial applications that don’t involve Cisco.

Also worth noting is that Freedom is certified for FICAM. Between Freedom and Hirsh, Identiv owns 2 of the 4 solutions that can bid on Federal government security contracts.

Thursby was a third acquisition in November 2018. Thursby added mobile security solutions, including apps for accessing secure data on mobile devices, and dongles and readers used with mobile devices for verifying credentials of the user.

Together these 3 acquisitions and the existing platform of identity cards, scanners, controllers and software give Identiv a complete physical security solution, applicable to government, but also to most levels of business.

While the Premises business has been rather blah for some time, Tthere are some hints it is about to gain traction.

First was the announcement in the first quarter of a fairly large Federal win.

One was a multiyear federal program award to one of our partners for FICAM deployments at over 500 sites worldwide. This is a good indicator of the increasing commitment to FICAM, and it’s really an endorsement of our Velocity software – Q119

– on the 500 sites in the federal government, roughly how many doors per site would that be? Steven Humphreys, Identiv, Inc. – CEO & Director [5] It varies dramatically. It’s anywhere from a couple of dozen to a couple of hundred

I remember back to when I first looking at the stock in 2016, Humphreys said that their FICAM solution would cost around $1,200 per door. If you do the math on 500 sites with maybe 75 doors on average, that would be a $45 million opportunity. Not inconsequential for a Premises business that is doing around $40 million a year.

That win was followed up by this news last week.

Hirsch Velocity Software is the physical access control system (PACS) platform specified in a recently awarded multi-year, $150M blanket purchase agreement (BPA) for the National Physical Security Program (NPSP) Maintenance and Installation Program. As part of the contract, the United States Marshals Service (USMS) is deploying Hirsch Velocity Software at more than 900 facilities across the country to deliver mission-critical security and protection to USMS facilities, visitors, and employees.

Don’t get too excited about the $150 million – I don’t think all of that purchase order is going to Identiv. They are specifically referring to their software getting the win, not the entire platform. But 900 facilities with even 20 doors per facility is still a good sized win for a company this size.

Then yesterday another U.S government agency selected Hirsch for their locations, which are home to 100,000 employees.

There was also this news today that an RFID tag collaboration between NXP and Identiv would be used on a scratch and reward game on Kraft cheese slices.

I’m not sure how material the revenue would be on this application, but Identiv has been trying to gain traction with their RFID products for years now, and this and another recent application in Hot Wheels cars could (and I emphasize could) indicate a turning point.

Identiv isn’t particularly cheap, but its also not pricing in a lot of success. It trades at 10x this year’s EBITDA. A couple of these government wins could tip the scales on that EBITDA number so we’ll see, I’m willing to brave the earnings storm.

{kind=link}