Smith Micro: Stealing a Good Stock Pick

So I can’t take credit for this idea. I also don’t have much to say that hasn’t been said already. But I added the stock to my portfolio a couple weeks ago so I need to talk about why.

Smith-Micro is a Mark Gomes stock pick. In fact if you go to his blog you will find so many posts on Smith-Micro that reading them all would keep you busy for a few days.

I’m not going to repeat all the information he provides. I’m just going to stick to the story as I see it, the reasons that I took a position and what makes me both optimistic and cautious about how it plays out (this is just a typical 2% position for me so I’m not betting the farm).

Yesterdays Smith Micro

Smith-Micro has been a bad stock for a number of years. But it used to be worth a lot. This was a $400 million market cap company stock back in 2010. Revenue in 2010 was $130 million.

At the time revenue relied on a suite of connection management products called Quicklink. This suite of products maintained and managed your wireless connection as you moved around with your USB or embedded wireless modem (remember those!). They also had a visual voicemail product that transferred voicemail to text and provided other voicemail management features (in fact they still do have this product).

From what I can tell it was Quicklink that was driving revenue. They had 6 of the 10 big North American carriers onboard and 10%+ revenue contributions from AT&T, Verizon and Sprint. It was a cash cow.

Now I haven’t figured out all the details of what happened next, but the short story seems to be that the smart phone happened. Smart phones had embedded hot spots or mobile hotspot pucks for accessing mobile broadband services. No more dongles, no more laptops looking to keep their connectivity. And the connection management product was no more.

That was pretty much it for Smith Micro. The company never recovered. 2011 revenue was $57 million. 2012 was $43 million. By 2014 it was down to $37 million.

Today’s Smith Micro

The struggles have continued up until today. Over the past few years the company has had a difficult time creating positive EBITDA and revenue growth has been in reverse. Revenues bottomed out at $22 million last year. It’s gotten bad enough that the company included going concern language in the 10-K.

The company currently has a suite of 4 applications.

CommSuite is their visual voicemail product. It is still used after all these years and generates about 60% of revenue. QuickLink IoT seems to be a grandchild of the original Quicklink products but with the focus on managing IoT devices. Netwise seems like another Quicklink spin-off, managing traffic movement for carriers by transitioning devices from expensive spectrum to cheaper wifi where they can while insuring that an acceptable connection is maintained.

So those are the other products. But there is only one that is really worth talking too much about and that’s SafePath.

SafePath is a device locator and parental control app. With the app installed on all devices in a household a parent can keep track of their kids or the elderly (or spouse for that matter) as well as control and limit what apps and access each device has.

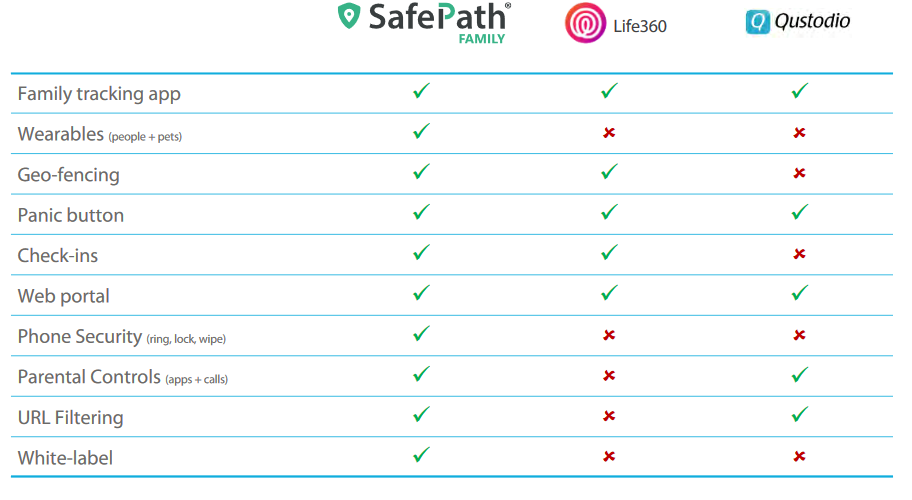

Smith Micro gave a rundown of the SafePath functionality in their latest presentation, comparing it these app store based competitors.

Essentially what these apps let you do is a combination of:

- Keeping tabs where all the other devices in your network are including geofencing alerts if the location is unexpected (ie. children not in school)

- Panic button if a family member is in trouble

- Content constraints on what apps can be downloaded onto each device, what websites can be visited

- Time constraints and time limits on when apps and web content can be accessed

- A history of device usage, location

I think it’s a pretty useful product. I actually didn’t know that so much functionality was available for parents to control what their kids have access to (my kids aren’t at that age yet but I could see a product like this being a purchase for me one day).

SafePath isn’t a unique offering. There are several apps on the market that offer a combination of the features. Each carrier seems to offer some sort of flavor. And there are freeium products available at the app stores, such as Life360 and Qustodio which are the comps used in the table above.

Both the Life360 and Qustudio apps are not associated with any carriers. You get them via the app store and you get some reduced version of the product for free (can only track a couple member of the family, don’t have all the controls, etc). You upgrade to the premium pay version if you want all the features.

For the premium version the pricing on the Qustudio app is between $4.50 to $11 per month depending on the family size. I believe the Life360 app costs $5 per month but I can’t really find recent information on that, and I would need to sign up to get pricing via the app itself which I can’t do here in Canada.

Before I talk about the SafePath pricing, I want to mention that maybe the most important differentiator for SafePath is the white label. Rather than providing a product into the app stores, Smith Micro licenses the app to carriers. They put their own labeling on it and offer it to their clients.

That’s where Sprint comes in.

Why SafePath?

Last fall Smith Micro added Sprint as a SafePath customer. Sprint obviously is a huge win, with 55 million wireless customers.

Sprint has named their version of the app Safe & Found. The product was launched near the end of 2017 but didn’t really accelerate until the last couple of months.

Prior to Safe & Found Sprint offered a product called Family Locator that provided location detection for families. They had a separate app for parental controls called Family Wall. These products didn’t work at all on iOS.

Combining the functionality into a single app that’s available on all operating systems is likely part of a bigger strategy. At the LD Micro conference William Smith, the CEO of Smith Micro said this:

[Safe Path is] an enabling platform for a carrier that is looking for a strategy to grow their consumer IoT devices… [such as] wearables, pet trackers, a module that goes in your car and lets you track your teens driving, a panic button that you give to your parents…

Putting together a single product geared at families is about attracting families to the carrier. Families are low churn and high dollar value customers.

Sprint is selling the Safe & Found app for $6.99 per month, so in-line with the other apps that are available. Smith Micro has a revenue sharing agreement, taking a cut on each customer. Apparently, Smith gets about $3/customer/month from Sprint (though I haven’t been able to verify that number).

The Sprint Bump

Ok so now let’s throw out some numbers.

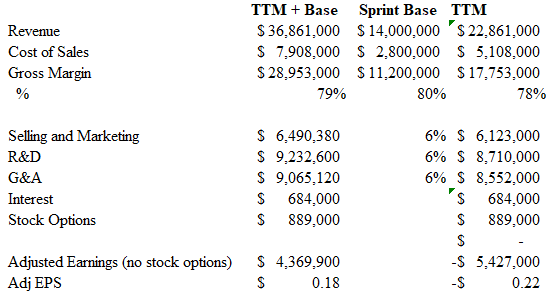

Smith Micro has about 24.5 million shares outstanding. At $2.50 that gives it a market capitalization of $61 million. There is about $10 million of cash on the balance sheet (maybe a bit more but they are still burning cash so call it $10mm) and $1.5 million of debt.

TTM revenues were about $23 million and gross margins are 75-80%.

Now let’s look at what Sprint does to those numbers.

On the fourth quarter conference call Smith said:

While the conversion of Sprint’s existing customer base is still underway, it will equal approximately $3.5 million in additional quarterly revenue for the company once it’s completed.

That’s including breakage. So this is a $6 million revenue per quarter company that is guiding that it can add $3.5 million a quarter on a Sprint ramp? Obviously, that’s the opportunity here.

The company said that margins on SafePath will be around 80% and that almost all that margin should fall to EBITDA.

Not surprisingly, if you model this out the company becomes much more attractive.

The above assumes 6% operating cost inflation (gets you to $6.2 million per quarter).

An analyst on the fourth quarter call said Sprint’s installed base was about 300,000 customers, so the above would assume a ramp of those customers (with breakage) to Safe & Found (I would really like to have this number verified though, I can’t find evidence of how many Sprint’s Family Locator subscribers there are anywhere else). Its worth noting that if the 300,000 subs is accurate it is is less than 1% of Sprints installed base. So there’s clearly lots of blue sky if all goes well. On the fourth quarter call Smith said that:

I think it is the goal of not only Smith Micro but also of Sprint to see millions of subs using the SafePath product and that’s a goal that, I think, would be echoing in the executive aisles of the Sprint campus as well.

So we’ll see. The numbers can get quite big when you are dealing with 80% margins and a large installed base.

Can Reality match the Model?

That’s the big question. Are these numbers achievable?

Look, I take small positions in a lot of little companies that give a good story. I tend to take management at face value.

This is a bit unconventional. I get called out for it by more skeptical investors. When these investors are right, which is more often then not, then they get to gloat and I get to look like a naïve fool for trusting management.

But bragging rights aren’t everything. There is a method to my madness and that method is that when I am right, I sometimes get a multi-bagger out of it. The big wins drive the performance of the portfolio and while on a “naïve-fool-basis” I come out looking poorly, I also come out profitably.

Nevertheless, I always try to keep it at the forefront of my mind that there is a pretty good chance that this isn’t going to end well.

With Smith Micro I’m taking management at face value. If they say they can do $3.5 million a quarter from Sprint, then okay, I’m buying the stock on the basis that they do $3.5 million a quarter from Sprint. They say the goal is for millions of subs then I say, okay, lets see that happen.

But I also recognize that might not happen.

My Concerns

Honestly my biggest hang-up with the stock right now is the reviews. The reviews on Google Play could be better.

I recognize you have to take these reviews with a grain of salt. First, they make up a very tiny percentage of the total downloads so far. Gomes put together a very helpful table of his estimated downloads and the reviews that have been added. Reviews are much less than 1% of downloads.

Second, its not clear that the reviews are all legitimate. I haven’t done this, but some others have dug into the reviews and questioned that they are often coming from locations that aren’t even in the United States.

Third, apart from a few legitimate concerns like battery drain (which other reviewers actually contradict), most of the reviews seem to be more about complaining that the Family Locator app they were used to is gone. Fourth, the trajectory of the reviews has been getting better.

Nevertheless the reviews are a datapoint and right now a somewhat negative one.

My second hang-up with the stock is that, at least from what I can tell, Sprint hasn’t completely shelved their legacy Family Locator app. On the first quarter call Smith said this:

The legacy product was originally due to sunset in the first quarter of 2018, but has subsequently been delayed for several months. This change was based solely on Sprint operations and was not a result of the SafePath application or change of our contract status.

Why has Sprint delayed the sunset? I have no idea. It could be (probably is) a completely benign reason. But again, it’s a bump in the road to weigh against the $3.5 million a quarter that I am taking at face value.

My third concern is that management hasn’t been on target with their projections. Originally they said the ramp on the Sprint installed base would be complete by the first quarter of 2018. That turned out to be way off. They were also positive on a Latin America carrier win that doesn’t appear to have panned out.

Finally, concern number 4 is that we are dealing with a service provider. These guys are A. Slow to adopt, and B. not at all loyal. We’ve already seen point A prove itself out as the ramp has lagged. Point B is something I’ve already experienced with Radisys, which was dumped unceremoniously by Verizon. Smith Micro has had this experience multiple times in its history, most recently by Sprint themselves when they dumped their NetWise product after what Smith Micro called a promising launch.

These are all reasons this is a 2% position for me.

On the other hand, Sprint does seem to be moving ahead. There was a big promotion in May including a joint deal for AAA members (talked about here), reps have been visiting stores and getting the sales staff up to speed, and stores are promoting the app to varying degrees.

One other potential positive is that Sprint might not be the only Tier 1 win. The CFO, Tim Huffmyer, presented at the Microcap conference in April. He mentioned a second win with a Tier 1 European carrier.

Huffmyer said that they had already been selected as the family safety application for this carrier but that the contract process was still ongoing. If they get the contract finalized it would be rolled out to Europe, Asia and the Middle East where this carrier operates. He didn’t give any more details on size but presumably it would not be a small rollout.

I know from painful experience how slow Tier 1 wins can be. But quite often they get around to it. It’s a good sign that they are moving down that road with others.

A Typical Stock for me

This is a Mark Gomes pick and I am stealing it. But I am stealing it because it fits right in my wheel house.

There is no question the stock could be a dud. The Sprint ramp might stagnate, Sprint might walk away and go back to the incumbent or to some other option, and then there is the merger with T-Mobile that throws yet another wrinkle into the equation. Who knows what’s in store?

The one thing I do know is that if the launch is successful and Smith hits their targets, the numbers are big enough to justify a higher stock price. Viable growing businesses with 80% gross margins and a recurring revenue model don’t trade at 1-2 times revenue. Simple as that.

So this is a classic stock for my investing style. An uncertain opportunity that has some positives, some negatives, no sure thing, but an upside that is more than large enough to make it worth throwing your hat in the ring.

How often do these sorts of opportunities pan out? Definitely somewhere south of half the time. If it doesn’t then I get to look like a naïve fool for trusting management. But if it does I get a big winner. It’s these sorts of moonshots where the 5-baggers come from. And that’s what drives the out-performance. Crossing my fingers that Smith-Micro will be next.

{kind=link}