Week 359: Buoyed by the CAD

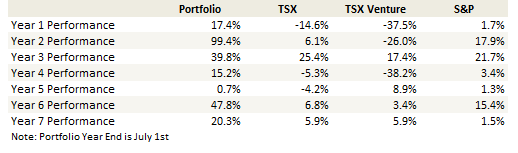

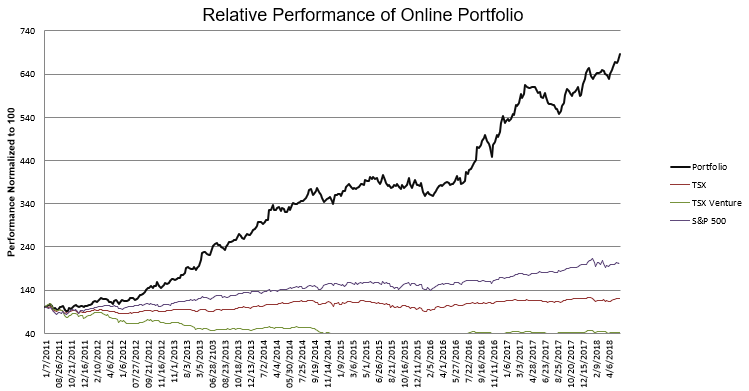

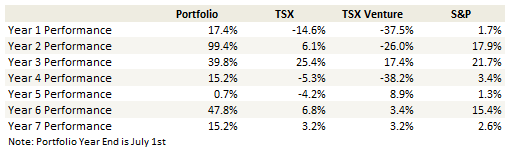

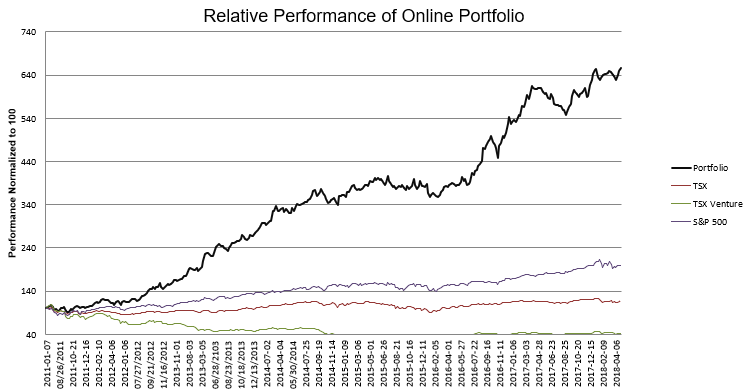

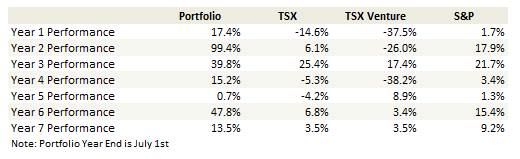

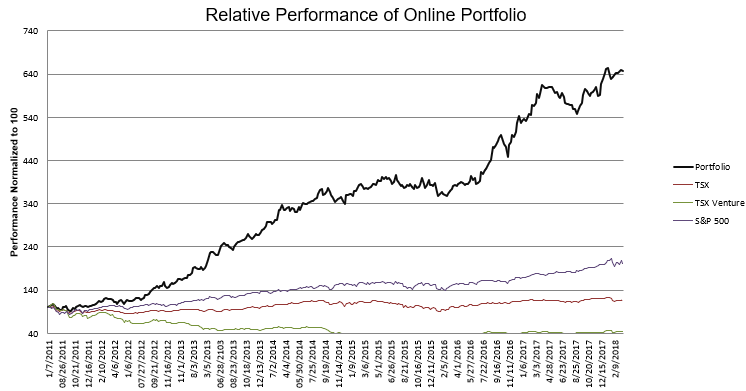

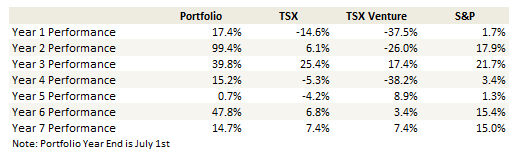

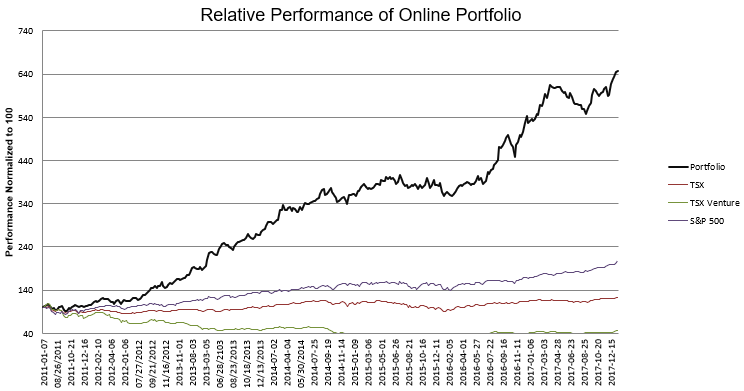

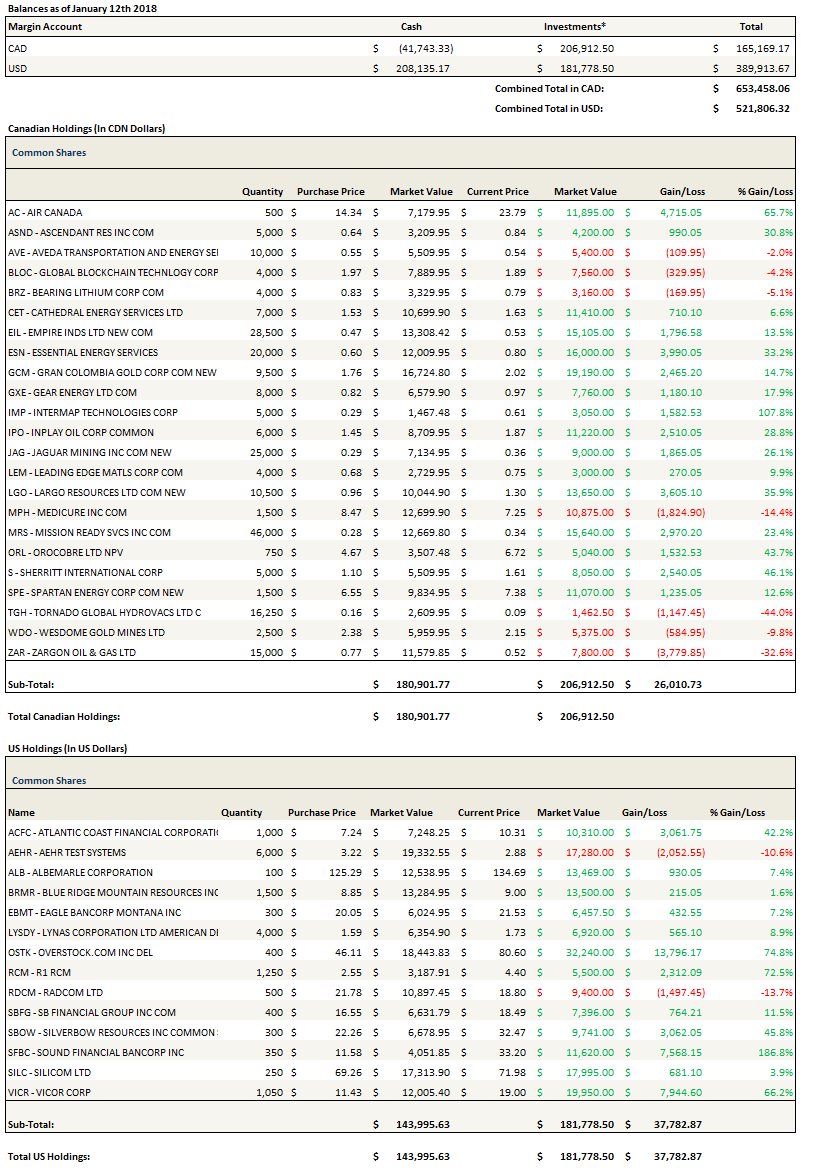

Portfolio Performance

Thoughts and Review

Another quiet month for my portfolio as I only added and subtracted a few stocks around the edges. But I had quite a good month.

I can’t take credit for all of it however. I have been getting a boost from the Canadian dollar. Since March the dollar has fallen from 81c to 77c. Last spring I talked about this when I was going through a period of massive headwind from a rising Canadian dollar. Now it’s the opposite.

If you do the math, the move in the Canadian dollar has added about $25,000 to the tracking portfolio totals since the beginning of March. So I’m looking somewhat better than I actually deserve (which is quite the opposite of last spring, when I looked like a schmuck as the CAD rose some 15% in a few months!).

Much of the rest of the move (which I can take credit for) is the move in Gran Colombia Gold.

Gran Colombia

In the last 5 weeks Gran Colombia completed the redemptions of their 2020 and 2024 debentures and announced first quarter results. The results were great. AISC of under $900/oz and EBITDA of $27 million.

After accounting for debentures redemptions and share conversions (including all the in-the-money warrants and the not yet converted 2018 debentures) I get about 60 million shares. So that’s a market capitalization of about $200 million (CAD) or USD$153 million at the current conversion. There is another USD$98 million of the new debt and they should have about USD$41 million of cash once all the warrants are converted.

The company did USD$27 million of EBITDA in the first quarter. It seems pretty reasonable that they should do at least USD$100 million of EBITDA in the full year. So even after the big jump in the stock price, Gran Colombia only trades at 2x EBITDA. I realize the gold stocks are cheap and unwanted, but even the most unloved get at least 3x EBITDA and some are getting 6-7x.

I think the re-valuation still has a ways to go.

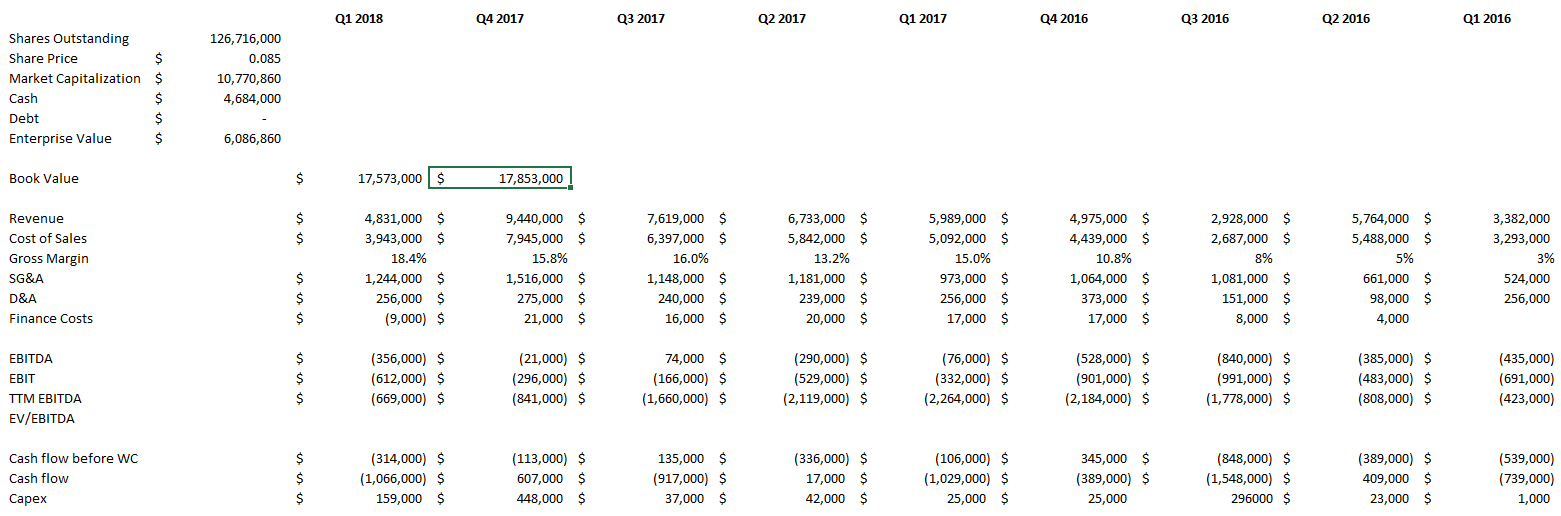

Tornado Hydrovac

Here’s a stock I haven’t talked about in a while. I took a closer look at it after the first quarter results and had someone on Twitter ask about it which got me thinking about the stock a bit more.

Tornado is a $6 million enterprise value company with almost $5 million of cash. However, most of the cash ($3+ million) is in China and not readily available for the North American business. They have an established hydrovac business in North America, and one they are trying to get off the ground in China.

These are the same trucks that Badger Daylighting rents out. But Tornado’s business is not quite like Badger, as they are primarily building the trucks not renting them out. Tornado has had a few rentals (1-4 trucks per quarter) over the past year, so its not a significant business.

The first quarter wasn’t great. I had been hoping for a follow-up on the fourth quarter, where revenue hit a 3+ year high at $9.4 million. But they only had $4.8 million of revenue in Q1.

So it was disappointing and the stock hasn’t really done much. But to be fair, the stock has never really done much so let’s not read into that too much. Still I’m inclined to think the business is turning for the better.

The poor results were partially seasonal – in 2014, 2015, and 2016, there was a significant slip in first quarter revenue from Q4 to Q1 (2017 was a bit of an anomaly because the industry was recovering from the downturn).

Also, inventory ticked up from $6.49 million in Q4 to $9.1 million in Q1. Inventory has been a pretty good indicator of the next quarter revenue, which I imagine is because of the part procurement and build cycle. The company said the following in the MD&A.

For the three months ended March 31, 2018, inventory was $9,072 compared to inventory of $6,490 as at December 31, 2017. The increase in raw materials is due to stocking up for production ramp-up in the second quarter. The increase in finished goods is due to 3 completed trucks held in finished goods as at March 31, 2018 that were not delivered and sold to customers until early Q2 2018.

The other angle with the company is China. They are getting closer to generating revenue from China. Tornado expanded into China over a year ago. Since that time most of the efforts have been establishing a footprint, starting up a manufacturing operation and developing relationships.

In the first quarter they sent out their first three demonstration units in China. Overall, China has overhead of $300,000 per quarter and no revenue.

The inventory related to the three demo units was $1.14 million. Assuming 15% gross margins (margins for the company are around this level), they need to sell about 5 trucks per quarter in China to break even.

But that’s only assuming sales of trucks. The model is China is both sales and services and I’m not sure about what the economics of the services side will look like.

Bottom line is that the stock is reasonable and I think its not a bad bet that they can have a breakout quarter one of these days. Book value is over $17 million while the enterprise value is $6 million.

On the other hand, margins are super-thin and the operating history isn’t exactly stellar. This remains a pretty small position for me, but an interesting one and one worth reviewing from time to time.

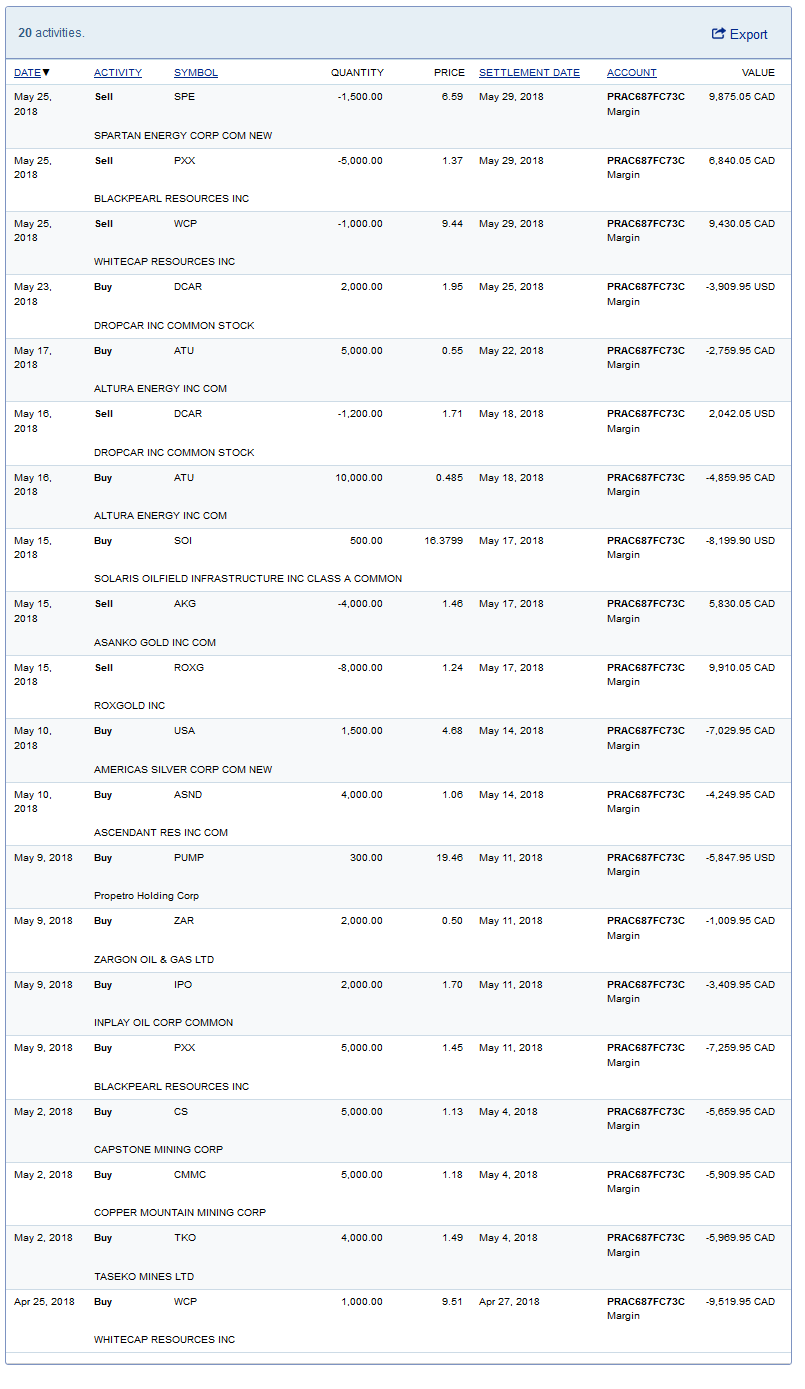

Oil Stock sales

I sold out of a few oil stocks last week. I can’t say that I had foresight into the carnage. A lot of my selling was done on Friday, so after the plunge had occurred. I sold Black Pearl, Whitecap and Spartan.

I have to admit, having missed a better opportunity to lighten up earlier in the week, I was a bit reluctant to do so after these stocks sold off. Nevertheless I had a couple of reasons that led me to decide to sell anyways.

First, I was just getting a little too overweight into oil. In particular, I took on a big position in Altura, which I wrote about, and hadn’t really sold anything.

I was getting particularly uncomfortable with my exposure to heavy oil. The Western Canadian Spreads are looking good but I was long Gear, Zargon, Black Pearl, and now Altura. It was a bit too much exposure.

Spartan was really now a bet on Vermillion and I don’t really know enough about Vermillion to want to take a position there.

Whitecap was just because I was nervous about Canada and Transmountain. I know Whitecap isn’t heavy oil so maybe my logic doesn’t string together that well, but I didn’t want to sell Gear, Zargon or Altura and yet wanted to get my Canadian exposure down a bit more, so there you have it.

The other consideration I weighed was the build in crude last week. It was a surprise, to say the least. It could be a one-off and there seem to be indications that this week will look much better. My thought was that the crappy number last week puts a lot of pressure on this weeks numbers. What if, for whatever reason, its another surprise build?

With the Trans-mountain decision out of the way I might look at buying some of these names back. But I think I will wait until after the Thursday numbers (delayed a day because of Memorial day) come out before doing anything.

Solaris Infrastructure

My services companies aren’t doing that well. Cathedral has been terrible, down to almost $1.20 and if it goes much lower its going to hit the 52-week lows of when oil was $20 less. I already gave up on Essential Energy. Energy Services of America is always a next quarter story.

The problem is that none of these service companies can seem to generate any gross margins.

One story that is not a problem for is Solaris Infrastructure, where gross margins are a pretty amazing 60%. But the stock is suffering nearly as much as these other names anyways.

Solaris provides a last mile solution for storing and delivering frac sand. They don’t actually sell sand. They rent out silos and conveyor systems that are installed on the well site and act as a sand buffer during the completion process.

The silo solution seems like it’s a big improvement over the Sand King trucks that are typically used. Costs are lower, trucks don’t have to sit and wait, and the footprint on the well site is smaller.

Solaris builds the silo units and rents them out on a monthly basis. The gross margins are as high as they are because of the rental model of the business.

Solaris is growing like crazy. Revenue grew at over 205% in 2017.

Here’s my back of the napkin math for a theoretical 2018 exit. At the end of the first quarter they had 98 systems in operation. On May 9th, the date of the conference call they had 108. They are adding systems at 8 per month.

So lets say they have 170 systems at year end. Solaris gets roughly $100k per month of rental revenue per system so that works out to $204 million of annualized revenue.

There is no reason to think they don’t maintain their EBITDA margin of 60%, which would mean they are annualizing $122 million of EBITDA by year end.

In the first quarter they had $3.2 million of depreciation on an average of roughly 90 systems in operation during the first quarter. That works out to $142,000 D&A per system or on 170 systems $24 million annually.

There is no debt so that means income before tax is $98 million and after tax is $77 million at a 21% tax rate. On 47mm shares that would be $1.63 EPS.

If I assume they slow down their build to 6 systems per month in 2019, I get EBITDA of close to $180 million and EPS over $2.50.

None of this includes their new sand terminal in Kingfisher. Or their sand supply chain management tool Propview.

There are a lot of things I like about Solaris but the one thing that I don’t like, that actually gives me a lot of pause, is the stock performance. It is such a good environment for oil stocks and here is a fast growing service company right in the middle of it. And the stock price is as dumpy as can be.

That makes me think that maybe I’m wrong about it. I’m hoping the market is just slow to jump on board, but its also possible that I’m too optimistic. Maybe margins will decline and growth vanish as competition comes on the scene. I have to think that’s what the market is worrying about. Because otherwise the current share price doesn’t make a lot of sense.

One last Buy

The last thing I did was buy a small position in 3 copper stocks. I’m not quite ready to talk about these, meaning I’m not sure I should have bought these stocks or not yet. So I’ll leave that for now.

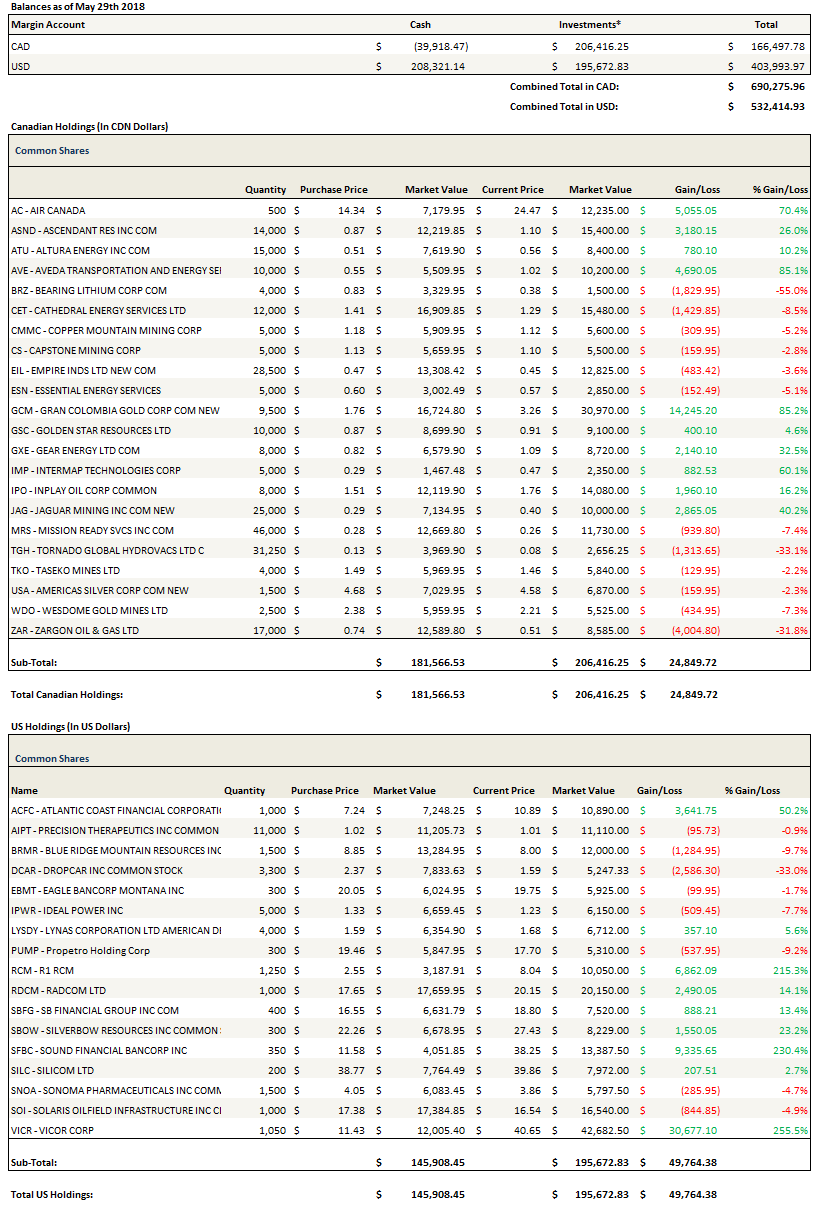

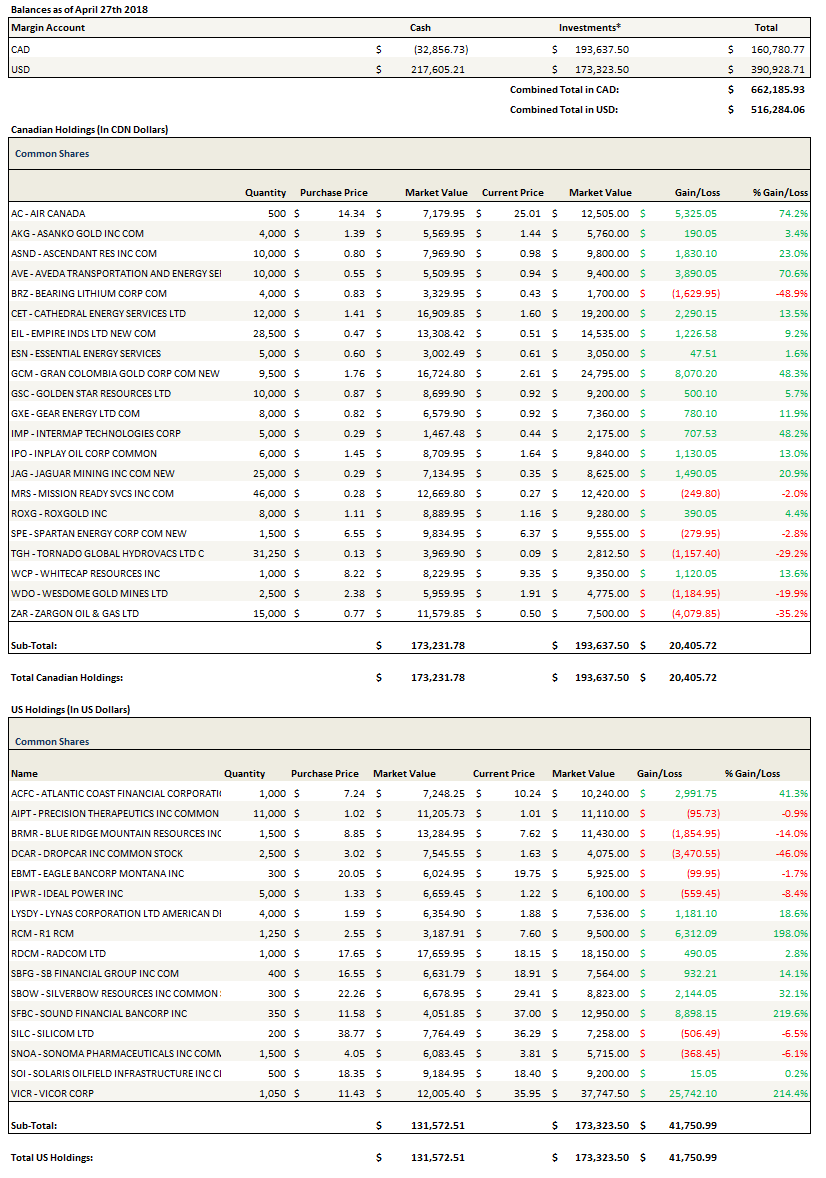

Portfolio Composition

Click here for the last five weeks of trades.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}