Looking at more quarterly results: Air Canada’s miss

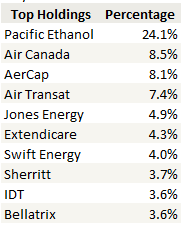

Air Canada is a fairly large position for me so I’ve spent a lot of time on their quarterly results in the last two days. The short story here is that the stock stock got hit because revenue per average seat mile (RASM) was below expectations and because of this, earnings were also below estimates.

There was an expectation among analysts that because load factors (how full the aircraft is) were strong in the second quarter, and because there was anecdotal evidence that ticket price checks showed improvement, Air Canada would pull off a decent year-over-year RASM increase in addition to its cost savings.

Because they didn’t the company missed earnings estimates and, on Thursday, the stock did what the stock did. The average estimate for earnings per share for the quarter was 51c. I saw that BMO was as high as 57c. The actual number came in at 47c.

First, let me say that I added to position on Thursday afternoon. I actually pretty much picked the short-term bottom on this one, a rare occurrence indeed, getting in at $8.50. I added because while the stock was down hard on the RASM miss, I thought that once everyone wrapped their heads around why, we would see it quickly move back up. Read more